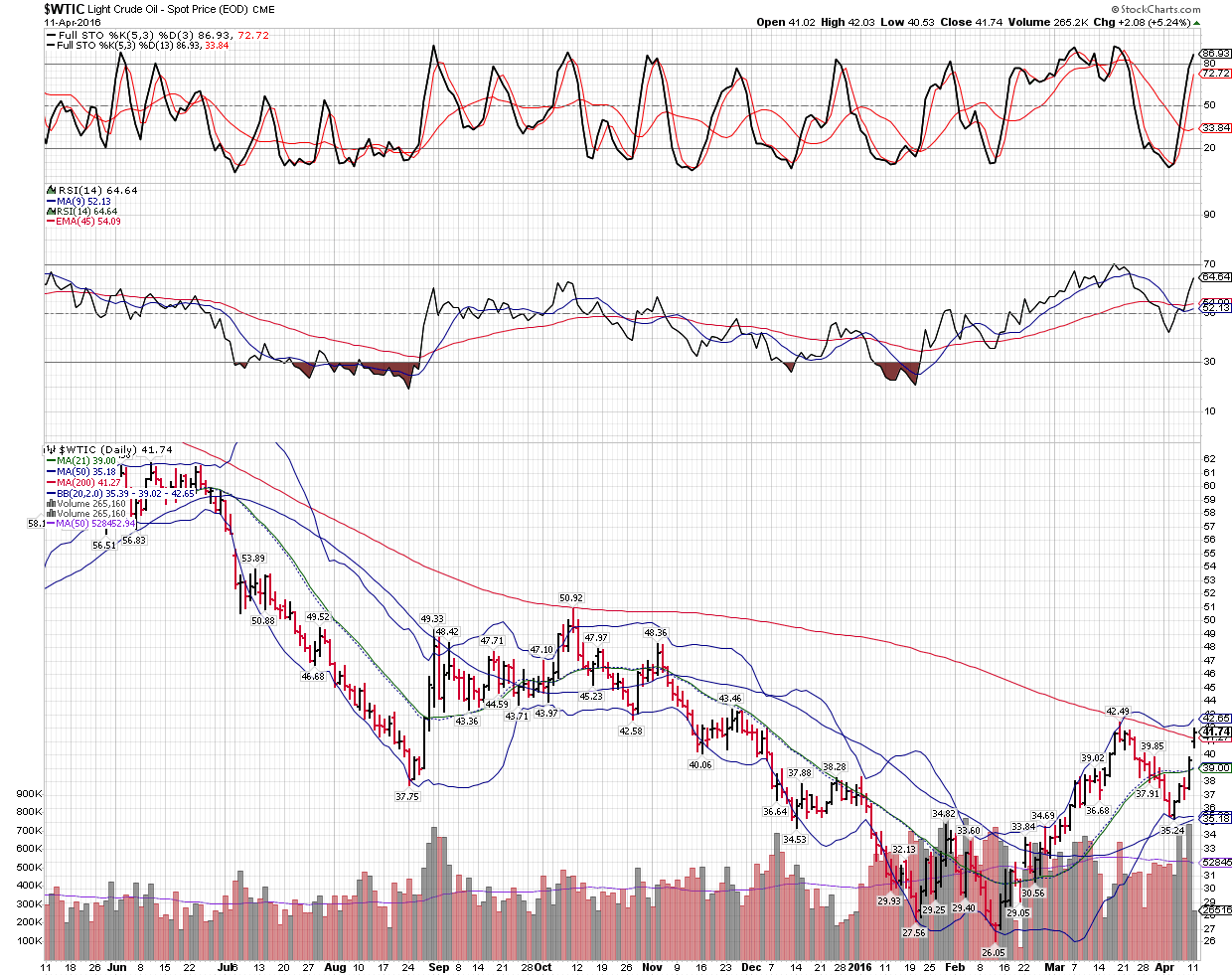

WTIC crude open interest in June just grew larger than May at the end of today's session I noticed tonight. Thus the lead month from a real algorithmic viewpoint is now June and is crude is a trading at $41.65 at the close... $41.65 at this moment which is a $1.38 more than most are looking at .

and daily crude has closed above 200 dma as a result...

That will give the market a bullish pop when everyone puts June in their systems.......

to the options skew... Delta hedging, a neutral strategy should tilt toward the upside so long as the call premiums are cheaper.

from over on H1's thread the cost of bullish call options is dropping, signaling muted expectations for gains in the stock market over the next three months.

The CS Fear Barometer, which measures the cost of bearish put options relative to bullish call options, rose to a fresh record of 44.7% on Friday. The gauge, which goes back to 1994, is calculated by selling a 3-month 10% upside call on the S&P 500 and using the proceeds to buy downside protection; the barometer’s level shows how far below the current level of the S&P, in percentage terms, an investor has to go to buy a put that makes the strategy’s total cost zero.

Put simply, an investor has to go really far below the current level of the S&P 500 to buy a put option that is as cheap as the call option 10% above the current level of the index. The closer a put is to the current level of the S&P 500, the higher the price.

