Some prominent investors say danger is lurking in the decades-old method used to build bond portfolios. If they are right, small investors might want to rethink their strategies.

The crux: The traditional method of weighting government bonds by "market capitalization"—the value of a country's bonds in the market—is leading to risky allocations to highly indebted countries, experts say.

Instead, some money managers are switching to other measures, such as gross domestic product, that reflect countries' capacity to pay off their debts.

In March, the managers of Norway's $600 billion sovereign-wealth fund said they would reallocate its government-bond portfolio to reflect the size of countries' GDPs instead of their market caps. That came soon after Citigroup C -2.17%and Research Affiliates launched bond indexes that weight countries by GDP and other measures.

And in May, Fidelity Investments launched a handful of bond funds with benchmarks that track GDP-weighted bond indexes.

"You have a lot fewer defenders of the status quo," says Eric Jacobson, a senior bond-fund analyst at investment-research firm Morningstar.

Since 2009, the earliest data available, GDP-weighted portfolios have outperformed market-cap-weighted bond portfolios by about 1.3 percentage points a year, according to Bank of New York Mellon BK -1.58%. Earlier periods have shown similar performance.

Market capitalization long has been the most-popular way to build indexes. The largest companies, like Apple and Exxon Mobil, XOM +0.21%get the biggest allocation in stock indexes like the Standard & Poor's 500, while small companies either get a tiny allocation or are left out altogether.

The biggest bond indexes, like Barclays BARC.LN -0.15%Global Aggregate Bond or Citigroup World Government Bond, work the same way. The countries with the biggest amount of debt outstanding take up the largest chunks of the index.

But what makes sense with stocks can lead to dangerous outcomes for bonds, say proponents of the new methods.

In effect, market-cap weightings in bond indexes mean that countries with spiraling debt, like those in the euro zone or Japan, take up ever-larger portions of the index and investors' portfolios.

"It doesn't take much to convince a client that the market-cap weighting in bonds doesn't make sense," says David Fisher, head of global product management at Allianz ALV.XE +0.37%unit Pacific Investment Management Co., or Pimco, which in 2009 released its own set of GDP-weighted bond indexes. "It's counterintuitive."

GDP weightings reflect a country's capacity to pay off its debt and ultimately make investors' portfolios less vulnerable to defaults by highly indebted countries, he says.

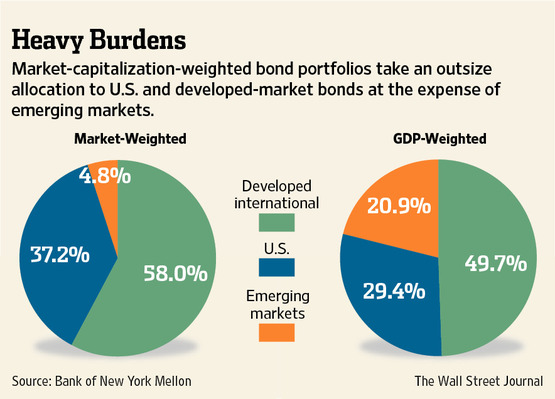

Right now, switching from a market-cap-weighted portfolio to one based on GDP would cut an investor's allocation to Japanese bonds in half, to 11%, and trim the U.S. Treasury allocation to 29% from 37%, according to BNY Mellon.

Emerging-market bonds, which make up only 4.8% of the market-capitalization of bonds world-wide, would make up nearly 21% of a GDP-weighted portfolio. Other developed regions, like Europe, Canada and Australia, fare about the same under either measure, according to BNY Mellon.

Switching to a GDP-weighted bond portfolio does carry risk, says Morningstar's Mr. Jacobson. For one, the higher concentration of emerging-market debt exposes investors to the volatility of countries like South Africa and Brazil, which have suffered serious setbacks even as they have grown.

GDP-weighted portfolios are also still vulnerable to shocks when countries enter debt crises, says Thierry Roncalli, head of research and development at Paris-based Lyxor Asset Management, which manages $97 billion.

Between 2008 and 2011, for example, Greek government bonds were responsible for less than 20% of the price fluctuation of a GDP-weighted European bond portfolio, according to a Lyxor analysis. But by the middle of this year, as the possibility of a Greek default ballooned, bonds from the country caused the vast majority of volatility.

What's more, most bond funds that take a GDP-weighted approach are actively managed, meaning investors have to trust that the manager will perform well on top of the new weighting.

One such fund, the $5.4 billion Pimco Global Advantage Strategy Bond Fund, was launched in 2009 and has had an average annual return of 5.6% in the last three years, 0.13 percentage point above that of the international-bond-fund category, according to Morningstar.

Investors also could build their own GDP-weighted portfolio, says Michael Faloon, chief operating officer at fixed-income specialist Standish Asset Management, a unit of BNY Mellon.

Instead of investing only in an exchange-traded fund that tracks the Barclays U.S. Aggregate Bond Index, such as Vanguard Total Bond Market, BND +0.21%they could keep about 29% in the U.S., 21% in emerging markets and the remainder in international bonds of developed countries. That allocation would roughly mirror countries' GDP breakdown today.

Low-cost options to build the international allocation include the SPDR Barclays Capital International Treasury Bond ETF, BWX +0.16%for example, which invests mostly in bonds in developed markets outside the U.S. and carries an expense ratio of 0.5%.

The Market Vectors Emerging Markets Local Currency Bond ETF EMLC -0.04%invests in emerging-market bonds and has an expense ratio of 0.47%.

Write to Joe Light at joe.light@wsj.com

Is Your Bond Strategy Wrong?

online.wsj.com |