METALLA REPORTS FINANCIAL RESULTS FOR THE SECOND QUARTER OF 2025 AND PROVIDES ASSET UPDATES

newswire.ca

News provided by Metalla Royalty & Streaming Ltd. Aug 14, 2025, 16:30 ET

(All dollar amounts are in thousands of United States dollars unless otherwise indicated, except for shares, per ounce, and per share amounts)

TSXV: MTA

NYSE American: MTA

VANCOUVER, BC, Aug. 14, 2025 /CNW/ - Metalla Royalty & Streaming Ltd. ("Metalla" or the "Company") (TSXV: MTA) (NYSE American: MTA) announces its operating and financial results for the three and six months ended June 30, 2025. For complete details of the condensed interim consolidated financial statements and accompanying management's discussion and analysis ("MD&A") for the three and six months ended June 30, 2025, please see the Company's filings on SEDAR+ ( www.sedarplus.ca) or EDGAR ( www.sec.gov). Shareholders are encouraged to visit the Company's website at www.metallaroyalty.com.

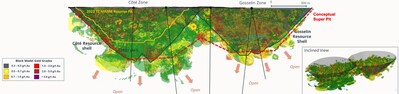

Figure 1: Long section of Côté and Gosselin conceptual super pit (Source: IAMGOLD Q2 2025 Presentation) (CNW Group/Metalla Royalty & Streaming Ltd.)

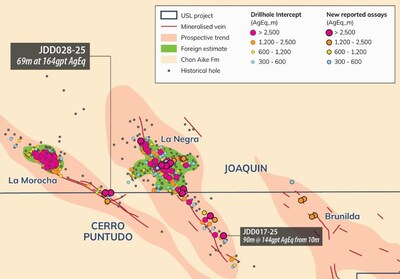

Figure 2: Plan view map of significant intercepts at Joaquin (historical and new) (Source: Unico quarterly activities report dated July 30, 2025) (CNW Group/Metalla Royalty & Streaming Ltd.)

Brett Heath, CEO of Metalla, commented, "The second quarter of 2025 marked another important milestone in Metalla's growth, highlighted by the successful closing of our inaugural revolving credit facility and recommissioning of the Endeavor Mine. The facility lowers our cost of capital and materially enhances our financial flexibility to continue scaling our business. We are also pleased that, in its first month of production, the Endeavor Mine has achieved its operating costs targets while producing 5,398 dry metric tonnes of silver-lead concentrate in July. We anticipate our first cash flows in the third quarter. Further and subsequent to quarter end, we are delighted to see Hudbay's joint venture announcement for a 30% interest in Copper World by Mitsubishi Corporation and Equinox Gold's announcement that Castle Mountain has been accepted into the United States Federal Permitting Improvement Steering Council's FAST-41 Program as we believe both updates are key to progressing these assets to a construction decision."

COMPANY HIGHLIGHTS

Key Company highlights for the three months ended June 30, 2025, and subsequent period include:

- On June 24, 2025, the Company entered into an agreement with the Bank of Montreal and National Bank Financial for a revolving credit facility ("RCF") of up to $40.0 million with an accordion feature for an additional $35.0 million in availability, subject to the satisfaction of certain conditions. Concurrent with entering into the RCF, the Company also fully repaid and retired a C$50.0 million convertible loan facility with Beedie Investments Ltd.;

- On June 26, 2025, the Company announced the release of its 2025 Asset Handbook outlining the Company's gold, silver, and copper royalties and streams, as well as Mineral Reserve and Mineral Resource data for the underlying properties. The Asset Handbook is available on the Company's website;

- On July 9, 2025, Polymetals Resources Ltd. ("Polymetals") announced that it had successfully refurbished and commissioned the Endeavor mine ("Endeavor") and processing plant with first concentrate shipment scheduled for July. On August 4, 2025, Polymetals announced that Endeavor was now meeting its operating costs after its first full month of production and had produced 5,398 dry metric tonnes of silver-lead concentrate during July and had received concentrate prepayments of A$11.6 million;

- On August 11, 2025, Equinox Gold Corp. ("Equinox") announced that its Castle Mountain Mine Phase 2 Project ("Castle Mountain") has been accepted into the FAST-41 program. FAST-41 is a federal permitting framework designed to streamline environmental reviews, improve interagency coordination, and increase transparency. Acceptance into the program is expected to enhance regulatory certainty through a defined permitting schedule that may reflect reduced permitting timelines. Based on the permitting timeline posted to the FAST-41 project dashboard on August 8, 2025, the federal permitting process should be completed in December 2026; and

- On August 13, 2025, Hudbay Minerals Inc. ("Hudbay") announced a $600 million strategic investment from Mitsubishi Corporation ("Mitsubishi") for a 30% joint venture interest in Copper World. The contribution from Mitsubishi will consist of $420 million upon closing and a $180 million matching contribution payable no later than 18 months following the closing. Mitsubishi will contribute 30% of the ongoing costs beginning August 31, 2025, and will participate in the funding of the definitive feasibility study as well as the final project design, project financing, and project construction for Copper World.

