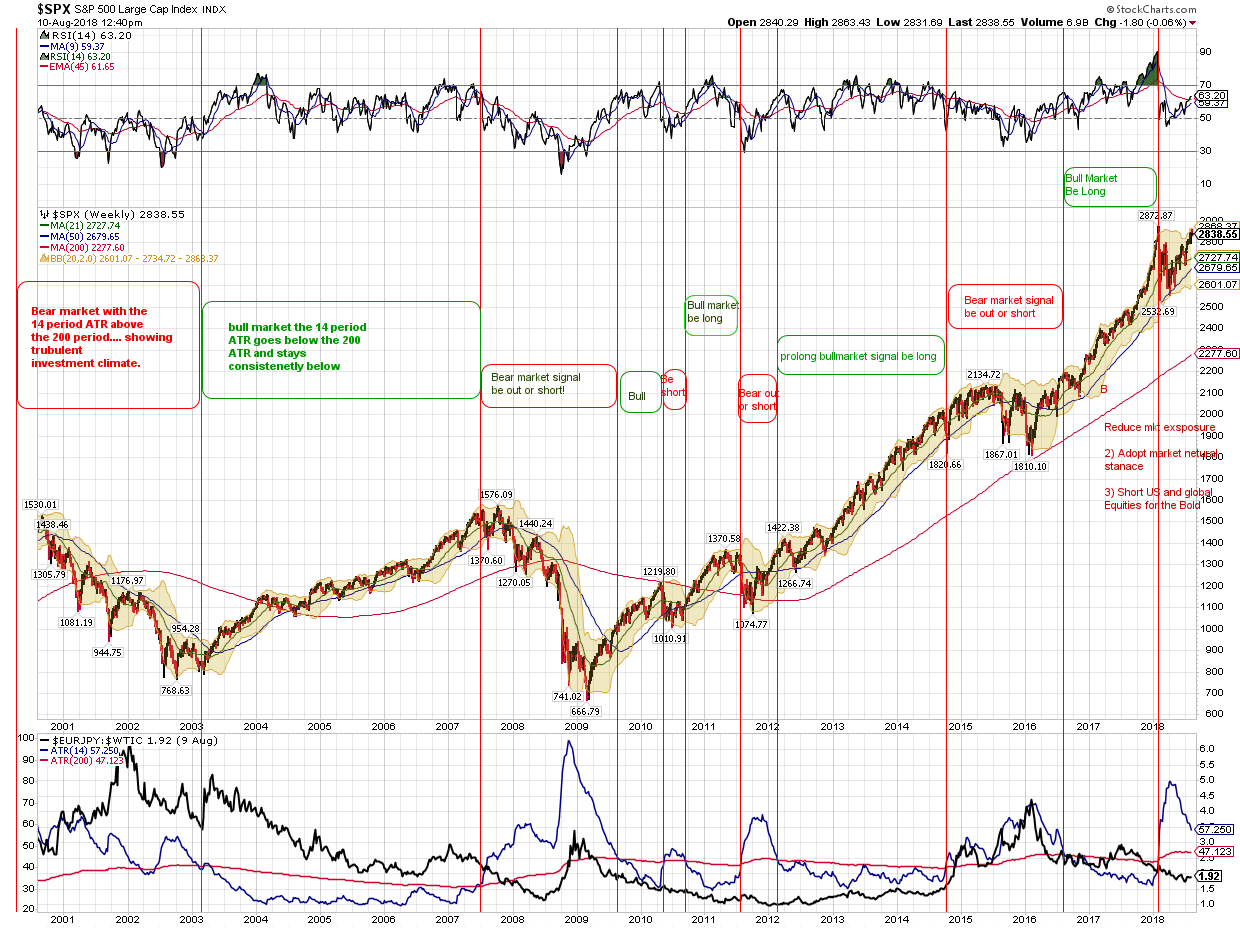

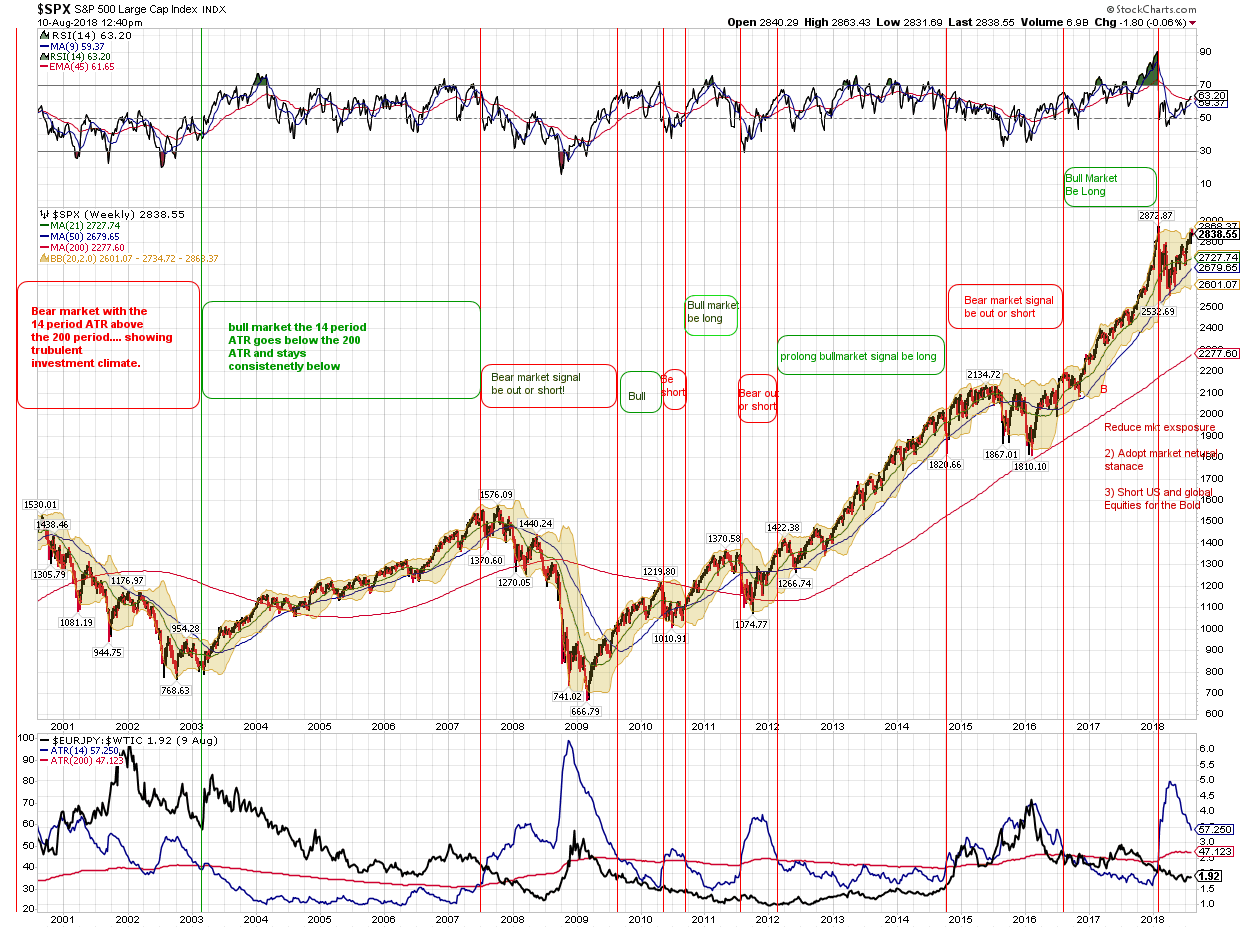

| | | The GFA Global Liquidity Model (which I developed ) has been in a sell mode since the 1st week of February.......

Where the Short VIX and shorting implied volatility in many instruments unwound as soon as the 14 week

ATR Average True Range of my global liquidity model ( which is constructed by taking the EUR/JPY crossrate and taking a ratio of it against $WTIC.) crossed above it's 200 week ATR of the same indicator.

