Your post is to an oil and gas patch veteran. So here is a bit about what I know. Retired plenty of time to write stuff.

Spent over 45 years in the industry (engineer), all facets mostly upstream. And I've also worked in LNG plants, many times. Turbines, compressors, loading arms, etc. My main area of expertise is prime movers and auxilaries, the whole gamut. This includes power production, especially modern gas turbines and generators. Oil and gas patch uses a lot of power, which costs money. Worked on some drilling rigs, mechanical equipment. Down hole and production geology not my area of work, but not w/o some knowledge.

It was a wonderful career, the oil and gas industry is an amazing industry. The use of technology is vast and deep, just as deep as what exists in the aerospace and space industries. And technology does not stand still. The deep offshore drilling and production is in a world of its own. A prime mover related example. When the space shuttle was being developed there were serious rotor stability problems with the high pressure oxidizer pumps. Several engines were blown up on test stand, and the early versions put into use were power limited. I worked on these same problems on high pressure centrifugal gas compressors and centrifugal pumps. And some of the people that contributed to solutions and understanding did work in the oil and gas industry, Dr. Dara Childs from Texas A & M for one, met him personally.

My favorite was offshore upstream. I worked the gamut but mostly on prime movers associated with offshore oil and gas processing, awa transportation. So I know about what is gas, what is condensate, what is NGL, what is LNG, what is oil, vapor pressures, separation schemes, liquifying methods, some refining, some chemical processes, and so on. Awa those little molecular formulas involving hydrocarbons ... C x H y.

No regrets on career path, but if I had to do it over I might consider drilling. The deep offshore drilling is fascinating, and the movie Deepwater Horizon was done fairly well (imo). BP of course said otherwise. Watched it 3 or 4 times, followed all the action relating to capping on the web.

A lot of changes occurred over those 40 plus years, a couple of the biggest areas with effects imo are related to environmental regulation awa safety areas. Not a tree hugger, but there were reasons for this, and a lot of positives have come about as a result.

My post was primarily about TA, not the fundamental side. But since you brought it up I will comment. I do have opinions maybe with some basis, on the ongoing issues. But opinions are just opinions, the future will tell the story.

There are still separate oil and gas wells. And it has always been the case that gas and condensate is produced with oil wells. Sometimes a lot, sometimes not so much on old wells. Likewise a lot of gas wells produce condensate, there are however some gas or near gas only wells. Drilling and fracking for gas is not a small undertaking, neither is drilling and fracking for oil in shale, or anywhere else. Afa I know drilling, fracking and well maintenance is the most expensive side of the production related business. If you want to produce longterm, it is a continual necessity. And if you don't keep it up, it will eventually affect your production.

In the 80's peak oil awa price controls were all the rage. Never believed in that due to new technology coming along, all but forgotten now. The Oil and Gas industry came through with shining colors. I follow the rotary rigs in operation figures, out of interest. Going to mention something about this, here is a very good LT graph of gas and oil drilling rigs in operation. eia.gov

An example of new technologies. I worked on a giant field in the North Sea for several years. Originally the recovery factor was thot to be less than 20 % of the oil in place. Today I think it may be near 70 % projected, due to new technologies, mostly drilling related. A good place to find more oil for production has in more recent times been in old fields.

I could probably write several pages, but I'll try to summarize.

- I already commented on gas vs. oil wells and all that stuff. I'll add there is nothing new about LNG. Been around for years. The first LNG plant in the US was put into operation in 1969 in Kenai AK. researchgate.net I have been in that plant several times. It is now afa I know mothballed, due primarily to lack of gas. I do not know why it took so long for LNG to proliferate in the US, lack of markets until more recently maybe. LNG requires liquification, shipping and receiving/regassification terminals. If there is a lack of the latter, it cannot go.