Friday’s increase in the Credit Suisse Fear Barometer was entirely driven by lower demand for bullish call options on the S&P 500, according to Mandy Xu, equity derivatives strategist at Credit Suisse. Typically, an increase in the index is driven by both higher put demand and lower call demand.

“It’s not so much that people are panicking and buying downside protection, but there’s this extreme pessimism or lack of confidence that the market can go higher from here in the next three months,” said Ms. Xu.

Meanwhile, the stock market’s go-to fear gauge has been languishing. The CBOE Volatility Index, or VIX, added 1.3% to 15.56 on Monday after falling on Friday. The VIX hasn’t closed above its 10-year average of roughly 20 since Feb. 29., and fell to a more-than seven month low of 13.1 on April 1.

To be sure, the VIX measures investors’ expectations for stock swings over the next 30 days, while Credit Suisse’s barometer targets a three-month time period. The divergence between the two illustrates how investors are more worried about the next few months than the next few weeks, as they consider first-quarter earnings and guidance, as well a sluggish global economy and swings in oil prices.

this is short term stuff.

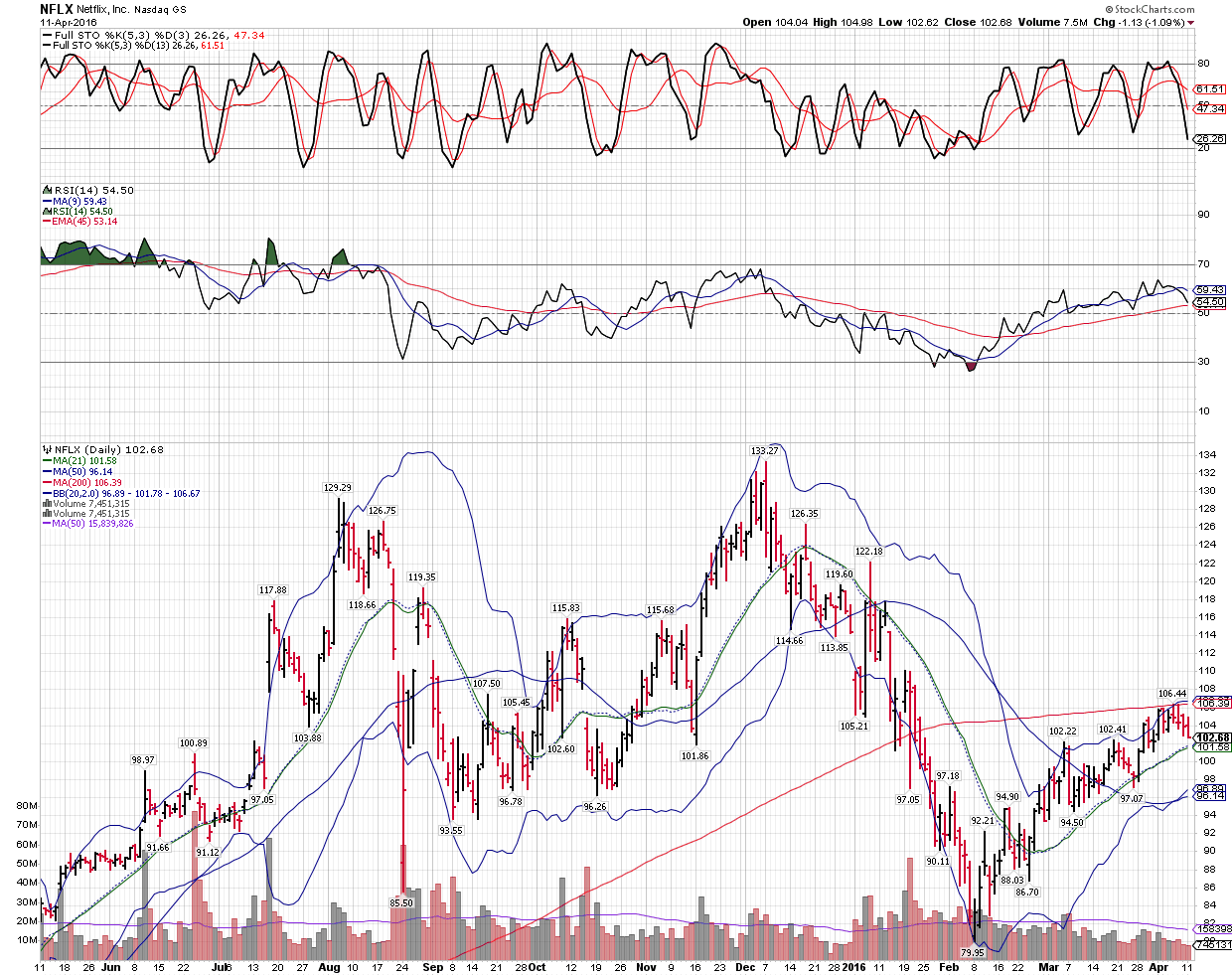

I would lighten up on NFLX as the technical traders shorted it at the 200 dma.... NFLX has a deluge of competition that is arriving as content is exploding . It is not GOOGL or AMZN.

The downside risk out ways the upside by 3 or 4 to 1 over the next 20% imo.

JP

|