It's completely logical as to why risk assets and the SPX sell off / or at least stop going up when the

14 week ATR crosses above the long term 200 week ATR. Since my / our model is looking at 4 of the deepest markets in the world.... The Euro, The Yen, $WTIC and the USD by default since Crude oil is

denominated in US dollars. The Global Currency markets are the deepest in the world with 6 to 7 Trillion

dollars of Foreign Exchange spot currency trading every day. When you add in Long dated FX,

Global Currency Swaps, Credit Default Swaps, CLO's and other derivatives also trading it creates

an extremely deep market.

The Size and Magnitude of the Global Energy market.... even using just the Crude oil and distillate

portion is Extraordinarily Massive and thus we are dealing with the Beating Heart of Global capitalism.

It goes without saying that the US Dollar is the global Key Currency and it is directly reflected in the

price of Crude.

Thus .........

What is occurring is that global asset prices are fluctuating more dramatically and it creates a risk off

environment for the entire world, where Companies, Governments, Individuals; indeed all sectors of the

economy do not have as much viability as to what there costs and cash flows are going to be, there is more

uncertainty as to whether assets are correctly priced.... the ability to judge whether capital expenditure

and other fundamental economic factors can be properly calculated loses way to much visibility.

And thus in the aggregate there is morecaution and less business, government and consumer confidence

Risk appetite is dramatically reduced.. This logically shows up in the global equity markets and is

typified by the price action of the S&P 500.

What has concerned me for the past 5 plus months is that the long term 200 week average True range of

these global liquidity keys has moved HIGHER showing growing consternation on a longer term basis

as to what is going on with the global economy. and the 14 week Average true range has been

spending way too much time above the long term 200 week ATR.....

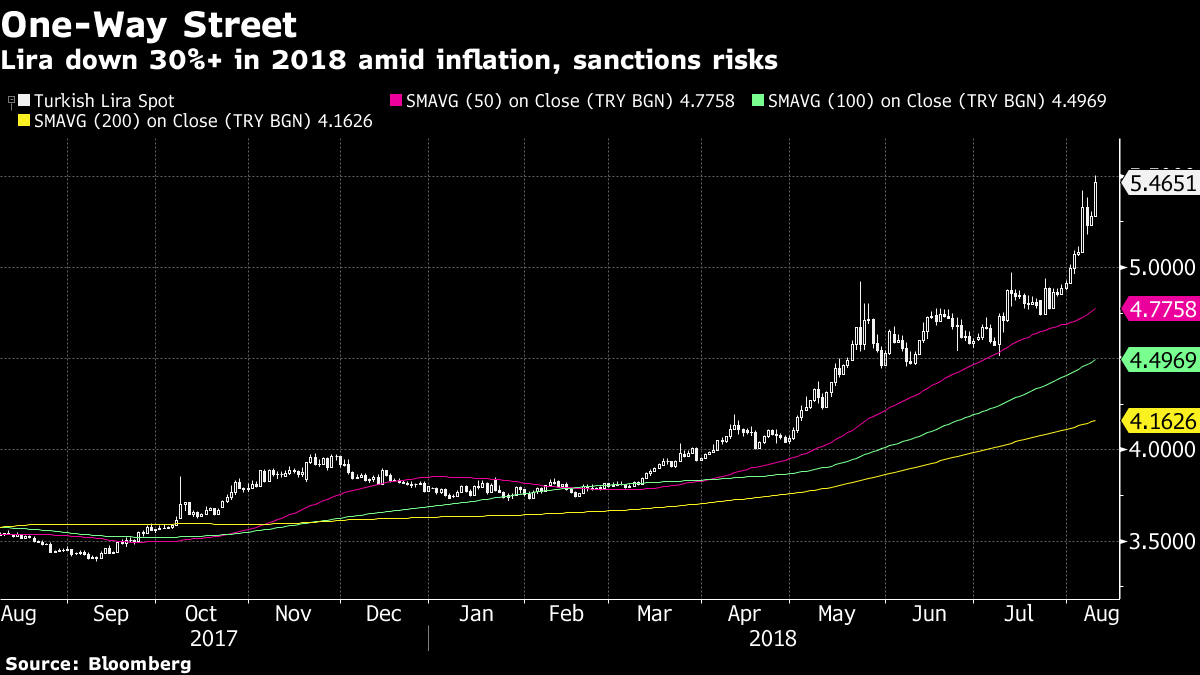

Now we have a potentially very serious global currency crisis on our hands, that the Turkish Lira is only

the tip of the Ice berg of.

