watch & brief, into the brave new world happenings

Quote ...

Fast e-CNY rollout on the merchants, but slow pickup in user acceptance

China is accelerating pilot testing of the world’s first central bank-backed digital fiat currency, officially known as the e-CNY, and has granted access to nearly 10% of its population. Our channel checks in Shanghai unveiled wide merchant acceptance of the new digital Rmb in both offline and online outlets. However, user acceptance still seems low for now, as the benefit of e-CNY seems only marginal to users. We expect the central bank to encourage circulation of e-CNY in more apps (especially Wechat Pay and Alipay) in the near future. In our view, the wider rollout of e-CNY would marginally benefit leading banks but represent a long-term risk to third-party payment companies on user data.

China is leading the way in testing a digital currency

The PBOC began research into the e-CNY in 2014, and has since launched several pilots, including introducing digital yuan “red packets” in 10 places.

Most recently, e-CNY testing has been expanded into wider use cases with commercial banks and internet companies promoting the account opening and usage. The e-CNY could also be piloted at the Beijing Winter Olympics.

As of October 2021, there were 3.5 million outlets to use e-CNY, 123 million retail e-CNY wallets opened, and Rmb56bn of transactions have been facilitated.

On-the-ground checks on e-CNY promotion and acceptance

Leading banks and internet companies are promoting the account opening and usage of e-CNY. Banks are offering small gifts offline and coupons online to attract new users, while internet companies such as Meituan are offering e-CNY lottery.

The rollout of e-CNY has processed well on the merchant side. About 70% of shopping malls in Shanghai accept e-CNY, according to a bank officer. We see almost all supermarkets and convenient stores accept e-CNY. Online outlets are widely accepting e-CNY for designated uses.

However, user acceptance appears to lagging behind. Only one or two users use e-CNY in a 7-11 store per day. The benefits of e-CNY look only marginal to users, while e-CNY is cheaper, safer and functional in absence of connections.

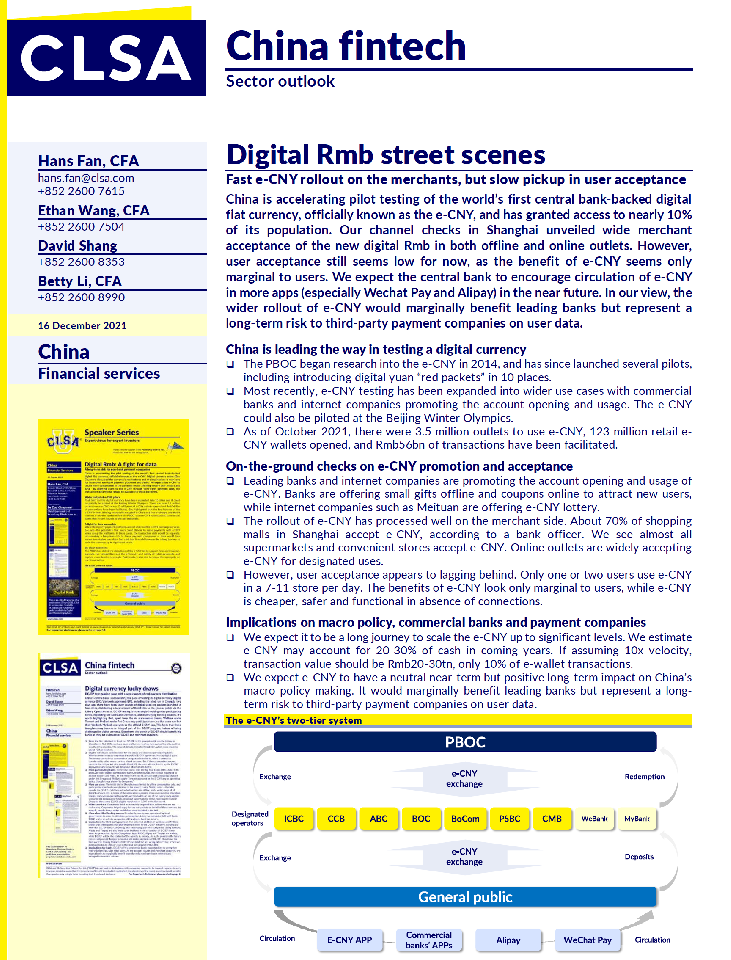

Implications on macro policy, commercial banks and payment companies

We expect it to be a long journey to scale the e-CNY up to significant levels. We estimate e-CNY may account for 20-30% of cash in coming years. If assuming 10x velocity, transaction value should be Rmb20-30tn, only 10% of e-wallet transactions.

We expect e-CNY to have a neutral near-term but positive long-term impact on China’s macro policy making. It would marginally benefit leading banks but represent a long term risk to third-party payment companies on user data.

Unquote

|