Key operating and financial metrics for the Company include:

|

| Three months ended

|

| Six months ended

|

|

| June 30,

|

| June 30,

|

| June 30,

|

| June 30,

|

|

| 2025

|

| 2024

|

| 2025

|

| 2024

| Revenue from royalty interests(1)

|

| $2,695

|

| $875

|

| $4,416

|

| $2,130

| Net loss

|

| $(1,603)

|

| $(1,491)

|

| $(2,334)

|

| $(3,223)

| Adjusted EBITDA(2)

|

| $1,485

|

| $165

|

| $2,351

|

| $243

| Total attributable GEOs(2)

|

| 840

|

| 401

|

| 1,468

|

| 1,025

| Average realized price per attributable GEO(2)

|

| $3,289

|

| $2,332

|

| $3,104

|

| $2,173

| Average cash cost per attributable GEO(2)

|

| $8

|

| $17

|

| $10

|

| $12

| Operating cash margin per attributable GEO(2)

|

| $3,281

|

| $2,315

|

| $3,094

|

| $2,161

|

(1) For the methodology used to calculate attributable Gold Equivalent Ounces ("GEOs"), see Non-IFRS Financial Measures.

| (2) Adjusted for the Company's proportionate share of NLGM held by Silverback.

|

ASSET UPDATES

Below are updates for the three months ended June 30, 2025, and subsequent period to certain of the Company's assets, based on information publicly filed by the applicable project owner:

Tocantinzinho

On July 8, 2025, G Mining Ventures Corp. ("G Mining") reported second quarter gold production of 42.6 Koz and that the processing plant reached nameplate capacity of 12,890 tonnes per day ("tpd") over 30 consecutive days. G Mining also reaffirmed their 2025 production guidance of 175 to 200 Koz with 56% of output concentrated in the second half of the year as higher-grade ore becomes accessible deeper in the pit.

Metalla accrued 309 GEOs from Tocantinzinho for the second quarter of 2025.

Metalla holds a 0.75% Gross Value Return ("GVR") royalty on Tocantinzinho.

Wharf

On August 6, 2025, Coeur Mining, Inc. ("Coeur") reported second quarter gold production of 24.1 Koz. Gold production in the second quarter increased 18% quarter-over-quarter driven by higher gold grades. Exploration expenditures for the second quarter were $4 million with expansion and infill drilling programs at Wedge and North Foley completed during the quarter, results met expectations with both zones expected to contribute meaningfully to year-end reserve and resource estimates. Coeur indicated that exploration priorities in the third quarter include infill drilling at Juno, following up on 2024 expansion drilling, which extended mineralization approximately 500 feet to the northwest. Coeur reaffirmed its full year guidance for 2025 at Wharf of 90 – 100 Koz gold and announced it expects to spend $13 to $17 million on capital expenditures to materially extend the mine life as well as other investments which are expected to be required to convert the Juno and North Foley deposits into reserves.

Metalla accrued 279 GEOs from Wharf for the second quarter of 2025.

Metalla holds a 1.0% GVR royalty on the Wharf mine.

Aranzazu

On August 5, 2025, Aura Minerals Inc. ("Aura") reported second quarter production from Aranzazu of 22,281 GEOs (as defined by Aura), marking a 9% increase over the first quarter of 2025. The increase was driven by higher grades and improved recoveries, attributed to greater stability in the grinding-flotation circuits and the introduction of more effective reagents. During the quarter, infill drilling at the Glory Hole zone focused on converting Inferred to Indicated Mineral Resources in deeper parts of the deposit. Drilling confirmed continuity of the mineralized skarn, with highlight intercepts of 5.86% copper, 1.3 g/t gold, and 62 g/t silver over 25.5 meters, and 0.95% copper, 0.33 g/t gold, and 10 g/t silver over 26 meters. At Esperanza, drilling continued to confirm mineralization continuity, with notable results including 2.3% copper, 0.88 g/t gold, and 20 g/t silver over 6.4 meters, and 0.72% copper, 0.27 g/t gold, and 5 g/t silver over 3.35 meters.

On May 5, 2025, Aura highlighted the release of an updated National Instrument 43-101 - Standards of Disclosure for Mineral Projects ("NI 43-101") technical report for Aranzazu on April 1, 2025, which confirmed a 10-year mine life and projected average annual production of 28.1 million pounds of copper, 25.2 Koz of gold, and 652 Koz of silver.

Metalla accrued 175 GEOs from Aranzazu for the second quarter of 2025.

Metalla holds a 1.0% Net Smelter Returns ("NSR") royalty on Aranzazu.

La Guitarra

On July 31, 2025, Sierra Madre Gold & Silver Ltd. ("Sierra Madre") announced closing of the final tranche of a C$19.5 million private placement, with net proceeds to be used to expand the capacity of the La Guitarra mine and conduct a detailed exploration program, including drilling in the East District of the La Guitarra property.

On April 29, 2025, Sierra Madre announced the commencement of underground mining at the Coloso mine, located within the Guitarra complex. The Coloso mine is located 4 kilometers from the Guitarra processing plant and was previously mined allowing Sierra Madre to restart operations with minimal pre-production expenditures and seven months ahead of schedule. Sierra Madre noted that the Coloso Mineral Resource grades are 1.7 times higher in silver and 1.2 times higher in gold than the Guitarra vein, which served as the initial mining front at La Guitarra.

Metalla accrued 30 GEOs from La Guitarra for the second quarter of 2025.

Metalla holds a 2.0% NSR Royalty on La Guitarra, subject to a 1.0% buyback for $2.0 million. The Company's NSR royalty covers 100% of the Guitarra complex, including the Guitarra, Coloso, and Nazareno mines.

La Encantada

On July 8, 2025, First Majestic Silver Corp. reported production of 49 oz of gold from La Encantada in the second quarter of 2025. During the quarter, one underground rig completed 2,546 meters of drilling on the property.

Metalla accrued 26 GEOs from La Encantada for the second quarter of 2025.

Metalla holds a 100% GVR royalty on gold produced at the La Encantada mine limited to 1.0 Koz annually.

