Seagate and Western Digital plummet on Friday following weak results/guidance

If Seagate's (NASDAQ: STX) April 13 warning didn't make it clear the hard drive industry is in bad shape, Seagate and Western Digital's (NASDAQ: WDC) latest numbers drive the message home. Both companies saw hard drive shipments drop over 20% Y/Y in FQ3 (calendar Q1), and are guiding for big declines in FQ4 - Seagate's guidance implies a 22% revenue drop, and Western is forecasting the hard drive addressable market will be down 14% Y/Y in Q2 to 95M.

The culprits: Weak PC sales, SSD cannibalization of both PC and enterprise drives, and an enterprise mix shift from high-margin, "performance-optimized," enterprise drives to the lower-margin/higher-capacity drives preferred by the likes of Google, Amazon, and Facebook. Also: Western reports seeing more price pressure in the high-capacity enterprise drive segment (where it leads with the help of its helium drives) thanks to Seagate.

The PC industry's sales declines should eventually narrow, but the other two trends aren't going away. Moreover, some of the product types the PC industry is counting on to boost growth - PC/tablet convertibles, thin-and-light notebooks, and inexpensive " cloudbooks" - often rely on SSDs. Hard drives aren't going to disappear - they'll continue to make far more sense than SSDs for many file, media, and backup storage use cases for a long time - but PC and enterprise/cloud app workloads are clearly migrating to SSDs at a brisk pace, and the arrival of cheaper/denser SSDs relying on 3D NAND flash could accelerate that pace.

Sales pressures are leading to gross margin pressures (particularly for Seagate), even as Seagate/Western cut costs and (following late-2015 Chinese approval) move to integrate previously-acquired hard drive units. Western's pending deal to acquire NAND flash memory giant SanDisk (NASDAQ: SNDK) - it's due to close in FQ4 - is likely a big reason its Friday decline (11.3%) was smaller than Seagate's (19.1%).

Seagate's plunge highlights the risks involved in chasing high dividend yields when the core business of the dividend-payer is deteriorating. Concerns about the sustainability of Seagate's dividend (now carries an 11.6% yield) are now bound to grow. As are questions about whether Seagate will follow Western in making a big acquisition to cut its hard drive exposure.

Even with major post-earnings estimate cuts, Seagate and Western now respectively trade for just 9x and 7x their FY17 (ends June 2017) EPS consensus estimates. The big question is whether future earnings/guidance figures will spark further cuts.

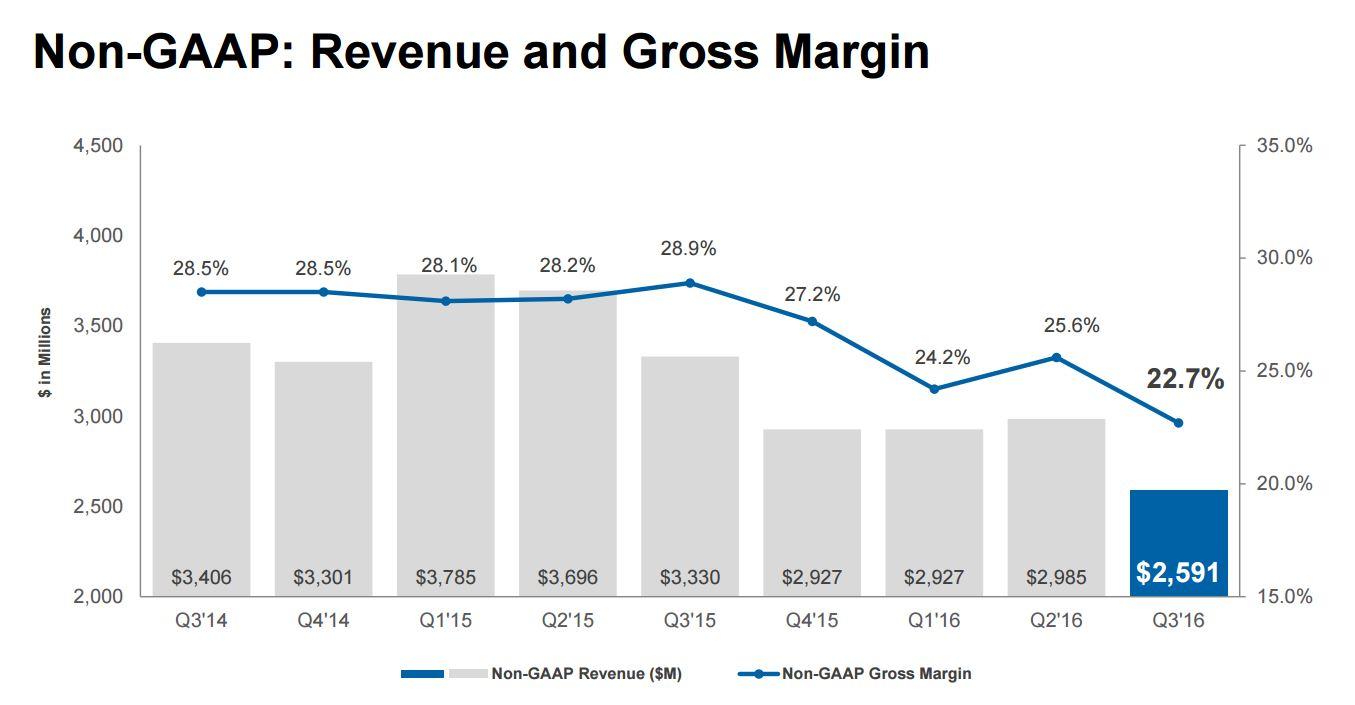

Seagate's quarterly revenue and gross margin. Source: Earnings slides.

|