EVs At 65.4% Share In Sweden – Incentive Scheme Incoming

1 day ago

Dr. Maximilian Holland

20 Comments

Support CleanTechnica's work through a Substack subscription or on Stripe.

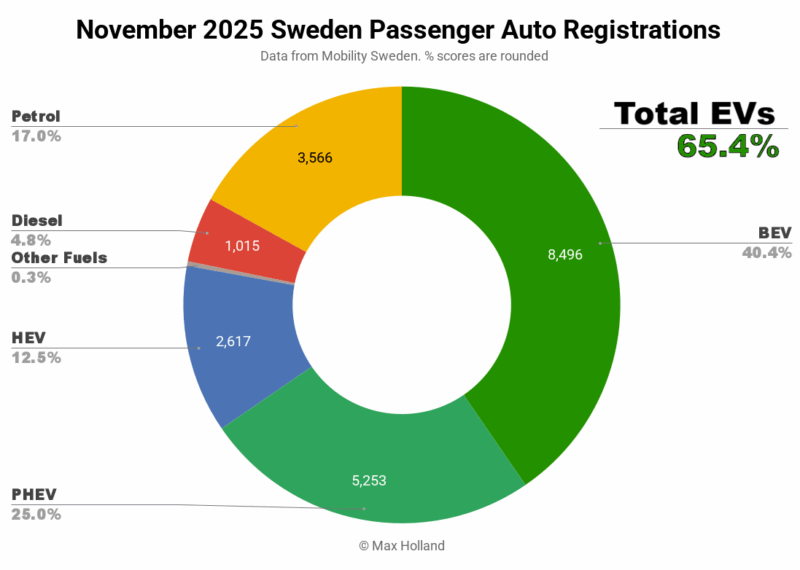

November’s auto sales saw plugin EVs at 65.4% share in Sweden, up from 61.7% year-on-year. BEVs were up in share, while PHEVs were flat. Overall auto volume was 21,016 units, down by some 15% YoY. The Volvo EX40 was the best-selling BEV.

November’s auto sales showed combined plugin EVs at 65.4% share in Sweden, with full electrics (BEVs) at 40.4% and plugin hybrids (PHEVs) at 25.0%. These figures compare YoY against 61.7% combined, 36.3% BEVs and 25.4% PHEVs.

BEVs actually fell in volume by 6% YoY, but the overall market (mainly led by ICE vehicles) fell by more, so BEV share improved. A chunk of the fall in YoY BEV volume is attributable to the Tesla Model Y delivering ~850 units less YoY. Whether this is due to supply delays or demand reduction for Tesla, we will know more by the end of December. The overall YTD BEV volume is up by around 7% compared to YTD 2024, though still 10% down from 2023 YTD.

There may also now be some holdback of BEV sales (at least by some buyers) ahead of new government incentives which were recently confirmed for H1 2026. These will only target lower income consumers in rural areas, but will give a slight boost to the overall BEV market.

Combined combustion-only share was close to a record low, at 21.8%, with volume over 30% down YoY.

Best-Selling BEVs

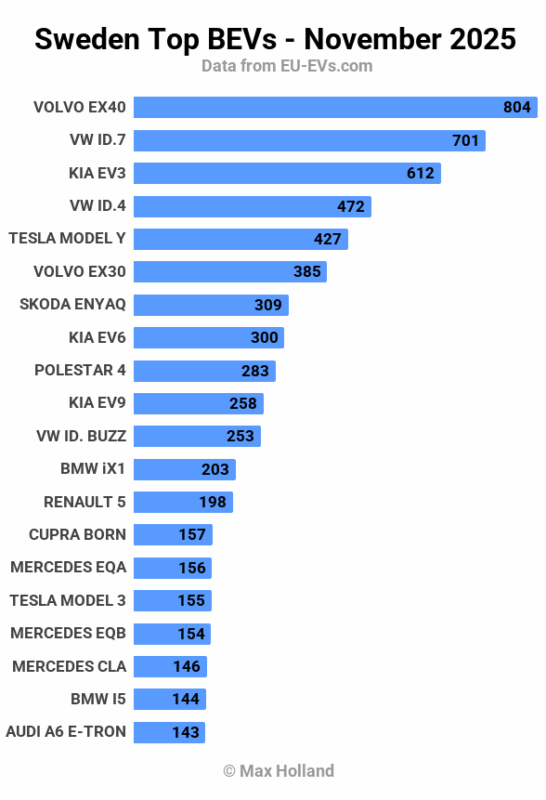

The Volvo EX40 was again the top seller in November, its fourth time in the top spot over the past five months.

The Volkswagen ID.7 came second, and the Kia EV3 came third. This was the same top 3 as October (and August).

Apart from some monthly variation in the volume of well-established models, due to international batch shipping, there was not much change in the top 20. There were, however, two outliers in November with strong performances. The Renault 5 saw its highest volume, with 198 units and 13th spot. The new Mercedes CLA sedan also saw record volume with 146 units, and climbed to 18th.

There were also 3 debutants arriving in the Swedish market in November. The new Kia EV5 made a strong initial impression with 76 units, and will climb from here. Its appearance resembles a downsized version of the Kia EV9, with a length of 4,610 mm.

Another Kia, the PV5 also debuted, with 55 units. The PV5 is a multifunctional vehicle, capable of both passenger use, and also various commercial configurations, similar in concept to the VW ID. Buzz. It is similar in length to the EV5, at 4,695 mm. Both of these Kias save money by sticking with a 400V architecture, unlike some of their more expensive E-GMP siblings.

The other debutant was the Suzuki Vitara, which delivered a more modest 29 initial units. We have covered Vitara elsewhere. It is mainly a compliance vehicle and may not be competitive in the European market unless Suzuki are willing to discount it to achieve compliance-aiding volumes.

Let’s now turn to the 3-month chart:

Here, the Volvo EX40’s consistent monthly lead is obvious, standing head and shoulder above any rivals. The VW ID.7 comes in second, and the Tesla Model Y comes third.

There are no all-new entries into the top 20, just variations in already familiar faces. We can expect to see the Mercedes CLA join the table over the next couple of months (currently in 24th after just 3 months of volume sales).

In the coming months the EV4 might join the top 20 though it may risk being slightly diluted by the EV5. Together, however, and with the popular EV3, EV6 and EV9, Kia will certainly achieve good market share, competing closely with market leaders Volvo and Volkswagen.

Outlook

The new BEV inventive scheme coming in early 2026 will give a welcome boost to Sweden’s EV transition. The scheme is applicable to both new purchases and to used BEVs. This design will give a lift to used BEV values, somewhat encouraging existing BEV owners (even those outside the scheme) to consider upgrading from their existing BEV to a new one.

The Swedish macroeconomy saw a recent upswing, with Q3 2025 recording 2.6% YoY GDP growth, up from 1.9% in Q2 (these figures have been retrospectively revised recently). Headline inflation has recently dropped dramatically from 0.9% to 0.3%. Interest rates have been flat at 1.75% since late September. Manufacturing PMI slowed slightly to 54.6 points, from 55.1 points in October.

What are your thoughts on the EV transition in Sweden? What boost might we expect from the targeted incentive scheme in 2026? Please share your comments and thoughts in the discussion below.

cleantechnica.com |