Endeavor

On August 4, 2025, Polymetals announced that Endeavor was now meeting its operating costs after its first full month of production. Endeavor produced 5,398 dry metric tonnes of silver-lead and zinc concentrates during July and has agreed to a second pre-payment with its offtake partner of A$11.6 million. Polymetals announced that zinc concentrate transports from site will commence mid-August with the first ocean shipment scheduled for early September. The operational ramp-up remains on track, with mining of the high-grade Upper North silver ore expected to begin in August.

On July 9, 2025, Polymetals announced that it had successfully refurbished and commissioned the Endeavor mine and processing plant. Mining and processing activities were ramping up to planned levels, with production of silver-lead-zinc concentrate well underway. Polymetals reported that first ore was treated on June 7, with a total of 36,066 dry metric tonnes of commissioning ore processed, grading 103 g/t silver, 3.72% zinc, and 2.31% lead. Site activities remain on track to process an average of 65,000 dry metric tonnes of ore per month during the second half of 2025. Exploration during the second quarter focused on the Carpark target and Endeavor South. At Endeavor South, drilling intersected encouraging alteration, veining, and visible sulphides, including elevated copper values, supporting the potential continuation of the mineral system south of the Endeavor main lode.

Metalla holds a 4.0% NSR royalty on lead, zinc and silver produced from Endeavor and expects its first cash flow in the third quarter of 2025 at which point it will be classified as producing.

Gurupi (formerly CentroGold)

On July 23, 2025, G Mining reported that a Brazilian federal court had nullified legacy environmental licenses granted in 2011 to a prior operator, resolving a longstanding legal dispute over the Gurupi Project and providing a clean regulatory path forward. The ruling allows G Mining to initiate a new environmental licensing process, including the preparation of a full environmental impact assessment and engagement with the National Institute for Colonization and Agrarian Reform. G Mining also announced a budget of $2 to $4 million has been allocated to Gurupi for 2025, with a larger budget to be mobilized in the second half of the year upon receipt of the necessary exploration permits.

Metalla holds a 1.0% NSR royalty on the first 500 koz of production, 2.0% NSR royalty on the next 1 Moz, and 1.0% NSR royalty thereafter on Gurupi.

Côté-Gosselin

On August 7, 2025, IAMGOLD Corporation ("IAMGOLD") reported in their second quarter MD&A that approximately 19,700 meters of drilling were completed at the Gosselin deposit during the quarter (31,700 meters year-to-date). The program was focused on increasing confidence in the existing resource and converting a significant portion of Inferred Resources to the Indicated category. IAMGOLD plans to drill a total of 45,000 meters at Gosselin in 2025, however this program could increase. In addition, 6,500 meters of the 20,000-meter infill drill program commenced in the second quarter of 2025 to improve resource confidence in the northeastern extension of the Côté deposit. According to IAMGOLD, the results of the Gosselin exploration program are expected to be included in an updated Mineral Reserve and Resource estimate next year and will inform the updated technical report which IAMGOLD announced will consider a larger scale Côté gold mine with a conceptual mine plan targeting both the Côté and Gosselin zones over life of mine. The updated technical report is expected to be completed by the end of 2026.

IAMGOLD also reported gold production at Côté gold mine in the second quarter was 96 Koz, as the mine continues to ramp up following the start of production in 2024. Mining activities continue to expand the pit and increase the volume of blasted ore in the pit to provide flexibility in supporting the planned mill feed with reduced handling. Production at Côté Gold in 2025 is expected to be in the 360 – 400 Koz range.

Metalla holds a 1.35% NSR royalty covering less than 10% of the Côté Mineral Reserves and Resources estimate in the northeastern portion of the pit design, as well as 100% of the Gosselin Mineral Resource estimate.

Castle Mountain

On August 11, 2025, Equinox reported that Castle Mountain has been accepted into the United States Federal Permitting Improvement Steering Council's FAST-41 program. FAST-41 is a federal permitting framework designed to streamline environmental reviews, improve interagency coordination, and increase transparency. Acceptance into the program is expected to enhance regulatory certainty through a defined permitting schedule that may reflect reduced permitting timelines. Based on the permitting timeline posted to the FAST-41 project dashboard on August 8, 2025, the federal permitting process should be completed in December 2026. Equinox further stated that with FAST-41 permitting status in place, that it has initiated study updates and project optimization to align with the permitting timeline and position the project for a timely construction decision. Based on a 2021 Feasibility Study, the project is expected to produce 200 Koz gold annually over a 14 year mine life, totaling 3.2 million ounces.

On May 7, 2025, Equinox reported in their first quarter MD&A that they are continuing to advance engineering and permitting for Castle Mountain. Equinox reiterated its expectation that the lead agencies will publish a notice of intent in 2025, which would commence the formal permitting review process, and announced that a memorandum of understanding has been signed among the project lead agencies to prepare the joint Environmental Impact Statement/Environmental Impact Report ("EIS/EIR"). Equinox expects the EIS/EIR stage of formal environmental analysis to occur throughout 2025 and 2026.

Metalla holds a 5.0% NSR royalty on the South Domes area of Castle Mountain.

Taca Taca

On July 23, 2025, First Quantum Minerals Ltd. ("First Quantum") reported in their second quarter MD&A that the Environmental and Social Impact Assessment ("ESIA") continues to be reviewed by the Secretariat of Mining of Salta Province. First Quantum is awaiting a consolidated technical report from provincial authorities, following an independent evaluation conducted by SEGEMAR (Argentinian Geological and Mining Service) in the fourth quarter of 2024. First Quantum also stated that it is preparing an updated NI 43-101 Technical Report for Taca Taca, and plans to submit an application for the RIGI regime, a new incentive regime for large investments created by the Argentine government.

Metalla holds a 0.42% NSR royalty on Taca Taca subject to a buyback based on the amount of Proven Reserves in a feasibility study multiplied by the prevailing market prices of all applicable commodities.

