Column: LME copper stocks plunge again as metal heads to China: Andy Home

mining.com

Reuters | October 19, 2022 | 8:33 am Intelligence Markets China Europe Copper

The amount of available copper in the London Metal Exchange’s (LME) warehouse network has halved over the last eight days.

Headline stocks of 139,000 tonnes may look healthy enough but a string of daily cancellations means that 48% of that tonnage is now awaiting physical load-out, leaving just 72,950 of live stocks.

The stocks grab looks strange, given the rapidly darkening outlook for demand as Europe heads into recession and US manufacturing growth brakes sharply.

But the clue lies in China, where a squeeze on the Shanghai Futures Exchange (ShFE) has generated a scramble for metal.

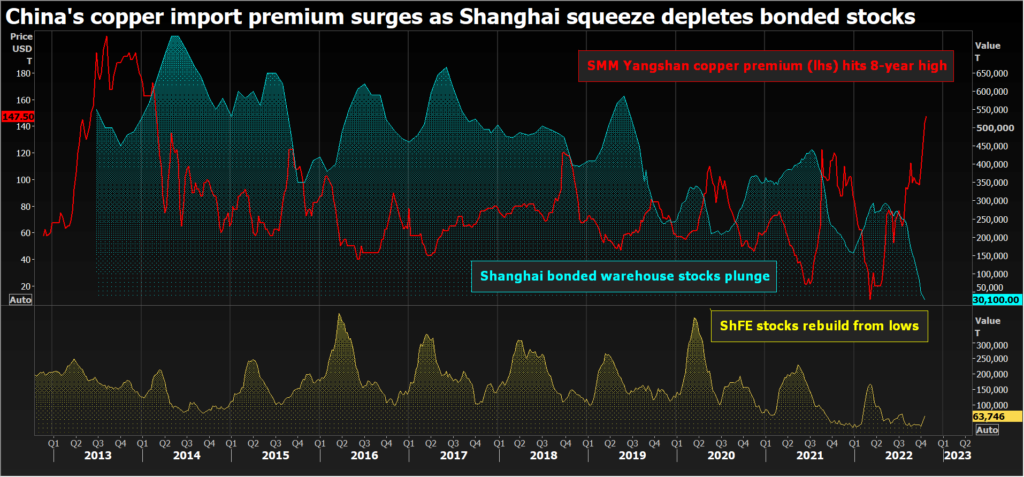

Shanghai squeeze

The ShFE copper contract has been characterized by low inventory and rolling tightness for some time. But things have come to a head since the market reopened after the Golden Week holidays and in the run-up to the October contract’s expiry on Monday.

Market open interest surged to 454,074 contracts at the end of last week, the highest level of participation since 2015, as the front part of the curve tightened.

Deliveries against short positions have been accelerating. Total registered ShFE stocks more than doubled over the holiday period to 63,746 tonnes with on-warrant inventory jumping from 3,729 to 25,588 tonnes.

More have arrived this week, and on-warrant stocks mushrooming to 70,547 tonnes as of Tuesday.

Shanghai is now acting as a magnet for available copper units both in China and the rest of the world.

Yangshan yanks the supply chain

It’s clear the first point of call for Shanghai shorts has been the copper sitting in the city’s bonded warehouses.

Shanghai’s international copper contract, traded via the International Energy Exchange (INE), is backed up by such stocks. Registered inventory plunged from 88,861 to 28,389 tonnes over the Golden Week holidays, by some margin the biggest change in INE stocks since the contract was launched at the start of 2021.

Local data provider Shanghai Metal Market (SMM) assesses broader bonded stock levels, sometimes termed “social stock”. These too have plummeted to 30,100 tonnes from a March peak of 293,500 tonnes.

As bonded stocks rapidly deplete to fill on-shore ShFE warehouses, physical premiums are in turn rising to attract more metal from the international market.

The Yangshan copper premium, a useful proxy for China’s spot import demand, has soared to $147.50 per tonne over LME cash, its highest trading level since 2013.

The high premium for Chinese delivery is now sucking in metal from the rest of the world, including LME warehouses in Asia, where all the cancellation activity has taken place over the last week or so.

Disrupted supply?

The scramble for Shanghai metal is surprising given China’s refined copper imports have been running at a fast pace in recent months. Net imports of 2.31 million tonnes in the first eight months of the year were up almost 10% in the same period of 2021.

However, these inflows have bypassed both bonded and on-shore warehouses to refill a depleted domestic supply chain after an extended bout of destocking due to record high prices earlier this year.

It is probable that the troubled trade house Maike Group is also somehow in the Shanghai copper cocktail right now.

The company, which is actively selling assets to forestall a liquidity crunch, is a copper powerhouse, typically handling around a quarter of China’s import volumes every year.

Its ongoing restructuring, which includes the liquidation of copper stock, is likely disrupting normal trade flows through the bonded warehouse system.

London’s Russian dilemma

China’s strong call on copper is being felt in London, where falling LME stocks have rekindled time-spread volatility.

The benchmark cash-to-three-months spread has been in backwardation since the middle of September and the cash premium was valued at a hefty $60 per tonne at Tuesday’s close.

The micro tightness continues to clash with the bearish macro picture, which has kept outright three-month copper under pressure close to its July low of $6,955 per tonne, last trading at $7,375.

The micro-macro divergence looks set to accentuate as LME stocks are stripped for shipment to China.

There’s an extra complication for the LME, which has launched a discussion paper on whether to suspend deliveries of Russian-brand metal.

Over 60% of LME copper stocks at the end of September were Russian metal. It’s quite possible that the ratio is about to go up further as total stocks fall and what’s left is increasingly concentrated on the European ports of Hamburg and Rotterdam.

Both are obvious shipping destinations for Russia’s two copper producers and they currently hold a combined 42,425 tonnes of live stocks, equivalent to 58% of the rapidly diminishing total.

Neither location has been touched by the recent spate of cancellation activity, which has understandably played out at Asian locations within much faster reach of Shanghai shorts.

While this week’s huge flows of aluminum into LME warehouses have inevitably turned the spotlight on Russian aluminum producer Rusal, copper stock movements may become a bigger problem sooner. |