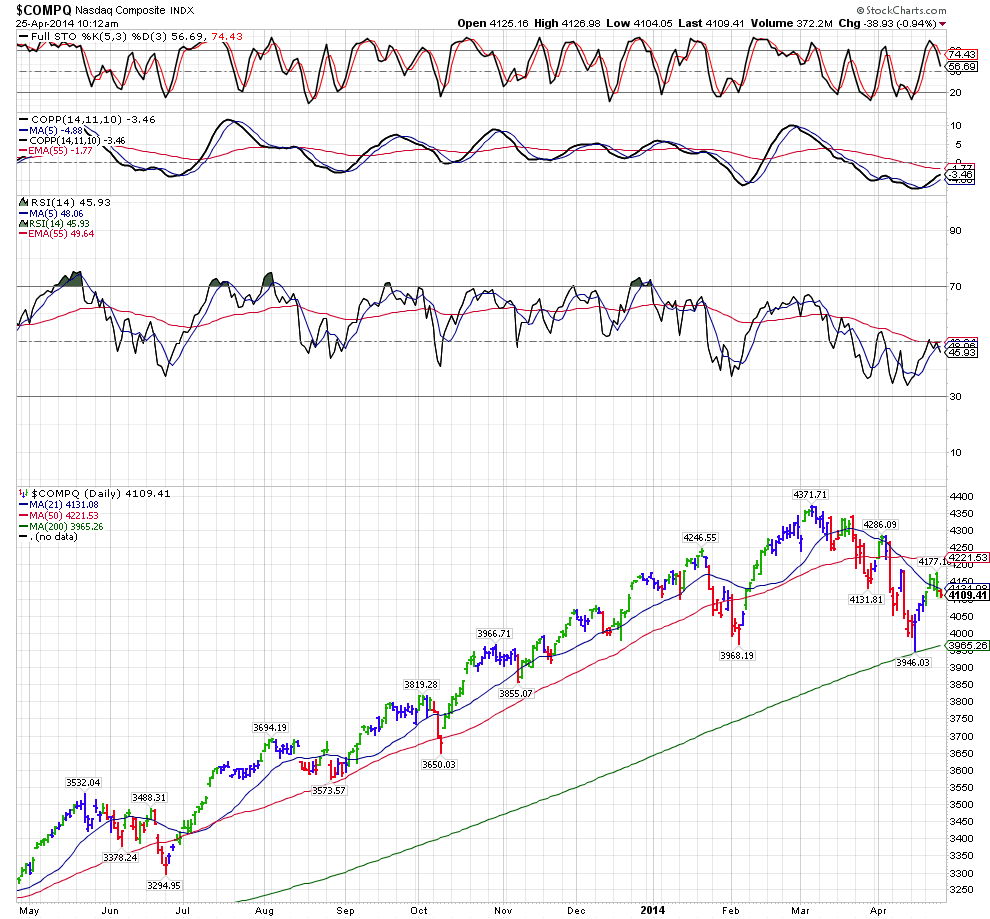

Russia gets a debt downgrade and continues to apply some geopolitical tension. The NASD created the bottom on April 15th when it hit it's 200 DMA.... now for the 3rd time since the March 6th top the NASD has sold off and rallied back above it's 50 DMA only to apparently fake out the longs as it rolls over and is now back below it's 50 DMA.

IBB the biotech sector went below it's 200 DMA and rallied back above it's 50 DMA and now it appears to be slipping below that MA.

\

....interesting to see how stocks like AMZN report strong numbers and yet the stock after initially rallying is selling off. ....interesting to see how stocks like AMZN report strong numbers and yet the stock after initially rallying is selling off.

The market is caught in a tug of war...

Why Markets Are Caught In a Tug-of-War

Mohamed A. El-Erian

comments icon1 time iconApr 25, 2014 7:03 AM EDT

By Mohamed A. El-Erian

There is a simple way to explain the tug-of-war that played out in the equity markets yesterday, over the last few weeks and, indeed, for much of this year. And this simplicity sheds an interesting light on investment strategies that are likely to play a larger role in price determination going forward.

Equity markets spent most of yesterday pushed and pulled by two opposing forces.

Stocks were pushed higher by better-than-expected corporate earnings, stepped-up mergers-and-acquisitions activity, and the continued comforting support of friendly central banks (particularly, the U.S. Federal Reserve and the European Central Bank). Moreover, as confirmed by the most recent data, the U.S. and, to a lesser extent, European economies are strengthening.

It helps that many professional investors have believed -- and quite a few still do (though see the qualification below) -- that climbing stock prices are magnets for increased interest from retail investors who have stayed on the sidelines. The same professionals also consider any sharp market selloff as an attractive opportunity to buy on dips, a strategy that has worked well for them so far.

Yet all is not well for the equity markets, and that reality has been a counterweight that has pulled back indexes. Yesterday’s spike in Ukrainian tensions serves as a reminder of geopolitical instability that, under a plausible set of conditions, could tip Europe and the global economy into recession. Valuations are also an issue, as is the Fed’s continued effectiveness in maintaining a sizable wedge between high equity prices and the more sluggish economic fundamentals underlying everything else.

Looking forward, an increasing number of professional investors are likely to gradually pivot away from targeting general equity market returns (the “beta” of the market) to one or more of three strategies: portfolios that are driven by more concentrated individual stock selection; reducing overall equity beta of portfolios by putting on general market hedges against specific long positions; and gradually accumulating higher cash balances to partially insulate their portfolios.

As this process continues, the equity markets may well lose some of the support that has proven so critical in blunting the scope and scale of price pullbacks in recent months. If this indeed occurs, investors may find out that they are underwriting a lot more price volatility than they currently realize.

Mohamed A. El-Erian at M.El-Erian@bloomberg.net.

John |