Joaquin

On July 29, 2025, Unico Silver Ltd. ("Unico") announced the results of continued drilling at Joaquin, aimed at expanding mineralization and converting the Foreign Resource Estimate (as defined by Unico) to a maiden JORC compliant resource. Step out drilling at La Marocha SE returned a highlight intercept of 163 g/t AgEq (as defined by Unico) over 69 meters. Further, initial infill drilling completed at Joaquin confirmed historical mineralization and highlight previously under-modelled high-grade zones with a highlight intercept of 522 g/t AuEq over 28 meters.

Metalla holds a 2.0% NSR royalty on Joaquin.

San Luis

On July 29, 2025, Highlander Silver Corporation ("Highlander") reported assays results testing a conceptual open pit target called Bonita at San Luis. All seven holes intersected high grade broad mineralization with highlight intercepts of 4.92 g/t gold and 16.52 g/t silver over 23.1 meters and 3.7 g/t gold and 17.47 g/t silver over 14.5 meters. Highlander plans to expand the drill program to two drill rigs upon receipt of regulatory approval.

Metalla holds a 1.0% NSR royalty on San Luis.

Fifteen Mile Stream

On July 24, 2025, St Barbara Limited ("St Barbara") reported that the prefeasibility study for the 15-Mile processing hub remains on track for completion in March 2026. The study is evaluating the integration of Cochrane Hill into the previously proposed 15-Mile and Beaver Dam combination, with an increased throughput scenario. St Barbara also highlighted continued improvements in the resource development and permitting environment in Nova Scotia, where gold was added to the list of Provincial Strategic Minerals.

Metalla holds a 1.0% NSR royalty on the Fifteen Mile Stream project, and 3.0% NSR royalty on the Plenty and Seloam Brook deposits.

Fosterville

On July 30, 2025, Agnico Eagle Mines Ltd. ("Agnico") reported that Fosterville produced 49.6 Koz of gold in the second quarter of 2025, higher than planned due to higher grades at Harrier and a change in mining sequence at Phoenix.

Metalla holds a 2.5% GVR royalty on the northern and southern extensions of the Fosterville mining license and other areas in the land package which are not currently in production.

Copper World

On August 13, 2025, Hudbay Minerals Inc. ("Hudbay") announced a $600 million strategic investment from Mitsubishi Corporation ("Mitsubishi") for a 30% joint venture interest in Copper World. The contribution from Mitsubishi will consist of $420 million upon closing and a $180 million matching contribution payable no later than 18 months following the closing. Mitsubishi will contribute 30% of the ongoing costs beginning August 31, 2025, and will participate in the funding of the definitive feasibility study as well as the final project design, project financing, and project construction for Copper World. The joint venture is expected to close in late 2025 or early 2026. Hudbay stated that this transaction secures a premier long-term strategic partner and validates the longer term value of Copper World as a world-class copper asset.

On June 11, 2025, Copper World Inc., a wholly-owned subsidiary of Hudbay announced the selection of several companies to conduct feasibility studies and drive early stage project development for Copper World, a milestone that marks the continued advancement of the fully permitted mine. Hudbay stated that this development is structured under an integrated project delivery model which fosters more efficient planning, enhances risk mitigation, and streamlines execution across all phases of the project lifecycle. Hudbay also announced that a coalition of local union building trades recently announced a letter of commitment for the construction of Copper World.

On May 12, 2025, Hudbay announced that in January 2025, they received the final major permit required for the development and operation at Copper World. Hudbay also stated that they have commenced the work to support the definitive feasibility and progress the project towards a potential sanction decision in 2026. Copper World is expected to produce 85,000 tonnes of copper per year over an initial 20-year mine life.

Metalla holds a 0.315% NSR royalty on Copper World with the right of first refusal to acquire an additional 0.360% of the NSR royalty.

Akasaba West

On July 30, 2025, Agnico reported record tonnage of ore was processed at the Goldex mill from Akasaba West. The target milling rate of 1,750 tpd was exceeded, averaging 2,864 tpd for the second quarter of 2025.

Metalla holds a 2.0% NSR royalty on Akasaba West subject to a 210 Koz gold exemption and a buyback of 1.0% for $7.0 million.

Big Springs

On July 24, 2025, Capricorn Metals Limited announced the acquisition of Warriedar Resources Limited, the operator of Big Springs and Golden Domes.

Metalla holds a 1.0% NSR royalty on Big Springs and a 2.0% NSR royalty on Golden Domes which is classified as at the exploration stage by Metalla.

Dumont

On June 4, 2025, Mining.com reported that the European Union had selected 13 new strategic raw material projects outside its borders as part of its efforts to secure critical mineral supplies, with the Dumont project among those selected. The 13 projects are expected to mobilize a combined $6.3 billion in capital investments from the European Commission.

Metalla holds a 2.0% NSR royalty on Dumont subject to a buyback of 1.0% for C$1.0 million.

Edwards Mine

On June 24, 2025, Alamos Gold Inc. ("Alamos") reported that regional drilling at the past-producing Edwards Mine intersected high-grade gold mineralization beyond the extent of previous mining, including a highlight intercept of 55.95 g/t gold over 2.12 meters. Edwards is located within seven kilometers of the Magino mill and is one of three targets being evaluated as potential sources of higher-grade mill feed as part of a broader expansion strategy. Alamos plans to complete 10,000 meters of surface drilling in 2025 as part of a regional exploration program at the Island Gold district, focused on following up high-grade mineralization intersected at the Cline-Edwards deposits.

Metalla holds a 1.25% NSR royalty on the Edwards Mine.

