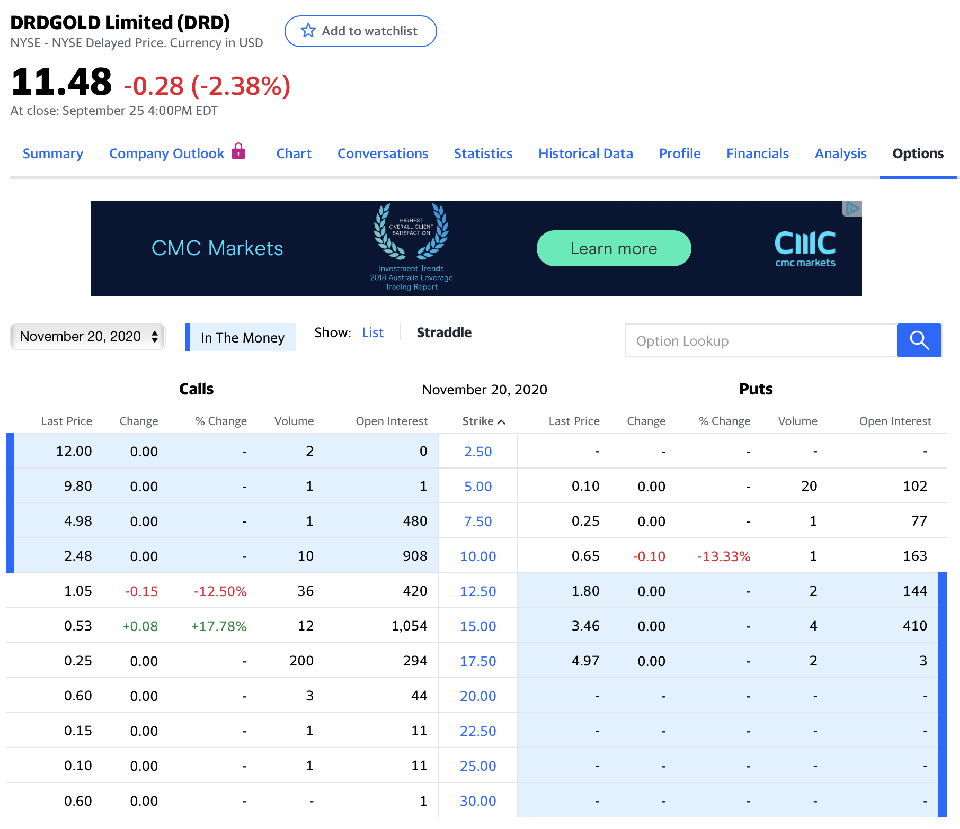

the mathematics of the current setup in DRD November expiration Puts / Calls strike 12.50

the largest concentration of my risk is for now is centered around November expiration, as October positions by and by traded away, and February / May positions still being built up.

Take 12.50 strike as example,

One can buy a share at 11.48 (Friday closing price) and sell a call and a put both at strike 12.50, undertaking to be robbed of a share at 12.50 on / before 20 November, or be force-fed an additional share at same 12.50, all in exchange for combined premium of 1.05 + 1.80 = 2.85, which would be 23% of the 12.50 undertaking

should one be actually force-fed a share at 12.50 on or before expiration day, less the 2.85. net cost of the additional share would be 9.65, and together with the Friday purchased share at 11.48, the average cost would be 10.57 for both shares.

should one instead be robbed of the share bought at 11.48, at price of 12.50 obligated, adding to the 2.85 premium earned, would show a profit of 2.85 + 12.50 - 11.48 = 3.87, which would be 34% return on the single share bought and robbed, for less than 60 days of hanging out

The options are not liquid so larger quantities actually has to be transacted awhile ago, as am now still building 'for the long term' positions in February and May expiration campaigns, when it is far less clear what would actually happen to gold and therefore DRD.

All seems unreasonable. Cannot get these odds at casinos / lotteries.

Of course none of the machinations can save one from a cratering back to 5 per share, thus the bet.

Even more wonderful, that one get to use TSLA premium to finance the wager!

Would be a shame when CEO retires - he is tops as far as I can tell

I do not do the options w/r to TSLA this above way, because TSLA can crater back to below 200, easily, and so I buy calls and sell other calls, in different wallop sizes and same / different expiration dates.

NLY is another good one, not so much because it is volatile, like TSLA, but given that it is steady.

NAK, BBL, RIO, TRQ ...

all just computer gaming, ideally for win-win outcomes |