HFT - Transaction Cost: Exhibit A

How much does it cost to keep investors in the HFT game? Is it true, as defenders say, that HFT has lowered trading costs?

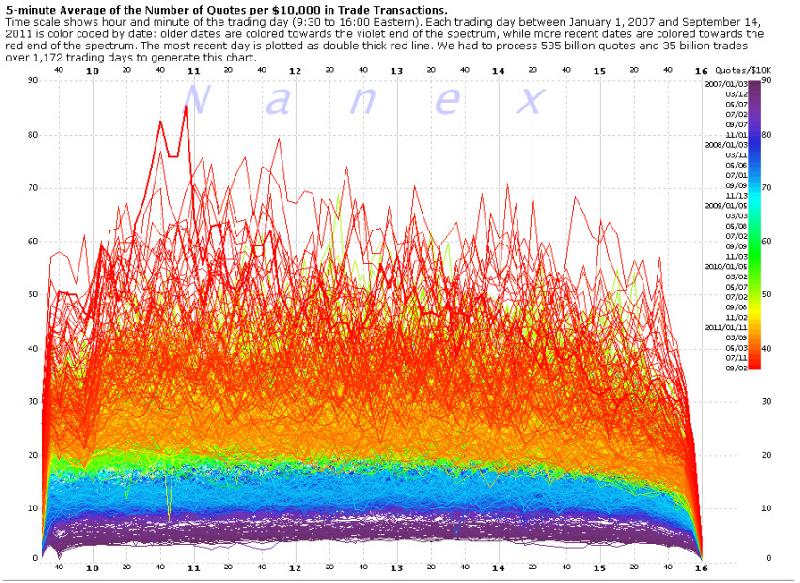

Chart:

From Nanex:

' The chart below shows how many quotes it takes to get $10,000 worth of stock traded in the U.S. for any point in time during the trading day over the last 4.5 years. Higher numbers indicate a less efficient market: it takes more information to transact the same dollar volume of trading.

Quote traffic, like spam, is virtually free for the sender, but not free to the recipient. The cost of storing, transmitting and analyzing data, increases much faster than the rate of growth: that is, doubling the amount of data will result in much more than a doubling of the cost. For example, a gigabit network card costs $100, while a 10 gigabit network card costs over $2,000. A gigabit switch, $200; a 10 gigabit switch, $10,000. This October, anyone processing CQS (stock quotes) will have to upgrade all their equipment from gigabit to 10 gigabit. Which would be fine if this was due to an increase in meaningful data.

We think that a 10-fold increase in costs without any benefits would be considered "detrimental" by most business people.

[Emphasis added, next paragraph]

This explosion of quote traffic relative to its economic value is accelerating. Data for September 14, 2011 is the thicker red line that snakes near the high. There is simply no justification for the type of quote data that underlies this growth. Only the computers spamming these bogus quotes benefit when they successfully trick other computers or humans into revealing information, or executing trades. This is not progress. Progress is almost always accompanied by an increase in efficiencies. This is completely backwards.

And to anyone who might say:

"To my knowledge there's been no proof shown that high-frequency trading has been detrimental.", we'd like to submit this paper as Exhibit A. We think that a 10-fold increase in costs without any benefits would be considered "detrimental" by most business people. We think the regulators would agree with us as well. In fact, they already have on this very topic:

Section I.C.4 of Reg NMS (page 30) states:

- Accordingly, one of the Commission's most important responsibilities is to preserve the integrity and affordability of the consolidated data stream.

And from the same document (page 410):

- But in those limited contexts where the interests of long-term investors conflict with short-term trading strategies, the conflict cannot be reconciled by stating that the NMS should benefit all investors. In particular, failing to adopt a price protection rule because short-term trading strategies can be dependent on millisecond response times would be unreasonable in that it would elevate such strategies over the interests of millions of long-term investors – a result that would be directly contrary to the purposes of the Exchange Act.'

nanex.net

Jim |