MANAGEMENT CHANGE

On July 9, 2025, Metalla appointed Marjorie Winslow as Corporate Secretary. In this role, she will support the Board of Directors and senior management in corporate governance, regulatory compliance, and public company disclosure obligations. Ms. Winslow brings a strong foundation in corporate governance and previously served as the assistant corporate secretary for several TSX and TSX-V listed public companies since 1995, including serving as Metalla's assistant corporate secretary since May 2017. Ms. Winslow replaces Kim Casswell who joined Metalla in 2017 and has decided to pursue other opportunities. We would like to take this opportunity to thank Ms. Casswell for all her efforts during a foundational period for Metalla and wish her luck in her future endeavours.

QUALIFIED PERSON

The technical information contained in this news release has been reviewed and approved by Charles Beaudry, geologist M.Sc., member of the Association of Professional Geoscientists of Ontario and of the Ordre des Géologues du Québec. Mr. Beaudry is a qualified person ("QP") as defined in NI 43-101.

ABOUT METALLA

Metalla is a precious and base metals royalty and streaming company with a focus on gold, silver, and copper royalties and streams. Metalla provides shareholders with leveraged metal exposure through a diversified and growing portfolio of royalties and streams. Our strong foundation of current and future cash-generating asset base, combined with an experienced team gives Metalla a path to become one of the leading gold, silver, and copper companies for the next commodities cycle.

For further information, please visit our website at www.metallaroyalty.com

ON BEHALF OF METALLA ROYALTY & STREAMING LTD.

(signed) "Brett Heath"

CEO

Website: www.metallaroyalty.com

Neither the TSXV nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accept responsibility for the adequacy or accuracy of this release.

Non-IFRS Financial Measures

Metalla has included certain performance measures in this press release that do not have any standardized meaning prescribed by International Financial Reporting Standards ("IFRS") including (a) attributable gold equivalent ounces (GEOs), (b) average cash cost per attributable GEO, (c) average realized price per attributable GEO, (d) operating cash margin per attributable GEO, and (e) Adjusted EBITDA. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors use this information to evaluate the Company's performance and ability to generate cash flow.

(a) Attributable GEOs

Attributable GEOs are a non-IFRS financial measure that is composed of gold ounces attributable to the Company, calculated by taking the revenue earned by the Company in the period from payable gold, silver, copper and other metal ounces attributable to the Company divided by the average London fix price of gold for the relevant period. In prior periods the GEOs included an amount calculated by taking the cash received or accrued by the Company in the period from the derivative royalty asset divided by the average London fix gold price for the relevant period. The Company presents attributable GEOs as it believes that certain investors use this information to evaluate the Company's performance in comparison to other streaming and royalty companies in the precious metals mining industry who present results on a similar basis. The Company's attributable GEOs for the three and six months ended June 30, 2025, were:

| Three months

|

| Six months

|

| ended

|

| ended

| Attributable GEOs during the period from:

| June 30, 2025

|

| June 30, 2025

| Tocantinzinho

| 309

|

| 575

| Wharf

| 279

|

| 405

| Aranzazu

| 175

|

| 339

| La Guitarra

| 30

|

| 59

| La Encantada

| 26

|

| 43

| NLGM

| 21

|

| 47

| Total attributable GEOs

| 840

|

| 1,468

|

(b) Average cash cost per attributable GEO

Average cash cost per attributable GEO is a non-IFRS financial measure that is calculated by dividing the Company's total cash cost of sales, excluding depletion by the number of attributable GEOs. The Company presents average cash cost per attributable GEO as it believes that certain investors use this information to evaluate the Company's performance in comparison to other streaming and royalty companies in the precious metals mining industry who present results on a similar basis. The Company's average cash cost per attributable GEO for the three and six months ended June 30, 2025, was:

| Three months

|

| Six months

|

| ended

|

| ended

|

| June 30, 2025

|

| June 30, 2025

| Cost of sales for NLGM

| $7

|

| $14

| Total cash cost of sales

| 7

|

| 14

| Total attributable GEOs

| 840

|

| 1,468

| Average cash cost per attributable GEO

| $8

|

| $10

|

(c) Average realized price per attributable GEO

Average realized price per attributable GEO is a non-IFRS financial measure that is calculated by dividing the Company's revenue, excluding any revenue earned from fixed royalty payments, by the number of attributable GEOs. The Company presents average realized price per attributable GEO as it believes that certain investors use this information to evaluate the Company's performance in comparison to other streaming and royalty companies in the precious metals mining industry that present results on a similar basis. The Company's average realized price per attributable GEO for three and six months ended June 30, 2025, was:

| Three months

|

| Six months

|

| ended

|

| ended

|

| June 30, 2025

|

| June 30, 2025

| Royalty revenue (excluding fixed royalty payments)

| $2,694

|

| $4,413

| Revenue from NLGM

| 69

|

| 143

| Sales from stream and royalty interests

| 2,763

|

| 4,556

| Total attributable GEOs sold

| 840

|

| 1,468

| Average realized price per attributable GEO

| $3,289

|

| $3,104

|

(d) Operating cash margin per attributable GEO

Operating cash margin per attributable GEO is a non-IFRS financial measure that is calculated by subtracting the average cast cost price per attributable GEO from the average realized price per attributable GEO. The Company presents operating cash margin per attributable GEO as it believes that certain investors use this information to evaluate the Company's performance in comparison to other streaming and royalty companies in the precious metals mining industry that present results on a similar basis.

