Here is one answer, from DramExchange--they are revising their previous expectations, as is pretty usual for them. They may end up revising these expectations too in a couple of months, who knows? But for now, whew!

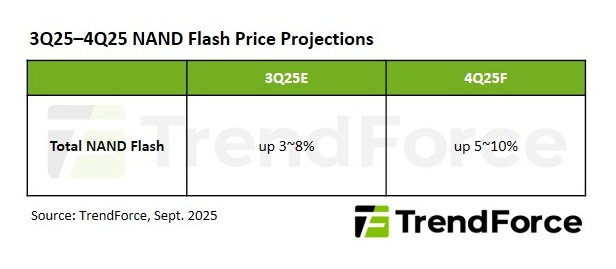

NAND Flash Prices to Rise 5–10% in 4Q25, Driven by Spillover Demand for QLC Products, Says TrendForce

Published Sep.25 2025,14:48 PM (GMT+8)

TrendForce’s latest investigations have revealed that with consumer demand was concentrated in the first half of the year, leading to the traditional second-half peak season underperforming. The market had expected NAND Flash prices to stabilize in 4Q25. However, HDD shortages and longer lead times have prompted CSPs to quickly redirect storage demand toward QLC enterprise SSDs. This urgent surge in orders has resulted in significant market volatility.

SanDisk was the first to announce a 10% price increase, while Micron paused quotations due to pricing and capacity issues. These events shifted supply-side sentiment from cautious to aggressive. Consequently, NAND Flash contract prices across all categories are expected to generally rise, with an average increase of 5–10% in 4Q25.

TrendForce highlights that in the supply side, production reductions and inventory clearance during the first half of the year have greatly enhanced market equilibrium, reducing both suppliers’ inventory and pricing pressures. Aside from a few leading companies planning to expand their new fabs next year, most suppliers are focusing CapEx on migrating to advanced processes in order to improve cost efficiency.

Capacity is allocated to high-margin products to minimize price competition and safeguard profits, creating a price support layer. Regarding the product side, QLC’s cost benefits have increased its adoption in SSDs. As generative AI drives higher demand for extensive data storage, suppliers are more focused on expanding QLC capacity.

On the demand side, the NAND Flash market continues to encounter weak consumer activity, slower OEM purchasing, and high finished-goods inventories in the distribution channels. Nonetheless, server OEMs and CSPs mostly cleared their inventory in the first half of the year. With NVIDIA’s upcoming Blackwell chips expected to increase shipments in the second half of 2025 and ongoing HDD shortages, demand for enterprise SSDs is growing rapidly. This situation helps keep the overall NAND Flash demand on a positive path.

Client SSD

In 1H25, production cuts and shipment adjustments by client SSD suppliers have greatly decreased inventories, helping to restore market balance. Meanwhile, the demand for large-capacity QLC SSDs, which are prized for their cost-performance benefits, remains high, further supporting the market.

Enterprise SSD

SSD suppliers are re-evaluating their 2026 order volumes due to increasing demand for enterprise products exceeding 120TB. They are also strategically increasing QLC output shares to adapt to fundamental market changes. Supplier inventories have dropped below healthy levels, and with growing demand for AI and servers in North America, supply shortages in 2026 are becoming increasingly apparent. This situation is likely to drive prices upward in 4Q25.

eMMC/ UFS

Within the NAND Flash supply chain’s profit-driven strategy, SSDs achieve higher margins, whereas eMMC and UFS experience weaker demand. International suppliers face stiff competition from YMTC and many Chinese module makers, increasing bargaining power for local smartphone brands. High inventory levels among module makers could lead to price competition, which might restrict price increases. However, in an effort to recover losses, suppliers are likely to raise eMMC/UFS prices in the fourth quarter of 2025.

NAND Flash Wafer

During process migrations, suppliers faced temporary output gaps caused by line adjustments, which reduced bit output. To compensate for losses from earlier quarters, they are reallocating resources to high-margin product lines, leading to further wafer supply constraints for module houses. As investment in enterprise AI continues to grow, the tight supply conditions are expected to persist, pushing wafer prices higher in 4Q25.

dramexchange.com |