Northwest Natural Gas Company (NWN)

ONEOK Partners, L.P. (OKS)

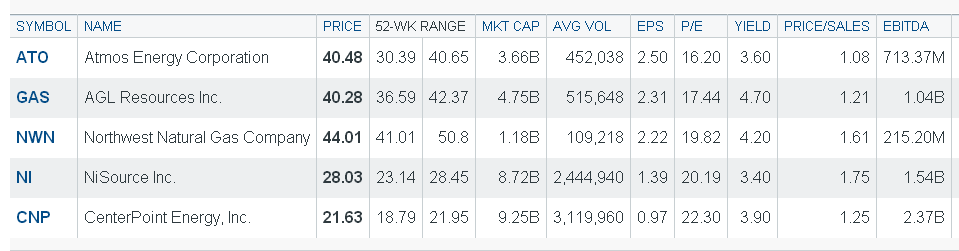

Paul of those stocks you listed these two caught my eye. NWN is still priced a bit high at 18 Forward PE. At 16 PE or 17 PE I may start a position. I need to add this one to my current watch list. From the list below ATO & GAS still have the lowest PE and GAS beats out on it's current yield. I presently own both ATO & GAS. I noticed that Grommit added shares (child portions) of ATO, GAS, NI & CNP. I currently own ATO, GAS & CNP. However, many of these utilities are at 52wk highs.

From that list of MLP's, what made you start a position in OKS? I still have a hard to trying to value these so if one looks at the future growth of the distribution, maybe this one is undervalued.

I have been playing around w/ different metrics for these MLP's. Clownbuck looks at the current distribution "yield", it's coverage and the potential to increase the future distribution w/o compromising the coverage (ie keep coverage above 1.1). What about a simple measure of calculating $EBITDA/share and then calculating the $Price/$EBITDA/share, similar to PE. Anything at 10 or less would be a value Buy. 20 or less might be ones to consider especially if new revenue streams are anticipated w/ prior ongoing capital investments.

So, if you compare these two MLP's (both mentioned in that Barron's article) OKS looks like the best value based on Price/EBITDA.

OKS has 219.82M shares EBITDA= $1.6B EBITDA/share = $5.30/share

Price/ EBITDA/share = $52.47/ $5.30/share = 9.9

OILT has 38.9M shares EBITDA= $ 76.64M EBITDA/share = $1.97/share

Price/ EBITDA/share = $48.37/ $1.97/share = 24.6

APL has 56.29M shares EBITDA= $206.36M/share = $3.67/share

Price/EBITA/share = $32.50/$3.67/share = 8.9

If that makes sense then OKS looks quite attractive with it's Price/EBITDA at 9.9. I recently doubled my APL position as it's Price/EBITA/share is quite low at 8.9. OILT has an interesting business model but to me is quite expensive at the current price. FWIW, OILT is up over 20% in the last 30 days. Maybe it becomes one of those "bolt" on acquisitions for somebody like WMB and/or WPZ.

Is this the best way to value MLP's? I guess it also depends how aggressive management is on growing revenues, managing distribution coverage and building new revenue streams (ie "bolt" on acquisitions that are accretive).

EKS |