(e) Adjusted EBITDA

Adjusted EBITDA is a non-IFRS financial measure which excludes from net income taxes, finance costs, depletion, impairment charges, foreign currency gains/losses, share based payments, and non-recurring items. Management uses Adjusted EBITDA to evaluate the Company's operating performance, to plan and forecast its operations, and assess leverage levels and liquidity measures. The Company presents Adjusted EBITDA as it believes that certain investors use this information to evaluate the Company's performance in comparison to other streaming and royalty companies in the precious metals mining industry who present results on a similar basis. However, Adjusted EBITDA does not represent, and should not be considered an alternative to net income (loss) or cash flow provided by operating activities as determined under IFRS. The Company's adjusted EBITDA for the three and six months ended June 30, 2025, was:

| Three months

|

| Six months

|

| ended

|

| ended

|

| June 30, 2025

|

| June 30, 2025

| Net loss

| $(1,603)

|

| $(2,334)

| Adjusted for:

|

|

|

| Interest expense

| 454

|

| 902

| Finance charges

| 81

|

| 161

| Income tax provision

| -

|

| 25

| Loss on extinguishment of convertible loan facility

| 738

|

| 738

| Depletion

| 558

|

| 1,055

| Foreign exchange loss

| 412

|

| 413

| Share-based payments

| 845

|

| 1,391

| Adjusted EBITDA

| $1,485

|

| $2,351

|

(f) Adjusted working capital

Adjusted working capital is a non-IFRS measure calculated by taking the Company's current assets less its current liabilities, excluding any items that are not expected to be settled in cash for the next twelve months. In prior periods the Company presented a working capital adjustment for the convertible loan facility, as the classification of the convertible loan facility as a current liability was driven by changes in classification requirements under IFRS and not because the Company expected that liability to be settled in cash within the next twelve months. With the retirement of the convertible loan facility during the second quarter of 2025, no such adjustment is required. The Company believes that the exclusion, in prior periods, of the convertible loan facility from adjusted working capital gave a more accurate picture of the liquidity of the Company. Adjusted working capital is not a standardized financial measure under IFRS and therefore may not be comparable to similar measures presented by other companies. The Company's adjusted working capital as at June 30, 2025, was:

| As at

|

| June 30, 2025

| Total current assets

| $13,230

| Less:

|

| Total current liabilities

| (3,173)

| Working capital

| 10,057

| Adjusted for:

|

| Convertible loan facility

| -

| Adjusted working capital

| $10,057

|

Refer the Company's MD&A for the three and six months ended June 30, 2025, which is available on SEDAR+ at www.sedarplus.ca, for a numerical reconciliation of the non-IFRS financial measures described above. The presentation of these non-IFRS financial measures is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Other companies may calculate these non-IFRS financial measures differently.

Future-Oriented Financial Information

This news release contains future-oriented financial information and financial outlook information (collectively, "FOFI") about the Company's revenues from royalties, streams, and other projects, which are subject to the same assumptions, risk factors, limitations and qualifications set forth in the paragraphs below. FOFI contained in this news release was made as of the date of this news release and was provided for the purpose of providing further information about Metalla's anticipated future business operations. Metalla disclaims any intention or obligation to update or revise any FOFI contained in this press release, whether as a result of new information, future events or otherwise, unless required pursuant to applicable law. FOFI contained in this news release should not be used for purposes other than for which it is disclosed herein.

Technical and Third-Party Information

Metalla has limited, if any, information on or access to the properties on which Metalla(or any of its subsidiaries) holds a royalty, stream or other interest and has no input into exploration, development or mining plans, decisions or activities on any such properties. Metalla is dependent on (i) the operators of the mines or properties and their QPs to provide technical or other information to Metalla, or (ii) publicly available information to prepare disclosure pertaining to properties and operations on the mines or properties on which Metalla holds a royalty, stream or other interest, and generally has limited or no ability to independently verify such information. Although Metalla does not have any knowledge that such information may not be accurate, there can be no assurance that such third-party information is complete or accurate. Some information publicly reported by operators may relate to a larger property than the area covered by Metalla's royalty, stream or other interests. Metalla's royalty, stream or other interests can cover less than 100% and sometimes only a portion of the publicly reported mineral reserves, resources and production of a property.

Unless otherwise indicated, the technical and scientific disclosure contained or referenced in this press release, ?including any ?references to mineral resources or mineral reserves, was prepared in accordance with Canadian ?NI 43-101?, which differs significantly from the requirements of the U.S. Securities and ?Exchange Commission (the "SEC") ?applicable to U.S. domestic issuers. Accordingly, the scientific and technical ?information contained or referenced in this press ?release may not be comparable to similar information made ?public by U.S. companies subject to the reporting and ?disclosure requirements of the SEC.?

?"Inferred mineral resources" have a great amount of uncertainty as to their existence and great uncertainty as to ?their ?economic and legal feasibility. It cannot be assumed that all or any part of an inferred mineral resource will ?ever be ?upgraded to a higher category. Historical results or feasibility models presented herein are not guarantees ?or expectations of ?future performance.?

Cautionary Note Regarding Forward-Looking Statements

This press release contains "forward-looking information" and "forward-looking statements" (collectively, "forward-looking statements") within the meaning of applicable securities legislation. The forward-looking statements herein are made as of the date of this press release only and the Company does not intend to and does not assume any obligation to update or revise them except as required by applicable law.