- US last year was largest world exporter of LNG afa I know. Australia (worked on LNG there too), Qatar and Russia all follow closely. I have wondered if Russian LNG is sanctioned, I don't thinks so, they purposely may have missed this to help Europe out. Plus some of the most recent Russian LNG projects were heavily invested with western money, Yamal for example.

- As a side note LNG plants are pretty efficient, one of the processes used is the COP cascade process, with which I am familiar. As I recall it is near 95 % efficient. Then there are losses involved in transport, receiving and regassification. Not sure but I suspect the overall efficiency is probably around 85 %, relative to using NG only.

- Now to rig counts, I remember the big peak in the 80's well, awa the following bust. I was working primarily in TX, OK and NM, drilling rigs everywhere. Then suddenly they were all parked in fenced off lots. From about mid 80's to 2000 it was really tough in the patch. W/r to more recent past, this is not a political post. Many opinions on SI, but fact is that no matter who recent pres has been rigs in use has declined, and is still falling. The last boom was a big one, the last bust about Covid time brutal, especially in my neck of the woods.

- It is not fake news, the US is energy self sufficient, we do import some crude, but on net we export more liquid hydrocarbons than we import. And we are huge exporters of LNG, and still growing. Oil and gas production at record highs. If you would have told me this would happen with present rig in operation trends, 25 years ago, I would have found it hard to believe. But it is happening, says something imo for new technology awa productivity.

- Why the current low gas prices? Just part of the cycle in process, and partially related to a lot of oil that has come online in the Permian. With the oil comes gas, and it has to go somewhere. Flaring long since not allowed.

- Oil companies keep their break even costs close to chest, and may not really know. My personal opinion is that gas prices are currently below break even, and that is why the rotary rig rates are still falling in the gas patch. Oil harder to say, depends on where you are at. I live way up north in the Arctic, I think breakeven up here is probably about where oil is priced at. Overall I think margins are pretty tight, and again this is why oil rig rates continue to fall.

- Speculation on my part, which is rig rates will probably continue to fall, especially if prices stay low or continue to fall, and put in a big bottom. Seems to be the way the patch works. They over invest and go crazy in boom times, and under invest during the busts, when it is cheaper to do work. Like part of the planning is back asswards. There is probably also some truth to the fact that current regulations impede the drilling side. It takes forever to get approvals for major projects these days, Willow on the North Slope but an example. Took years, people continually brought up court actions/suits, until it finally ended. Was not totally dependent on who was in office, regardless of who was, it had to work its way through the courts and due process.

- Devon is probably typical of the production side, ~ half their revenue is from black oil, ~ 1/4 from gas, ~ 1/4 from NGL's. NGL's are low vapor pressure condensates, used primarily as feed stocks for various petrochemicals.

- Now to EV's, I'll start by saying that in my early days I worked on a lot of big prime mover stuff designed in the 30's and 40's. Mostly all gone now. The drivers for improvement over the years were always the same, with a few exceptions. Hp per unit weight, efficiency, and maintenance required. An exception possibly related to environmental regs, now all these prime movers, mainly diesels and gas turbines are subject to environmental regs, to meet regulated emission requirements, mainly Nox and CO. Old equipment was mostly purely mechanical, with few or no wires attached. All new equipment is much more complex, complicated controls, sensors and chit everywhere. A bit similar to how autos with ICE's have evolved, for similar reasons.

- BEV's depending on size are typically 2.5 to near 5 times as efficient at using energy, as compared to ICE counterparts. Moreover that energy can come from oil, gas, nuclear, hydro, coal or renewable sources. A typical BEV is probably near 90 % efficient, a typical ICE vehicle probably less than 30 %. ICE's been around for one hundred plus years, I don't see a magic development to change this, most of the heat of combustion goes out the radiator and tail pipe.

- BEV's utilize a lot of electrical stuff, special type of induction motors, and some gearing. Very little maintenance required normally, over lifetime of the vehicle.

