At this juncture we are starting to short way-out-of-money puts to take advantage of the panic and sense of impending doom, even as we are still naked-short some way-out-of-the-money calls.

Must remember to progress, to close the pincers, to actually buy the equities, to go long calls, way long, for the ferocious-relief slingshot to-da-moon.

The damage has been real. Some structures cracked, and others buckled, but yes, grandparents, selves, bath water, nanny, baby, and pets all chucked out.

The selling has not been sincere. The sincerity shall come, maybe another time, could still be this time.

All very interesting.

In the meantime, some stuff to take into reckoning ...

bloomberg.com

Mizuho Charts Roadmap for an ‘Illiquidity Doom Loop’ in ETFs

Katherine GreifeldMarch 20, 2020, 11:10 AM GMT+2

The rout in European bonds has set in motion what could become an “illiquidity doom loop” in the region’s investment-grade debt ETFs, Mizuho International Plc?????? warns.

While this month’s sell-off has inflicted only minor stress on most exchange-traded products, some have seen extreme gaps form between the price and the value of assets, signifying disorder in the underlying markets. That has reignited anxiety about fixed-income ETFs, which are more liquid than the assets they hold.

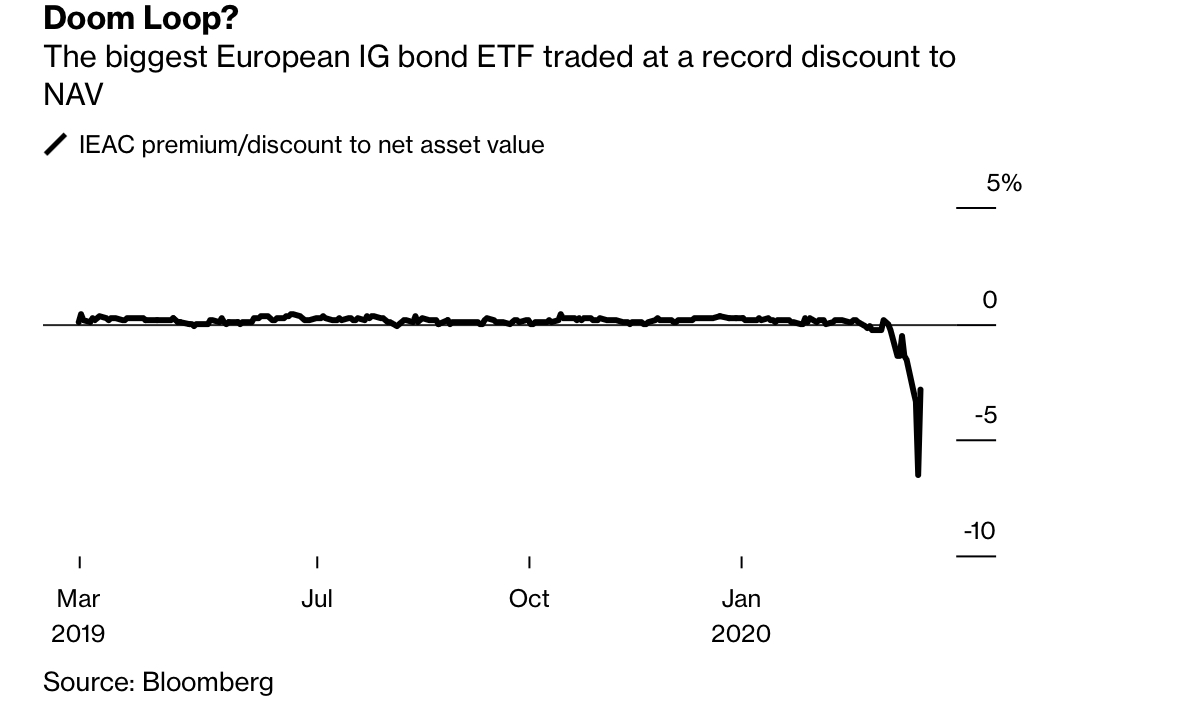

So far, ETFs have largely withstood one of the toughest liquidity tests they’ve ever faced, but Mizuho’s Peter Chatwell sees the beginning stages of the spiral taking place in funds such as the 10.2 billion euro ($11 billion) iShares Core EUR Corp Bond UCITS ETF, ticker IEAC. The ETF’s price traded at a record 6.5% discount to its net-asset value this week.

Doom Loop?

The biggest European IG bond ETF traded at a record discount to NAV

Source: Bloomberg

Rampant volatility in bond markets makes it unappealing for middlemen known as authorized participants to step in to equalize the value of the ETF and the bonds underlying it. In normal times, the price dislocation would spur them to buy shares of a falling ETF in order to exchange them for the underlying bonds with the fund’s issuer, capturing a virtually risk-free profit.

Now, with stress mounting, fears are rising that investors rushing to redeem ETFs will exacerbate a sell-off in the underlying market as authorized participants channel bonds out of the fund. The rampant volatility has made it more difficult to unload the underlying bonds.

Chatwell warns the price dislocation may cause investors to abandon the ETFs, and argues that the region’s central bank should purchase European high-grade ETFs in addition to corporate bonds in order to reduce selling pressure on the underlying bonds.

‘Lose Faith’“ETF investors may lose faith in the ETF products, and sell even more, unless policy makers take action to break the loop,” wrote Chatwell, Mizuho’s head of multi-asset strategy, in a note Thursday. “Given the importance of corporate bond spreads in the transmission of ECB monetary policy to the real economy, we think the ECB should also consider measures to address this problem.”

Concerns about the economic fallout of the coronavirus have upendedfinancial markets, unleashing historical turbulence across the bond spectrum and sapping liquidity.

While many strategists have long argued that such turmoil will cause ETFs to exacerbate the selling, so far the evidence for a liquidity spiral is scant, even as some of the largest fixed-income ETFs continue to trade at steep discounts. IEAC’s discount narrowed to 2.9% in the latest session.

In the eyes of Dave Perlman at UBS Global Wealth Management, ETFs actually diminish the risk of such a doom loop.

“The ETF provides a mechanism for sellers and buyers to meet without selling the underlying bonds,” said Perlman, an ETF strategist. “The ETF wrapper helps slow the risk of the death spiral.”

— With assistance by Yakob Peterseil |