All statements included herein that address events or developments that we expect to occur in the ?future ?are ?forward-looking statements. Generally, forward-looking statements can be identified by the use of ?forward-looking terminology such as ??"plans", "expects", "is expected", "budgets", "scheduled", ??"estimates", "forecasts", "predicts", "projects", "intends", "targets", ??"aims", "anticipates" or "believes" or ?variations (including negative variations) of such words and phrases or may be ?identified by statements ?to the effect that certain actions "may", "could", "should", "would", "might" or "will" be taken, ?occur or be ?achieved. Forward-looking statements in this press release include, but are not limited to, statements ?regarding: future events or future performance of Metalla;? the completion of the Company's royalty ?purchase transactions; ?the Company's plans and objectives; ?the Company's future financial and ?operational performance; ? expectations regarding stream and royalty interests owned by the Company; ??the satisfaction of future payment obligations, contractual commitments and contingent commitments by ?Metalla;? management's statements regarding the start and increase of production at properties on which Metalla ?holds royalties and streams, and the timing thereof;? the future availability of funds, including drawdowns pursuant to the RCF; the completion by property owners of announced drilling programs, capital expenditures, and other planned activities in relation to properties on ?which the Company and its subsidiaries hold a royalty or streaming interest and the expected timing thereof; production and life of mine estimates or forecasts at the properties on which the Company and its subsidiaries hold a royalty ?or streaming interest; future disclosure by property owners and the expected timing ?thereof; the completion by property owners of announced capital expenditure programs; the ?expected 2025 gold production guidance at Tocantinzinho and the expected timing thereof; the contributions of Wedge and North Foley to year-end mineral reserve and resources estimates at Wharf; the exploration priorities in the third quarter at Wharf; the expected 2025 production guidance at Wharf; the expected expenditures at Wharf and their purposes; the expected mine life and average annual production at Aranzazu; Sierra Madre's use of proceeds from its private placement to expand the capacity of La Guitarra and conduct a detailed exploration program; Polymetals second pre-payment with its offtake partner; the commencement of concentrate shipments at Endeavor and timing thereof; the expected ores to be processed at Endeavor; the anticipated timing of initial cash flows from Endeavor; the commencement of a new environmental licensing process at Gurupi; the budget allocated to Gurupi; the 2025 planned drilling programs at Gosselin and Côté; the inclusion of the Gosselin deposit into an updated mineral reserve and resource estimate; the completion of an updated technical report for Côté gold mine and the timing thereof; the expected ramp up and expected 2025 production at Côté gold mine; the expected benefits for Castle Mountain's inclusion into the FAST-41 program; the completion of Castle Mountain permitting in December 2026; the completion of the study updates and project optimization for a timely construction decision at Castle Mountain; The expected production based on a 2021 Feasibility Study at Castle Mountain; the advancement of engineering and permitting for the Castle Mountain Phase 2 expansion; the receipt of a notice of intent in connection with the mine permitting ?for Castle Mountain, the ?commencement of the formal permitting review and the anticipated timing thereof; the EIS/EIR stage of formal environmental analysis for Castle Mountain and the timing thereof; the review of the ESIA for Taca Taca by the Secretariat of Mining of Salta Province; First Quantum's wait for a consolidated technical report from provincial authorities for Taca Taca; the completion of an updated NI 43-101 technical report? for Taca Taca; the submission of an application for the RIGI regime for Taca Taca; Highlander's plans to expand the drill program at San Luis; the anticipated completion of the prefeasibility study for the 15-Mile processing hub; the anticipated completion of the joint venture between Hudbay and Mitsubishi; the expected investment and contribution by Mitsubishi into Copper World; the completion of a feasibility study at Copper World by selected companies; the efficient planning and risk mitigation of the project lifecycle at Copper World; the participation of a minority joint venture partner for Copper World in funding the definitive feasibility study, final project design and construction; the completion of a definitive feasibility study for Copper World; the sanctioning of Copper World and the timing thereof;? the expected production of Copper World and anticipated mine life; the mobilization of capital investments from the European Commission into certain strategic projects, including Dumont; the evaluation of Edwards Mine in Alamos' broader expansion strategy; the planned drilling program at Edwards Mine in 2025 and the focus thereof; royalty payments to be paid to Metalla by property owners or operators of mining projects ?pursuant to ?each royalty ?interest; ?the future outlook of Metalla and the mineral reserves and resource ?estimates for the properties with respect to which ?the ?Metalla has or proposes to acquire an interest;? ??future gold, silver and copper prices;? other potential developments relating to, or achievements by, the ?counterparties for the Company's stream and ??royalty agreements, and with respect to the mines and ?other properties in which the Company has, or may ??acquire, a stream or royalty interest;? costs and other ?financial or economic measures;? ?prospective transactions; ?growth and achievements?; financing and ?adequacy of capital; ? future payment of dividends; ?future public and/or private placements of equity, ?debt or hybrids thereof; and ?the Company's ability to fund its current operational requirements and ?capital projects.

