Re: Recent Dividend Increase - Part 4 PEP (currently owned)

PepsiCo (PEP).

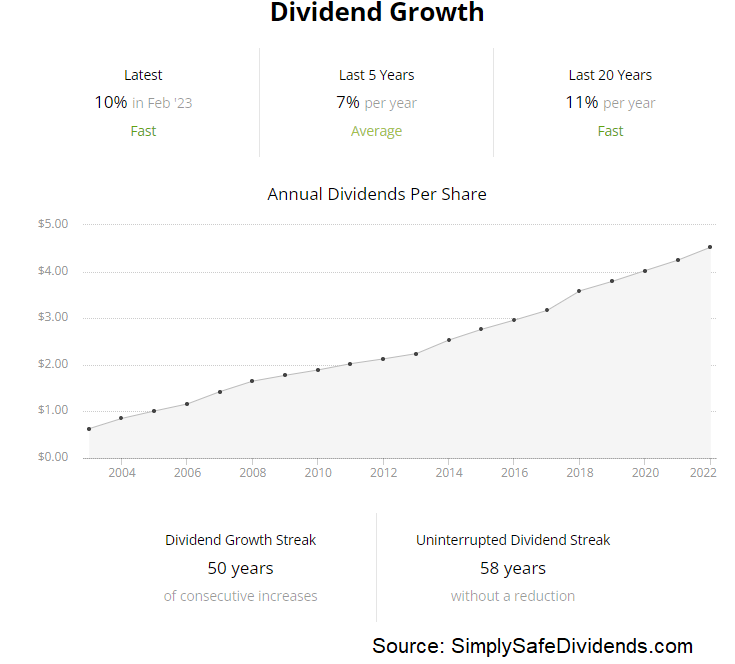

PepsiCo just increased its dividend by 10%. Yet another double-digit dividend increase from yet another high-quality company providing the world with more and more of the products it demands – and doing that providing to more people, at higher prices.

This is the 51st consecutive year of dividend increases for the global beverage, food, and snack company.

PepsiCo is living up to its Dividend Aristocrat status. When I was born, this company had already been increasing its dividend for more than a decade straight. And I’m no spring chicken any more.

The 10-year DGR is 7.8%, so this most recent dividend boost is actually outsized and most welcome by shareholders. The stock now yields a respectable 2.9%. And the payout ratio, based on midpoint guidance for FY 2023 Core EPS, is 69.8%. Higher than I’d like to see it, but PepsiCo has been operating with an elevated payout ratio for a number of years now.

It’s one of my favorite businesses. Not cheap. But it’s a terrific long-term compounder.

I’ve been investing for more than a decade now. Guess what I’ve consistently heard about PepsiCo for the whole time? That its stock is too expensive. Well, all PepsiCo has done over the last decade is grow the business and compound its shareholders’ wealth at about 12% annually.

What’s it worth to have your wealth compound at a 12% clip annually – from a very predictable, low-risk business model? I think that’s worth quite a bit. The forward P/E ratio, based on that aforementioned guidance, is 24.3. The stock’s five-year average P/E ratio is 25.5. I see nothing egregious here. Decades from now, I think shareholders are going to be very happy with their investment.

Source: Jason Fieber |