The USD index is moving higher at a parabolic rate, while at the same time we see severe weakness in

the Pound Sterling, The Euro which is weakening dramatically down to 1.14. The Chinese Yuan is

sliding, as is the Russia Ruble ... and all emerging currency markets are under pressure since the

US interest rate differentials are so strong compared to the policies of the BOJ, ECB, SNB the BOE

has it's own existential crisis with the potential for a disastrous lack of guidelines in leaving the

European Union and with a no deal Brexit is threatening $34 Trillion in Derivative contracts according

to UK Regulators.

I want to reiterate the following concern:

What has concerned me for the past 5 plus months is that the long term 200 week average True range of

these global liquidity keys has moved HIGHER showing growing consternation on a longer term basis

as to what is going on with the global economy. and the 14 week Average true range has been

spending way too much time above the long term 200 week ATR.....

Also we have seen a 1999 type pick up in the IPO market, as well as a bit of a Merger Mania.....

where some of the prices paid have the appearance of the top of the market cycle.

We do have the positive aspect that the market action since the sever market plunge from January 26th

2018.... straight down to February 9th of 2018 is an "A" wave in Elliott wave terms.... the price action

since then has constituted a "B" wave and that we may be able to get away with a "C" wave correction,

which takes us back down to the SPX lows of 02/09/2018 and that will be able to purge the excesses

and create a reset, at which time we would be good for this fabulous new way of Machine Learning,

Deep Learning, AI, autonomous driving , 5 G communications and a plethora of other exciting new

technologies that are upon us.

Now we have a potentially very serious global currency crisis on our hands, that the Turkish Lira is only

the tip of the Ice berg of.

The USD index is moving higher at a parabolic rate, while at the same time we see severe weakness in

the Pound Sterling, The Euro which is weakening dramatically down to 1.14. The Chinese Yuan is

sliding, as is the Russia Ruble ... and all emerging currency markets are under pressure since the

US interest rate differentials are so strong compared to the policies of the BOJ, ECB, SNB the BOE

has it's own existential crisis with the potential for a disastrous lack of guidelines in leaving the

European Union and with a no deal Brexit is threatening $34 Trillion in Derivative contracts according

to UK Regulators.

Message 31727105

Message 31716802

Wolf Street

“Cliff Edge”

Brexit Threatens $34 Trillion of Derivative Contracts: UK Regulator

by Don Quijones • Jul 24, 2018 • 43 Comment

A high-risk blinking contest no one wants to lose.By Don Quijones, Spain, UK, & Mexico, editor at WOLF STREET.

A messy, no-deal Brexit could throw 48 million insurance contracts and £26 trillion ($34 trillion) of derivatives deals into confusion. Nausicaa Delfas, head of international strategy at the Financial Conduct Authority (FCA), told delegates at a CityUK and Bloomberg event that there were “cliff-edge” risks due to uncertainty over the legality of financial contracts extending beyond the planned Brexit date, in March.

The UK government has already passed regulations that would allow European banks and insurers to maintain their UK operations under current rules after Brexit. So far, the EU has refused to reciprocate, even on a temporary basis.

The EU has also ruled out extending passporting rights to UK financial institutions after Brexit. These rights allow UK-based institutions to sell financial products from the City to investors in the 27 other EU member states. Brussels has also turned down the UK government’s latest proposal for a system of “advanced equivalence” between British and EU financial services.

