Why Almonty Industries is THE tungsten mining stock to watch

Tungsten applications. (Source: Gemini. Generated by AI) Tungsten applications. (Source: Gemini. Generated by AI)

Demand for tungsten is rising rapidly thanks to its unmatched hardness, density and heat-resistance, granting the critical metal fundamental roles in the global industrial complex.

Applications include EV batteries, aircraft, rocket and missile components, armor-piercing bullets, bulletproof shields, tungsten wires, as well as tungsten hexafluoride gas used in the production of semiconductors, which facilitate the processing speed required in the burgeoning AI space. These sub-markets contribute to a more than US$5.5 billion total tungsten market expected to surpass US$10.26 billion by 2032, posting a compound annual growth rate of 8 per cent.

Concurrent with robust demand, tungsten’s supply side is falling behind because of numerous idiosyncratic headwinds. Here’s a breakdown:

- In May 2024, the US instituted a ban, effective January 2027, on the military’s purchase of minerals from China, Russia, Iran and North Korea, vying to destabilize the conflict-prone nations. This ruling was soon followed by US President Trump’s March 2025 executive order to strengthen domestic critical mineral production, with the US having not produced tungsten since 2015 and China serving as its largest import partner.

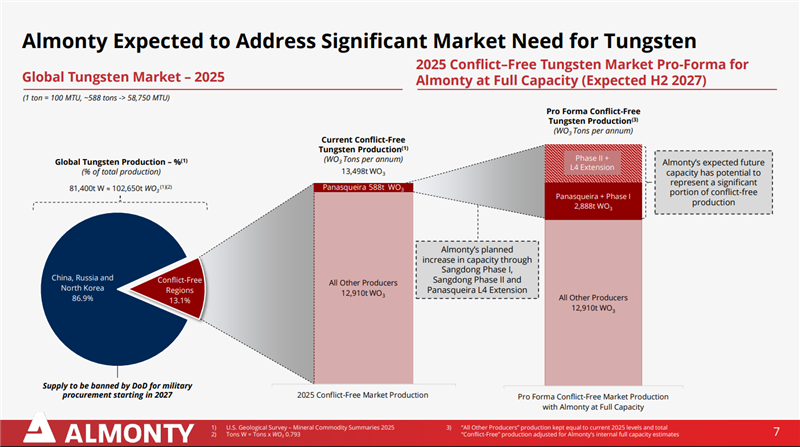

- In February 2025, China imposed export controls on five critical metals, including tungsten and molybdenum, citing concerns for national security. As the world’s largest tungsten producer, representing over 80 per cent of primary production, the communist nation’s market-tightening tactics have sent the rest of the world scrambling to secure long-term resources from more reliable partners, with conflict-free regions representing only about 13 per cent of global tungsten production, according to the U.S. Geological Survey.

- Running through these supply suppressing catalysts is the record pace at which global military spending is rising, coupled with the glacial pace of new tungsten mine development, with only two projects recently in or on the verge of production, including the Boguty mine in Kazakhstan in 2024, operated by Hong Kong-listed Jiaxin International Resources, and the Sangdong mine in South Korea in H2 2025, operated by Almonty Industries, which is listed on the Nasdaq and Toronto Stock Exchange.

Given this push-and-pull supply and demand dynamic, it’s no surprise that the price of tungsten has risen sharply from just over US$200 per metric ton unit (MTU=10 kg) in 2020 to nearly US$500 to date, according to data from Fastmarkets, with strong expectations of a firm floor and untapped upside as ongoing conflicts in Europe and the Middle East play themselves out, the EV and AI revolutions continue their rapid ramp-ups, and the global economy tilts towards deglobalization amid ongoing supply chain disruptions stemming from US tariff renegotiations.

In this way, investors are being handed the high-conviction thesis of resilient and rising tungsten demand, supported by persistently tight supply, which they can put into play by focusing on miners best-positioned to inject new ex-China tonnage into the supply chain at costs conducive to shareholder value.

