Why PayPal Stock Deserves a Second Look Before 2025 Ends

Sushree Mohanty - Barchart - 21 minutes ago Columnist

Share

/PayPal%20Holdings%20Inc%20logo%20and%20money-by%20Sergio%20Photone%20via%20Shutterstock.jpg)

PayPal Holdings Inc logo and money-by Sergio Photone via Shutterstock

PayPal Holdings (PYPL) is regaining its stride after a challenging few years of post-pandemic normalization and fierce fintech competition. PayPal reported its third-quarter earnings on Oct. 28. Although PYPL stock is down 16.7% year-to-date, Q3 numbers reveal that PayPal’s transformation is working and could propel the stock to rebound.

As 2026 approaches, PayPal’s balance of profitability, innovation, and long-term growth potential makes the stock worthy of a second look.

www.barchart.comA More Balanced and Profitable Growth EngineUnder the leadership of CEO Alex Chriss, the fintech giant is becoming a stronger, faster-growing, and more profitable company than it was just two years ago. PayPal's comeback is being fueled by a diverse set of business engines, including branded checkout, Venmo, Buy Now, Pay Later (BNPL), and its enterprise payments platform (PSP). www.barchart.comA More Balanced and Profitable Growth EngineUnder the leadership of CEO Alex Chriss, the fintech giant is becoming a stronger, faster-growing, and more profitable company than it was just two years ago. PayPal's comeback is being fueled by a diverse set of business engines, including branded checkout, Venmo, Buy Now, Pay Later (BNPL), and its enterprise payments platform (PSP).

In the third quarter, total payment volume (TPV) increased 8% year-over-year to $458 billion. BNPL also demonstrated ongoing progress with a 20% increase in payment volume, putting PayPal on target to handle almost $40 billion in BNPL TPV by 2025. Pay with Venmo also increased by 40%, setting a record high of $1 billion in TPV in September alone. Adjusted earnings per share (EPS) increased 12% year on year, driven by solid operating leverage.

Venmo is the company's rapidly expanding money transfer platform, which already has roughly 100 million active accounts and has reached a critical inflection point. Venmo's overall payment volume increased by 14% in the third quarter, up from 9% the previous year, marking the fourth consecutive quarter of rapid growth. Venmo is on track to generate $1.7 billion in revenue in 2025, representing a more than 20% year-over-year increase. This performance has made Venmo one of PayPal’s highest-growth segments and a key contributor to the company’s margin expansion.

Management believes that despite its scale, Venmo’s monetization runway remains wide open. The company's "PayPal Everywhere" project, which debuted in the U.S. last year, aims to make PayPal and Venmo the default payment options for all forms of commerce. PayPal intends to be present at every checkout point, whether customers shop online, in a store, or through developing channels like AI-powered agents built by Google, OpenAI, and Perplexity.

What was even more impressive in the quarter was the initiation of PayPal's first dividend, which demonstrated management's confidence in long-term cash production. The company also intends to return 70% to 80% of its free cash flow to shareholders, mostly through share repurchases. Management stressed that the company now has the financial power to both invest in expansion and reward shareholders.

Looking AheadPayPal’s strategic initiatives this year have set the stage for continued growth and expanding margins. The company anticipates a 6% to 7% transaction margin dollar increase in 2025, reversing the negative growth observed two years ago, and at least 15% adjusted EPS growth this year. PSP expansion is also projected to increase PayPal's relevance to major merchants while diversifying its global transaction base. Additionally, Venmo's income is expected to hit $2 billion by 2027.

As Chriss highlighted during the Q3 earnings call, “ We've moved this business from defense to offense, from stabilization to acceleration.” Analysts covering PayPal stock predict earnings to increase by 15% in 2025, followed by another 8.04% in 2026. Currently, PayPal is trading at 13x forward earnings, which is lower than its five-year historical average of 25x.

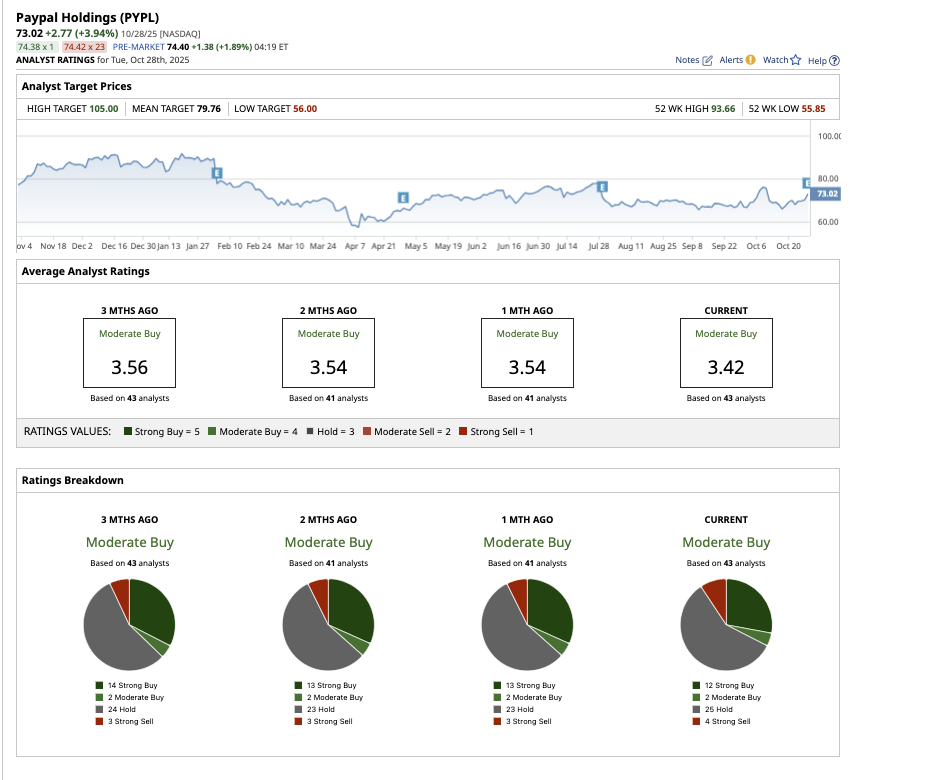

What Is Wall Street Saying About PayPal Stock?Overall, PayPal stock has earned an overall “ Moderate Buy” rating. Of the 43 analysts covering the stock, 12 rate it a “Strong Buy,” two rate it a “Moderate Buy,” 25 rate it a "Hold," and four say it is a “Strong Sell.” The mean target price for the stock is $79.76, which is 12.5% higher than the current levels. The stock's high target price of $105 implies 48.2% potential upside over the next 12 months.

www.barchart.comThe Key TakeawayAfter years of investors’ skepticism, PayPal is making significant progress. With growing TPV, improved transaction margins, expanding Venmo adoption, 12% EPS growth, and robust free cash flow, this may be the moment to look again at PYPL stock. As 2025 comes to a close, PayPal may surprise the market with its next stage of profitable expansion, making it a good growth stock to grab now. www.barchart.comThe Key TakeawayAfter years of investors’ skepticism, PayPal is making significant progress. With growing TPV, improved transaction margins, expanding Venmo adoption, 12% EPS growth, and robust free cash flow, this may be the moment to look again at PYPL stock. As 2025 comes to a close, PayPal may surprise the market with its next stage of profitable expansion, making it a good growth stock to grab now.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here. |