Such forward-looking statements reflect management's current beliefs and are based on information ?currently available to ?management. Forward-looking statements are based on forecasts of future results, ?estimates of amounts not yet determinable ?and assumptions that, while believed by management to be ?reasonable, are inherently subject to significant business, ?economic and competitive uncertainties, and ?contingencies. Forward-looking statements are subject to various known and ?unknown risks and ?uncertainties, many of which are beyond the ability of Metalla to control or predict, that may cause ??Metalla's actual results, performance or achievements to be materially different from those expressed or ?implied thereby, and ?are developed based on assumptions about such risks, uncertainties and other ?factors set out herein, including but not ?limited to: risks related to commodity price fluctuations; the ?absence of control over mining operations from which ?Metalla will ?purchase precious metals pursuant to ?gold streams, silver streams and other agreements or from which it will receive royalty ?payments ??pursuant to NSRs, gross overriding royalties, gross ?value royalties and other royalty ?agreements or ?interests and risks related to those mining operations, including risks related to ??international operations, government and ?environmental regulation, delays in mine construction and ??operations, actual results of mining and current exploration ?activities, conclusions of economic ??evaluations and changes in project parameters as plans are refined; risks related to ?exchange rate ??fluctuations; that payments in respect of streams and royalties may be delayed or may never be made;? ??risks ?related to Metalla's reliance on public disclosure and other ?information regarding the mines or ??projects ?underlying its streams ?and royalties;? ?that some royalties or ?streams may be subject to ?confidentiality arrangements that limit or prohibit ?disclosure ?regarding ?those ?royalties and streams;? ??business opportunities that become available to, or are pursued by, Metalla;? that ??Metalla's cash flow is ?dependent on the activities of others;? that Metalla has had negative cash flow from ?operating activities ?in ?the past; ?that some royalty and stream interests are subject to rights of other ?interest-holders;? ?that ?Metalla's royalties and ?streams may have unknown defects;? risks related to ?Metalla's two ?material assets, ?the Côté property and the Taca Taca property;? risks related to general ?business and economic ?conditions;? risks related to global ?financial conditions, risks related to geopolitical events and other uncertainties, such as the conflict in the Middle East and Ukraine;? ?risks ?related to epidemics, ?pandemics or ?other public health crises, including the novel coronavirus global health pandemic, and the spread of other viruses or pathogens, and the ?potential impact thereof on Metalla's ?business, operations and financial ?condition; ??that Metalla is dependent on its key personnel;? risks ?related to Metalla's financial controls;?? dividend ?policy and ?future payment of dividends;? ?competition among mineral royalty companies and other participants in the global mining industry;? that ?project operators may not respect ?contractual obligations;? that Metalla's ?royalties and streams may be ?unenforceable;? risks related to ?potential conflicts of interest of Metalla's directors and officers;? that ?Metalla may ?not be able to obtain adequate ?financing in the future;? ?? risks ?related to Metalla's ?credit facilities and financing agreements;? ?litigation;? ?title, permit or ?license disputes related to ??interests on any of the properties in which Metalla holds, or ?may acquire, a ??royalty, stream or other ?interest;? interpretation by ?government entities of tax laws or the implementation ?of new tax laws;? ?changes in tax laws impacting Metalla;? risks related to ?anti-bribery and anti-corruption ?laws; credit and ?liquidity risk; risks related to Metalla's information systems and cyber ?security;? risks ?posed by activist ?shareholders;? ? that Metalla may suffer reputational damage in the ordinary course of ?business;?? ?risks ?related to acquiring, investing in or developing resource projects;? ? risks applicable to ?owners and ?operators of properties in ?which Metalla holds an interest;? ? exploration, development and ?operating risks;? ??risks related to climate change;? ?environmental risks;? ?that the exploration and ?development activities ?related to mine operations are subject to extensive laws ??and ?regulations;? that the ?operation of a mine or ?project is subject to the receipt and maintenance of permits from ???governmental ?authorities;? ?risks ?associated with the acquisition and maintenance of mining infrastructure;? ?that Metalla's ??success is ?dependent on the efforts of operators' employees;? ?risks related to mineral resource and ?mineral reserve ?estimates;? ?that mining depletion may not be replaced by the discovery of new mineral ?reserves;? that ?operators' mining operations ?are ?subject to risks that may not be able to be insured ?against;? risks ?related to land title;? risks related to international operations;? ?risks related to operating in ?countries with ?developing economies;? ?risks related to the construction, development and ?expansion of ?mines or ?projects;? risks associated with operating in areas that are presently, or were formerly, inhabited ?or used ??by ?indigenous peoples;? that Metalla is required, in certain jurisdictions, to allow individuals from ?that ?jurisdiction to hold ??nominal interests in ?Metalla's subsidiaries in that jurisdiction;? the volatility of the ?stock ?market;? ?that existing securityholders ?may be diluted;? ?risks related to Metalla's public disclosure ??obligations;? ?risks associated with future sales or issuances of debt or ?equity securities; risks associated ??with the RCF;? that there can be no assurance that an active trading ?market for ??Metalla's securities will be sustained;? risks related to the enforcement of civil judgments against Metalla; ???risks ?relating to Metalla potentially being a passive "foreign investment company" within the meaning ?of ??U.S. federal tax ?laws; and the other risks and uncertainties disclosed under the heading "Risk Factors" in ?the Company's most recent Annual ?Information Form and other documents ?filed with or submitted to the Canadian securities ?regulatory authorities on the SEDAR+ website at ? www.sedarplus.ca and the U.S. Securities and Exchange Commission on the ?EDGAR website at ? www.sec.gov. Although we have attempted to identify important factors that could cause actual actions, ??events or results to differ materially from those described in forward-looking statements, there may be ?other factors that cause ?actions, events or results not to be as anticipated, estimated or intended. There ?can be no assurance that forward-looking ?statements will prove to be accurate, as actual results and ?future events could differ materially from those anticipated in such ?statements. Accordingly, readers ?should not place undue reliance on forward-looking statements. We are under no obligation ?to update or ?alter any forward-looking statements except as required under applicable securities laws. For the reasons ?set forth ?above, undue reliance should not be placed on forward-looking statements.

SOURCE Metalla Royalty & Streaming Ltd.

CONTACT INFORMATION: Metalla Royalty & Streaming Ltd.: Brett Heath, CEO, Phone: 604-696-0741, Email: info@metallaroyalty.com; Kristina Pillon, Investor Relations, Phone: 604-908-1695, Email: kristina@metallaroyalty.com CONTACT INFORMATION: Metalla Royalty & Streaming Ltd.: Brett Heath, CEO, Phone: 604-696-0741, Email: info@metallaroyalty.com; Kristina Pillon, Investor Relations, Phone: 604-908-1695, Email: kristina@metallaroyalty.com

|