The West’s only tungsten mine slated for imminent productionThis is where Almonty Industries (TSX:AII) enters the picture once again, thanks to its differentiated position on the global tungsten stage.

This article is disseminated in partnership with Almonty Industries Inc. It is intended to inform investors and should not be takenas a recommendation or financial advice.

Capacity expansions at Almonty’s producing Panasqueira mine in Portugal and past-producing Sangdong mine in South Korea, slated to restart in H2 2025, put the company on a path to becoming the largest conflict-free tungsten supplier by 2027, accounting for about 40 per cent of non-Chinese tungsten production.

Slide 7 from August 2025 investor deck. (Source: Almonty Industries)As the driving force behind near-term Western tungsten supply, Almonty is well-positioned to fill the Chinese supply gap, while growing production revenue at attractive margins, with management targeting gross margins of 50-60 per cent and a net income margin of 30-40 per cent, supposing US$350 MTU (see slide 20 of the August 2025 investor deck), while timing its go-to-market strategy to maximize operational leverage with a near-term tungsten deficit. Slide 7 from August 2025 investor deck. (Source: Almonty Industries)As the driving force behind near-term Western tungsten supply, Almonty is well-positioned to fill the Chinese supply gap, while growing production revenue at attractive margins, with management targeting gross margins of 50-60 per cent and a net income margin of 30-40 per cent, supposing US$350 MTU (see slide 20 of the August 2025 investor deck), while timing its go-to-market strategy to maximize operational leverage with a near-term tungsten deficit.

Merchant Research & Consulting estimates the deficit to reach ~5,570 tons in 2025 and ~2,330 tons in 2026, a tailwind Almonty has gradually aligned itself with, partnering with government relations firm American Defense International in March 2025 and gaining U.S. Congressional recognition for its strategic role in the U.S. critical minerals supply chain in June as it works towards redomiciling from Toronto to Delaware.

Let’s assess Almonty’s main assets, one by one, to capture the full extent of the company’s leadership position and asymmetric value proposition.

Almonty’s Sangdong mineAlmonty’s Sangdong mine in South Korea houses a resource estimated at 36,000 tons tungsten trioxide (WO3) probable (grading 0.42 per cent), 41,000 tons indicated (0.51 per cent) and 218,000 tons inferred (0.43 per cent), making it one of the largest and highest-grade tungsten deposits in the world.

Management projects an over 45 year mine life at full production capacity, while remaining confident in Sangdong’s untapped reserve upside, driven by estimated low-quartile production costs of US$126.8 per MTU and an average metal recovery rate of 85 per cent, as per the June 2025 technical report.

This is in addition to Sangdong’s large molybdenum deposit on an adjacent land package, which is fully permitted for estimated 2028 production to supply a US$20 billion market brimming with military, technology and industrial players keen to capitalize on the metal’s unmatched heat resistance (except for tungsten).

Tungsten mineralization in Sangdong mine. (Source: Almonty Industries)Sangdong’s fundamentals have attracted a number of offtake partners that de-risk Almonty Industries’ path to near-term tungsten leadership. These include: Tungsten mineralization in Sangdong mine. (Source: Almonty Industries)Sangdong’s fundamentals have attracted a number of offtake partners that de-risk Almonty Industries’ path to near-term tungsten leadership. These include:

Backed by industry leading partners and a globally relevant resource, Almonty is hard at work on Sangdong’s phase-I stage, with advanced construction underway and initial production, slated for the second half of 2025, envisioned to ramp up to 640,000 tons in processing capacity and 230,000 MTU of output over the near term.

Phase-II will take the company through construction in 2026 to commercial production in 2027, expanding processing capacity up to 1.2 million tons per year, with higher ore grades relative to the Panasqueira mine, discussed in the next section, expected to improve production economics on Almonty’s path to profitability.

