'Babies And Bathwater': Risks Of Passive Investing And ETFs Pile Up--

this was a Seeking al[ha's

Sep. 25, 2017 5:21 PM,,,,,,,,,,, this article was one of the ones on the rhe editors of Seeking alpha highlighted as a seeking alpha as one of the articles they choses to recommend as well

The Heisenberg

Currencies, macro, commodities, geopolitics

I can't understand why proponents of passive investing and/or ETFs steadfastly refuse to acknowledge the inherent risks.

On Monday, Goldman is out with a new note that flags two related issues that stem directly from what one might call "too much passive investing."

Either internalize the dynamic at play here, or don't act surprised when some babies are thrown out with the bathwater.

---------------------------------------------------

I am continually amazed at the demonstrable propensity of ostensibly astute market commentators to imagine that somehow, the epochal shift to low-cost passive investing as facilitated by the rampant proliferation of ETFs somehow doesn't come with consequences.

This is another one of those situations where it isn't entirely clear to me why people steadfastly refuse to acknowledge the downside. In situations where acknowledging the potential drawbacks of this or that phenomenon amounts to a tacit admission that the net effect won't still be positive, it makes some measure of sense to pretend like the drawbacks don't exist. But this isn't one of those situations.

That is, it would be almost impossible to argue that the proliferation of low-cost vehicles - SPDR S&P 500 Trust ETF ( SPY) being the poster child - that allow investors to cheaply express a long-term view on the broad market isn't generally a positive development. It would be equally difficult to argue that the shift to passive isn't likely to be a net win in the long-run. Even if we got a series of meltdowns and malfunctions like those that occurred on the morning of August 24, 2015, it wouldn't change the fact that low-cost, passive investing is the best strategy for most people.

So, you don't need to pretend like there is no downside in order to be a proponent. I will never understand why people insist on ignoring risks when acknowledging those risks doesn't change the general thesis.

There is no question that the shift to passive investing funnels money indiscriminately. That's self-evident. The indiscriminate funneling of money impairs price discovery and leads to the misallocation of capital. Those two considerations are foundational to the broader criticism of passive investing and the rise of ETFs. Recall the following from Howard Marks, quoting Steven Bregman:

As Steven Bregman of Horizon Kinetics puts it, “basket-based mechanistic investing” is blindly moving trillions of dollars. ETFs don’t have fundamental analysts, and because they don’t question valuations, they don’t contribute to price discovery. Not only is the number of active managers’ analysts likely to decline if more money is shifted to passive investing, but people should also wonder about who’s setting the rules that govern passive funds’ portfolio construction.

The knock-on effect of this is obvious. It creates a self-fulfilling prophecy - a perpetual motion machine that serves to levitate a handful of stocks while simultaneously making them appear less volatile than they perhaps should be based on the characteristics of the underlying businesses. Those stocks then become synonymous with momentum and low vol., which embeds them in still more ETFs (factor-based vehicles) and that funnels still more money, and around we go. This is how Arik Ahitov and Dennis Bryan, who run the $789 million FPA Capital Fund, described the situation in a now famous letter penned earlier this year:

The consequence of unrelenting inflows into passive funds is that stocks that are included in a major index receive ongoing support by the indiscriminate purchases made by these funds regardless of a company’s fundamentals. The benefits are amplified for companies that are owned by dozens of ETFs and index funds.

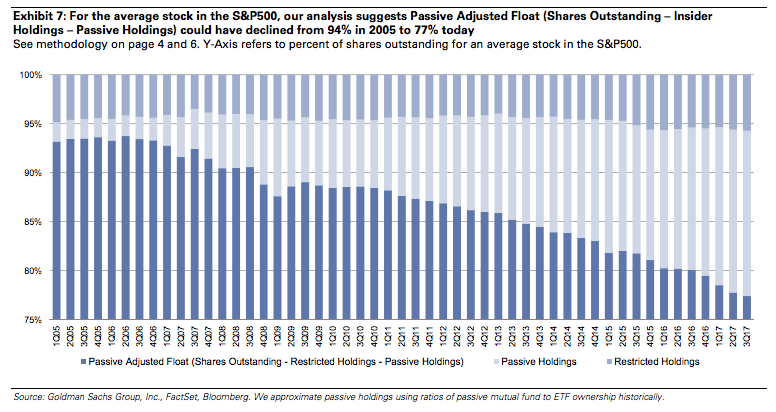

This raises all manner of questions. For one thing, it suggests that the percentage of a stock's float available to active investors who trade or allocate based on fundamentals shrinks. As Goldman writes in a brand new note out Monday, “the share of stock that might trade on fundamental views has dropped to 77% for S&P500 average stock from 95%” in the space of just 10 years. Have a look at this chart:

(Source: Goldman)

Simply put: there goes price discovery.