- BEV batteries this always comes up. Yes they are expensive, but a typical Tesla warranty is 8 yrs and 150 K miles. Lifetime nearly for many. caranddriver.com If you drive a lot and are unlucky enuff to have to replace, the fuel and maintenance savings should more than make up for the cost.

- BEV's if desired offer tremendous improvement in power density, there are standard BEV's available with ~ 1000 Hp to the wheels. Seems a bit more than necessary for me but to each his own.

- A lot of US based posters may think the world revolves around the US. It sort of does in many ways but the global auto market is huge, US total about 1/5 of that. spglobal.com

- US is lagging but much of rest of world is going BEV, including China, Europe, India and Japan. Might be different for them if they produced the amount of gas and oil that the US does, but they don't.

- I have no fight in the BEV vs the ICE, I own ICE's now. Both are functional. Maybe a BEV is in my future, to me it is just an improvement in overall technology, related primarily to successful integration of more recent technologies.

- Nearly 70 % of each barrel of crude is used for transportation fuel, mainly gasoline and diesel. And most of that is gasoline. Each BEV sold on a global basis is like a little cut into future crude oil demand, the math is not complicated.

- QS is probably the leader in the US in solid state battery development, seems less than 2 yrs out now. Battery prices should drop, and the energy density will take a quantum step up. The electrification process will continue and broaden out. Vehicles could see 1000 mile ranges, which is a bit designer choice. Lee might some day buy an electrified Bobcat. If he lives long enough.

- There are other issues, namely the proliferation of solar and wind power. I believe this is the fastest growing area of grid power production in the US right now, followed by natural gas fired turbine power. Nuclear is dead for a while, coal is dying probably forever, in the US anyway. Being a turbine engineer I have followed the wind turbine industry, young and vibrant it is. Use of deep offshore wind turbines is expanding and they are no longer small things. 15 Mega Watts and larger. The industry is still evolving rapidly and the practical size limit is unknown. I think China recently installed an 18 Mega Watt unit. China, India and Europe are heavily investing in solar and wind power.

- Here is a major international oil company that thinks crude is in long term trouble, they have used their offshore technology to develop deep water floating offshore wind turbines, and plan to be a leader. Hickups along the way. They recently commissioned some of these to power some of their offshore oil and gas platforms. equinor.com

Summary and a Few Final Comments.

I am long term bullish natural gas (and LNG), US and world wide. Grid demand will continue to grow and renewables are but part of the total answer. In the US about 40 % of the grid power comes from gas turbine power plants, and is growing. These plants are fairly clean and efficient, maybe from 55 % to 80 % efficiency, depending on exact type of plant. The high efficiencies are in part what helps them to be clean.

I have a small investment in NG, my timing was too early. But not too worried about it, I go for more LT stuff.

Nothing is free. A modern turbine driven power plant is capital intense, as are wind turbines. But once the gas fired power plant is in operation, the fuel cost overwhelms everything else and is continual. It is probably 90 % of the cost of operation. A 13 MWatt liquid fired turbine consumes near 900 gallons of diesel per hour. Do the math, a large plant is 1000 Mwatts. Big big numbers dollar wise.

I've done more fuel usage costs than I care to think about. It is a big deal to anyone operating a lot of power, because of the cost.

Crude oil has always been king in the oil patch, and for integrated production companies always the primary source of revenue. I am less bullish the LT future for crude oil, given the global proliferation of EV's. US is currently lagging but EV's are here to stay as well. Very interesting times we live in, and am looking forward to see how all this develops.

In regard to the crude to natural gas price ratio, we will see. I think it has merit, because it has its basis in energy equivalent.

There is another LT aspect that the general public awa as investing public is probably not aware of.

A gas turbine is called a gas turbine because the primary working medium is in the gaseous state. But the fuel can be liquid, like on aircraft. Some have even been fired on coal dust, but it is too abrasive to use, the turbine would not last long.

The desired fuel in power plants is generally natural gas, because the maintenance is a bit less. And in some locations there may be environmental regs that favor natural gas.