In conjunction, from 2025-2028, Almonty will work towards adding a tungsten oxide production facility at Sangdong expected to yield 4,000 tons per year, expandable to 6,000 tons dependent on market conditions. The price of tungsten oxide sits at approximately US$42,000 per ton as of August 19, according to Shanghai Metals Market, representing about US$168 million to US$252 million in potential revenue.

The upcoming facility will increase Almonty’s long-term exposure to the semiconduc tor and battery industries, backed by an up to US$50 million letter of intent with KfW bank, a memorandum of understanding for the location with the regional provincial government, as well as initial revenue from Metal Tech and Tungsten Parts Wyoming.

Almonty’s Panasqueira mineImminent low-cost tungsten from Sangdong will complement about 58,000 MTUs per year from Almonty’s Panasqueira mine in Portugal, which has been in continuous production for more than a century, including almost a decade under Almonty’s control, during which time leadership has gained the operational expertise required to make Sangdong a success.

The Panasqueira tungsten mine. (Source: Almonty Industries)This expertise is evident in Panasqueira’s low-impurity and high-grade (0.12 per cent WO3) tungsten, allowing for about a 15 per cent premium to market prices at cash costs of only US$185-$200 per MTU, motivating management to more than double production to 124,000 MTUs by 2027. The Panasqueira tungsten mine. (Source: Almonty Industries)This expertise is evident in Panasqueira’s low-impurity and high-grade (0.12 per cent WO3) tungsten, allowing for about a 15 per cent premium to market prices at cash costs of only US$185-$200 per MTU, motivating management to more than double production to 124,000 MTUs by 2027.

Almonty’s value creation is in the earliest stageOverseen by a leadership team with deep tungsten, US defense and mining project management experience, and supported by C$25 million in cash as of Q2 2025, plus US$90 million raised in the Nasdaq IPO in July, Almonty Industries’ ongoing ascent into Western tungsten leadership has garnered broad investor attention, highlighted by an approximately 400 per cent stock return year-over-year.

President and chief executive officer, Lewis Black, who owns 8.27 per cent of the company, encapsulates this sentiment in the Q2 2025 news release, stating that “we believe Almonty is entering a transformative new chapter, poised to deliver long-term value to my fellow shareholders.”

Black’s enthusiasm is catching on with an increasing number of analysts, including Oppenheimer, which set a 12-18-month price target of US$7 per share, representing a 68.26 per cent return from US$4.16 as of August 19, driven by:

- Estimated EBITDA growth from a C$4.8 million loss (adjusted) to a gain of C$43 million in 2026, C$116 million in 2027 and C$243 million in 2028.

- China’s continued domineering of global critical metals supply, coupled with restrictions from the US Department of Defense.

- Rising military spending, as evidenced by a NATO agreement in June to a significant increase from ~2 per cent to ~5 per cent of GDP by 2035.

- A potential C$12 million EBITDA boost by 2028, should market conditions warrant the advancement of Los Santos and Valtreixal, Almonty’s development projects in Spain, the former housing reserves of ~3.8 million tons at 0.13 per cent WO3, and the latter housing reserves of ~2.5 million tons grading 0.34 per cent WO3, as well as an inferred resource of 15.4 million tons at 0.17 per cent WO3.

With differentiated assets and a tungsten tailwind to propel its initiatives forward through 2028, investors have a minimum three-year runway to capitalize on Almonty Industries stock today, taking advantage of numerous potential catalysts including increasing revenue, resource expansion, scaling into better margins and eventual profitability.

None of these catalysts have been fully priced in, given that new production won’t be reflected in income statements until Q1 2026, and operations are still posting net income losses, mostly because of non-cash losses from warrant and derivative liability revaluations stemming from Almonty’s monumental increase in stock price.

Look for increased liquidity and market awareness from the Nasdaq listing, coupled with rising geopolitical tensions, to reward positive news flow and improving financials with increasing floors under Almonty’s stock price, gradually strengthening the case for long-term value creation and demonstrating why there will never be a better entry point than right now for prospective investors.

stockhouse.com |