DragonKrys,

I'd like to address several of your points.

About six months back management provided 2015 guidance of 36M revenue, 33% gross margin, and 15% EBITDA margin. The revenue estimate seems reasonable and could be obtained with a sales mix of 23-27k EPRV (up 10-30% from '14 depending on order timing) and a very modest 2-3k KKM (vs. just 100 following Oct '14 approval). Analyst estimates are in the mid-40Ms which would require significant KKM adoption. This isn't impossible -- a single 100 car unit train order would be ~$300k in KKM -- but seems unlikely for '15 in my estimate. As for margins, I believe management guidance to be conservative, and note they've even stated a 40% target on their website. Regardless, there's little doubt gross will come down from 2014 levels due to EPRV mix (there were some large orders for stainless models in 2014 with higher margins) and KKM introduction. While variable based on sales mix, I use 40% as my baseline for 2015 and beyond. I don’t recall seeing the 33% gross margin and 15% EBITDA margin. Those figures seem highly improbable given that the GM in 2014 was near 45% and the EBIT margin was somewhere around 24% unadjusted and 27% adjusted. I think it’s safe to use 40% since their product insurance liability increased in Q1 and resulted in a 2% GM margin decrease, and also as you suggested the product mix could skew it downwards a tad.

Looking medium term, it's reasonable to assume this could be a $100M business in 2017-2018, though that is definitely a bull case estimate. If you assume the combined new/retrofit market to be 50k cars (at max capacity) and Kelso captures 50% of that with the EPRV, that alone is just ~$28M sales. A key patent covering external PRV design expires in January, but this should have no impact medium term. Still, the growth will need to come from the KKM and BOV. I'm very skeptical of any KKM penetration on the retrofit side due to cost (note there's no regulatory requirement), but if they're wildly successful (again this is bull case) and capture 50% of the OEM market, that could be 16,000 units or nearly $50M sales. Again this is ramping from just $151k in 2014, so there is plenty of uncertainty. BOV sales will just be getting started in a couple years. The adoption rate is likely to be much higher than KKM in my opinion but timing is uncertain. I believe a bullish estimate would be 8,000 units in the first full year, which at an estimated $2,500/unit would be another $20M sales to approach a $100M revenue total. With 40% margins and 12M opex you get 28M EBIT or around $0.36 EPS fully taxed with a little dilution. Kelso captured 50% of the OEM EPRV business in 2014 alone. Based on the growth in market share seen from 2013-2014 and the advantages of their product, I think a 75% market share is a more reasonable assumption.

BOV sales could get started as early as this year. The latest would be mid 2016. The company is pushing for an accelerated field service trial with two other organizations (FRA and I forget the other). It would probably be a 6 month trial or based on a predetermined number of miles traveled.

Longer term prospects are so uncertain that I'm hesitant to put a high multiple on those numbers. With many microcap growth stories discussed here, it's often reasonable to slap a relative valuation (EV/EBIT) on a 3-year estimate, assuming some albeit slower growth in terminal years. With Kelso, it's entirely possible that the bullish scenario plays out, they generate $100M revenue three years out, and then experience declines due to the highly cyclical nature of their business. I don't think most investors respect just how cyclical the railcar industry can be -- and here we're dealing not just with railcar orders but tank car orders, and not just tank car orders but components specifically for volatile cargo. (It may already be apparent that I avoid cyclical industries -- I would have never bought KLS at $1/share except for my background in the rail industry.) Given existing orders, tank car production should continue near max capacity (~32k/year) through 2017, but then it's very possible for this to drop 90% virtually overnight as it's done before -- of course when industry valuations are also at their peak. The regulatory-driven retrofit business looks more stable and will last well beyond 2017-2018 given limited capacity, assuming crude volumes don't erode significantly.

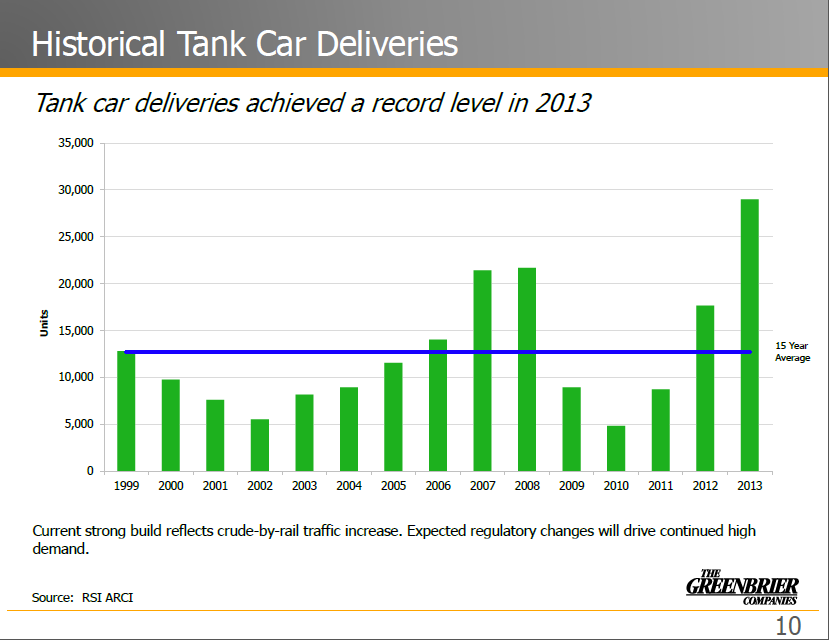

You are right that this is a cyclical industry. However, I think you’re exaggerating when you say that business can drop 90% virtually overnight and you seem to be forgetting that the company can offset some, if not a good chunk, of the cyclicality. The lowest amount of tanker cars delivered since 1999 has been ~5000 and that was only one year. The 15 year average is around ~13k. With the rise in crude by rail, I see this average getting larger or at the very least remaining the same. See the graph below (source: Greenbrier investor presentation).

Furthermore, the way the company can counteract the cyclical nature of the tanker car business is by a) diversifying into new markets (i.e. trucking, marine, railcars other than tanker cars) and b) adding additional products to their pipeline (via acquisition or in-house development). The company is doing both of these things. The retrofit business should also keep revenue high till the retrofit deadline is done.

|