But some of these gas turbine driven power plants are equipped with dual fuel gas turbines. They can in some cases switch from using natural gas to liquid (generally diesel) on the fly. And since the plants are very sensitive to fuel costs, they use what is overall cheapest. Natural gas now the big winner at present. I do not have a good idea of % of plants that can readily fuel switch.

So I for one would not be surprised if in the future, natural gas and crude oil will compete with each other, to some extent. It is something to be aware off.

Tweets

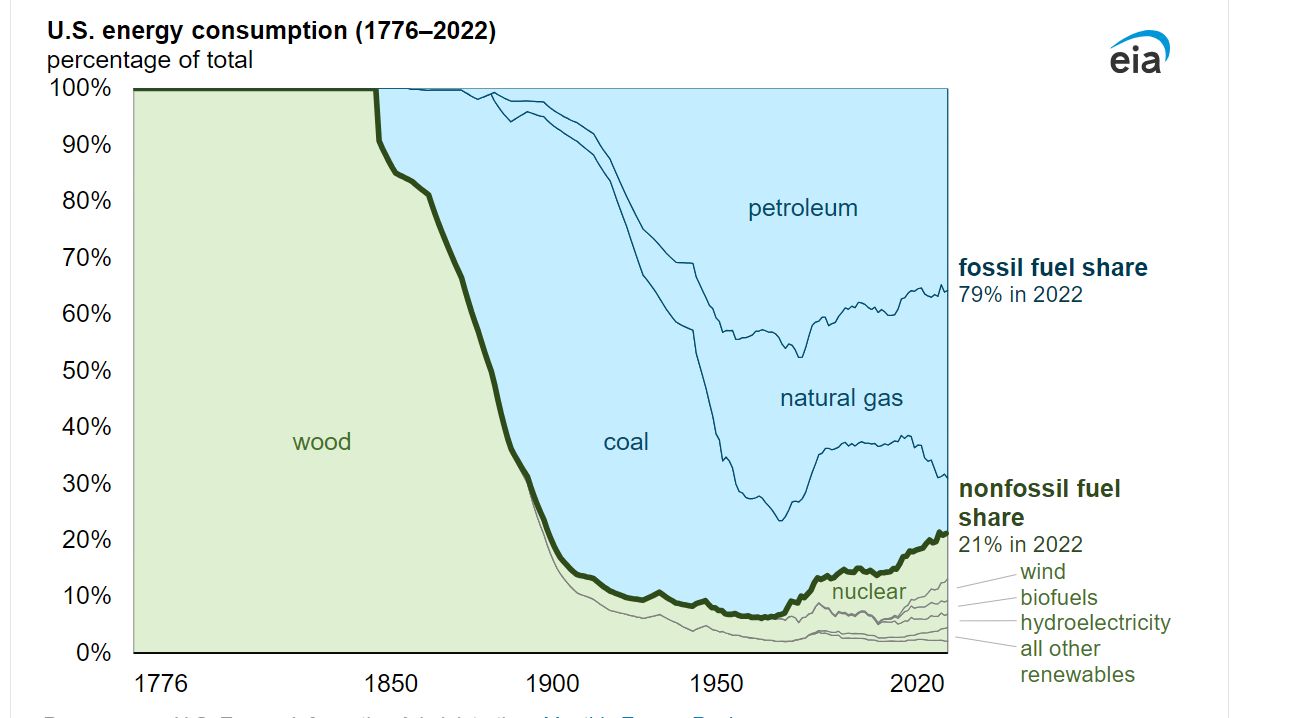

I thot this was interesting. In the old days the US was settled with wind power (sailing ships) and then the settlers used wood 100%. Then came coal, petroleum, natural gas, nuclear and a bit of this and that. And now the use wind and solar is increasing the non fossil fuel share again.

Plus as a % of the mix, petroleum is declining, natural gas is expanding.

eia.gov

|