New Found Gold's big find sparked the ongoing gold rush in Newfoundland...

There are quite a few companies that have shown some evidence of similar styles of mineralization on their properties... the right sorts of rocks... the right indicators minerals... the right structures... and more than a few showing gold exists in other types of deposits... often in higher grades and wider intercepts than is typical for gold these days in other regions... So, lots of potential... in various places... almost all of which will be much slower to develop than will be the case in the few larger properties hold by the better funded companies... Those without the $ to support the rapid pace in exploration you see at New Found Gold... won't be doing very much in altering the perception of their potential... rather than, perhaps, masking it.

So, there's opportunity in the difference... and that extends across the entire region.

But, among the potentials, there are a couple of companies that are directly "on trend" with New Found Gold... that have, at least, some shared potential to participate directly in the continuity of discoveries that are occurring along the same shared fault structures that New Found Gold is exploring.

Labrador Gold and Exploits are the most obvious of those... and they are also fairly well funded. Perhaps include in that lot some of the Crest holdings, if not the Crest/Exploits JV in the Exploits subzone...

In poking at the older information on Newfoundland participants, a few weeks back, I had noted that William Sheriff had an interest there at one time... (Perhaps it was as Golden Predator, or might have been Silver Predator related ?) I didn't follow up on it. But, it popped up again today... and might still prove interesting to follow that history in property ownership, while noting the connection that does exist between Sheriff's interest in Exploits... and the residuals that might remain in the Arizona Gold / Golden Predator merger now as Sabre Gold ? I just don't know how the history of those properties in Newfoundland evolved. But the news recently had Sheriff, at Exploits, signing this August 26 PR as interim President and CEO...

EXPLOITS COMMENCES DRILLING AT JONATHAN’S POND, AND PROVIDES MID-SEASON EXPLORATION UPDATE

Shortly before firing himself, on September 16, while signing this one...

EXPLOITS ANNOUNCES JEFF SWINOGA AS CEO

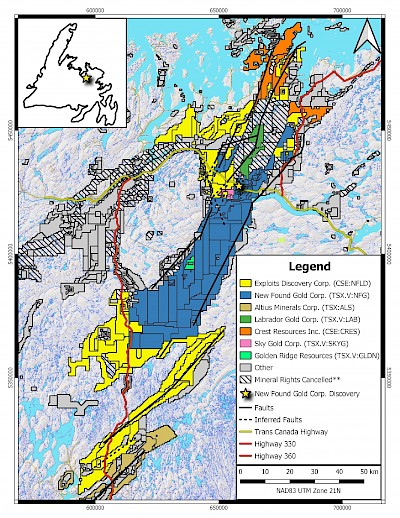

There are also a number of smaller companies that don't have the largest land positions, as Exploits does... but there is a lot of acreage proximal to the trends... that shows up in grey on the Exploits produced map of the region showing who has what... showing claims that are staked... without showing who owns them ? Some of that is probably claims still held by the prospect generators... some of it will be privately held... and some will probably have deals done and emerge later...

Seems like it might be worth finding out more about the acreage that's been claimed but isn't yet attributed to any company... on the Exploits map. Work to do.

Some of that potential is also held in smaller holdings, by smaller companies, with odds favored by being among those most directly associated to the known potential... if among the least well known. But, we're still at such an early stage, when the market is more focused on participants amassing acreage "nearby" enough... while hoping that quantity in holdings will help capture some bit of the hoped for potential. But, without adequate tools to enable better focused evaluation, (and with a market shifting its focus away from bothering anyway) there is isn't yet a shift to parsing quality in smaller scale potentials, and, whether or not their proximity is a useful proxy for that potential remains an open question.

Opportunity there, too, perhaps... as the error in assumption exists that without already having a stack of drill holes proving values exist in particular places.... places without them must all be of equal (non-existent until proven) value ? But, while the NI43-101 does try to insist that "value" should work that way... reality doesn't have any need to comply in locating value only where holes have been drilled. There are a couple of smaller spots that are not "proximate to" but are directly on the same proven trends... that are being considered as moose pasture now... for want of holes drilled proving IF they have a share in the mineralization known to exist along the trend, or not ? And, a couple of those... have all the known indicators in the right kind of geology, but also with relevant quantities of gold reported in soils, grab samples, trenches, and with visible gold and high grades in outcroppings ?

The most directly associated have small holdings on the same structures... and parallel adjacent structures.

They might be "close but no cigar ?"... or, perhaps they might not have figured out how to look in the right places, yet... or how to target the right structures on trend at the right depths... where there's possibly better potential for both wider intercepts and higher values ? The same criticism applies to NFGC, too, who haven't yet reported very many holes drilled on structure along trends as they extend below 200 meters...

Others are just moving a bit more slowly, perhaps... even with solid history in the occurrences reported... also making it clear that the delays in assays will be forcing most of the regions' exploration efforts to be dragged out over longer periods of time... with many if not most of the better prospects in the Camp not even slated to turn drills until this fall, and into the winter...

It seems worth the effort in poking at them to see who holds those smaller patches... the ownership of which the larger and most recent Exploits map really doesn't help with very much...

I'll post more when and as I get it figured out...

|