CL – Colgate-Palmolive (and additional info on PM).

I see CL as much the same, in certain respects, to PM. Both companies have been around for ever and a day. CL started off way back in 1806 and eventually listed on the NYSE in 1930. PM can be traced back to 1847 with the opening of a single shop on London’s Bond Street selling tobacco products.

With regard to CL, they have been producing and selling products that have become household names, and if these products were not sustainable I guess the company would be long gone by now. So I guess there’s something of a “moat” about CL.

If we are going longer term with the SI Portfolio then I’d say that a company such as Colgate-Palmolive will be there delivering a steady income plus dividend, which stood at 2.4% at its last year end.

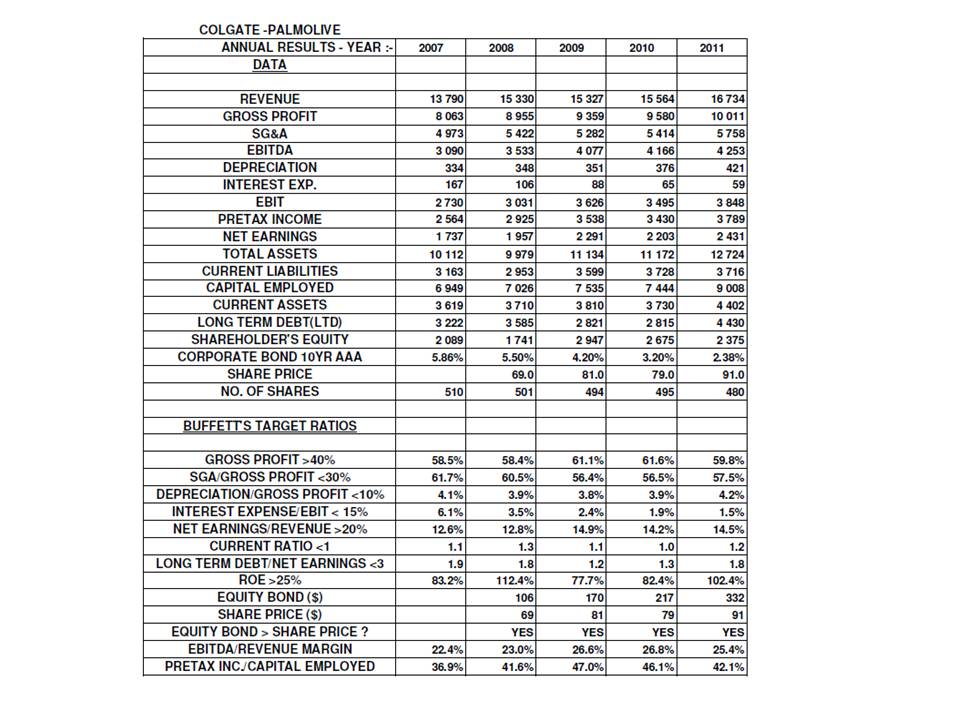

I’ve done a similar exercise with CL as I did with PM, and below are the numbers which indicate the quality of the business ….

Ongoing increase in top line Revenue, little or no debt expense, excellent ROE, excellent EBITDA margin and a very substantial Pre-tax Income return on Capital available to be Employed.

Net Profit is lower than the 20% target, and is also lower than what PM has been achieving, but is still at a very comfortable and consistent percentage in excess of 14%.

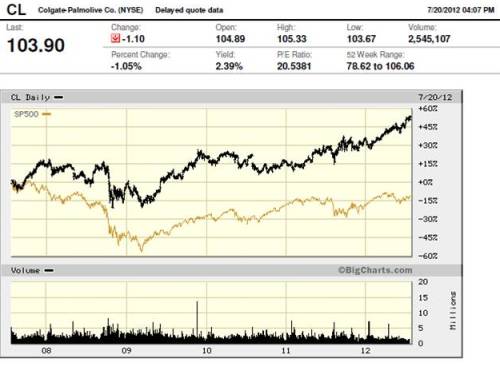

In CL’s 5 year chart below, we see that it’s been outperforming the S&P500 since 2008, and by an increasing margin since the end of 2010 ….

Reading what others have said regarding their stock choices, emphasis is often put on the following areas …

a) what are the future prospects of the company in terms of the market that it’s in, and

b) if the company is at a new low or it’s currently trading below its book value, isn’t that the time to buy its shares because there’s every likelihood that it must surely go up from this ‘low point’.

Speaking for myself, what I prefer to determine from the word go, is how has the company been performing as a business in terms of it efficiency, minimum cost in terms of materials/services, the running cost of the business, minimal or zero expense due to debt, and the maximum amount of top line Revenue that reaches the bottom line … amongst other things.

If all of these relevant components of its financials have gelled and have, simultaneously, been showing a good or above average performance over the long, or even medium, term then it’s very likely that it will continue to do so for the foreseeable future, especially if it’s in the business of basic and/or popular consumables, etcc..

Conversely, if one sees one or more of those relevant components of the company’s financials indicating poor performance, losses, etc.., then that could very well be why it’s price is at a new low, or is below its ‘book value’. So if one then bought its shares before the company had done something to rectify what was evidently a “negative” in its financials, then one could be sitting with an ongoing loser for quite a while. And, in addition, a share holder only realises ‘book value’ when the company liquidates.

With regard to my previous post on PM (Philip Morris) I didn’t include its Pre-tax Return on Capital Employed in its table.

The relevant numbers for PM are :-

37.7%(2007), 43.5%(2008), 39.5%(2009), 46.4%(2010) and 60.6%(2011). |