If the EU continues to reject a temporary permissions regime and no cooperative Brexit deal is signed by the March 29 deadline, big doubts could be raised about the viability of certain derivatives contracts. And that could seriously disrupt an already highly volatile, deeply opaque, largely unregulated $600-trillion dollar industry.

The FCA is not the first regulatory body to warn of such an outcome. At the end of June, the Bank of England said that unless the EU accepted a temporary permissions regime for financial services, up to £29 trillion worth of financial contracts could be declared void in the event of a no-deal Brexit, of which around £16 trillion matures after March 2019.

In its Brexit FAQs handbook the International Swaps and Derivatives Association (ISDA), a global association for market dealers of over-the-counter derivatives, states that it is unlikely that Brexit will lead to a Force Majeure Termination Event, which allows for the termination of a contract or postponement of a party’s obligations or covenants. It does, however, highlight a number of other high-risk events that could transpire in the event of a disorderly Brexit:

“A Cleared Transaction Illegality/Impossibility event… could be triggered by loss of the ability for UK financial services firms to provide investment services cross-border into the EU.”“

A Clearing Member Trigger Event could occur if the loss of passporting rights causes the party which is the Clearing Member to be in default under the rules of an EU Central Counter Party Clearing House ( CCP).”“

A CCP Default could occur if a UK CCP loses its rights to offer clearing services pursuant to EMIR (European Market Infrastructure Regulation), is not granted recognition pursuant to the third country provisions of EMIR… and the rules of that CCP entitle Clearing Members to terminate their transactions with that CCP.

The eventual market impact may result in additional Credit Events pursuant to the 2014 Credit Derivatives Definitions.“Market movements could trigger increased margin calls or trigger provisions linked to ratings.”It’s impossible to overstate just how important the clearings business is to the City of London, or for that matter how important the City of London is to the global clearings industry.

LCH, the world’s largest clearing-house, is based in London. It clears over 50% of interest rate swaps across all currencies, functioning as a middle man collecting collateral and standing between derivatives and swaps traders to prevent a default from spiraling out of control. The role of clearing houses like LCH in global finance has become far more entrenched since the 2008 Financial Crisis. London houses are estimated to handle 75% of all euro-denominated derivatives transactions, equivalent to around €930 billion of trades per day, and 97% of those in dollars.

Representatives for the City of London have called for a deal that preserves the status quo as much as possible. But the EU — and in particular, the ECB — seems more interestedin wresting a larger share of financial clearing from London, something it’s been trying to accomplish for years.

Ironically, it was the European Court of Justice (ECJ) — the same court whose jurisdiction the UK government is now determined to elude — that, in 2015, stopped that from happening on the grounds that the ECB cannot discriminate against an EU member. But if the UK leaves the EU, and thus the ECJ’s jurisdiction, that ruling will no longer be applicable.

The ECB has an obvious motive for seeking to wrest control of the euro-denominated clearing business from the City. In a post-Brexit scenario, the EU would be left with little influence over how clearing houses in the UK are policed once Britain leaves the single market. Yet if a euro-clearing bank failed, it would be the ECB that would have to pick up the pieces.

There’s also a clear commercial incentive at play. Eurex, LCH’s largest continental competitor, based in Frankfurt, announced last year that it would allow banks to share in the profits from clearing. Since then its daily cleared volume in interest rate derivatives has surged from €8 billion to €67 billion — the equivalent of roughly 8% of the global Euro-denominated interest rate derivatives market.

But as impressive as Eurex’s recent growth has been, it’s still dwarfed by London’s clearing operations, which are also growing. The future of those operations are still very much up in the air. If the last two years of negotiations are any indication, either side will be reluctant to back down in this gargantuan blinking contest that could have ugly reverberations far beyond Europe’s economy. |

---------------------------

and Japan has gotten the message that the era of ZIRP, Quantitative Easing and negative soveriegn

yields is detrimental to economic health and they will be embarking upon the normalization of Interest

rates over the next few years...

A Wake-Up Call From Japan

Central banks are withdrawing from ultra-loose monetary policy as gradually as possible, but volatility is still inevitable

Message 31727138

JJP |

|