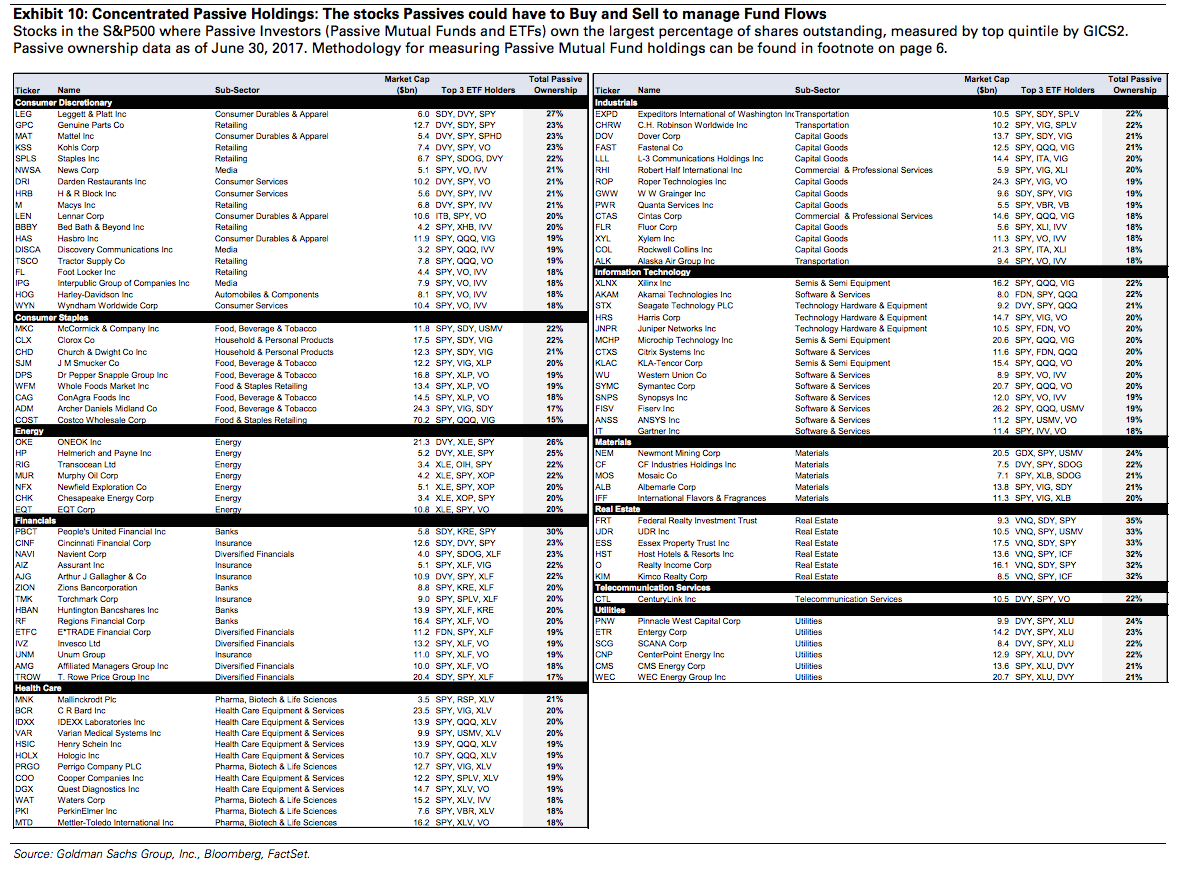

More worrying than that, consider what this means for stocks where passive vehicles control an outsized percentage of the float. Here's Goldman again, from the same note:

We find stocks across all sectors in the S&P500 where Passive ETFs and Mutual Funds have concentrated positions and will likely need to buy if inflows continue or sell if Passive sees outflows.

Because Passive turnover is just 3% a year, current holdings can give us insight into what stocks Passives will need to buy and sell to meet inflows/outflows. We focus on Concentrated Passive Positions for where the impact of a sudden change in flows could be the greatest.

If inflows into passive strategies continue, the impact from Passives having to buy these stocks to deploy capital could be greater. However, if Passive Funds see outflows, the impact from selling concentrated holdings to meet redemptions could be greater.

Do you see what they're driving at? This is creating inefficiencies. It's setting the stage for a scenario in which what gets dumped on a broad-based move lower will be based not necessarily on fundamental concerns, but rather on the extent to which passive strategies have accumulated concentrated positions. Here's the chart that accompanies those excerpts:

(Source: Goldman)

Just to drive the point home: the more concentrated the passive position, the more likely it is that the name could be sold for reasons that have nothing to do with company fundamentals if there is a reversal in fund flows.

That is an exceptionally undesirable situation for anyone who has invested in those names based on an in-depth analysis of the company's prospects (as opposed to owning the shares through a passive vehicle as part of a basket).

Coming full circle, I have a hard time understanding why this is such a contentious topic among those who defend the shift away from active management. On balance, that shift is a positive. But a shift of that magnitude (as Goldman reminds you, "Passives have been net buyers of over $1.7 trillion of US Equities since 2000, while active managers have been net sellers of $1.4 trillion), invariably creates problems and some of those problems are so glaringly obvious that they need to be addressed outside of Street research that most investors will never lay eyes on.

As I wrote earlier today over at Heisenberg Report, you can of course feel free to deride all of this if you so choose, but don’t be surprised if some of your individual stock picks fall more than they should during a broad-based sellofl

seekingalpha.com

JP |