Re <<What Russia's gold maneuver means>>

IWM (I wet myself)

For the read is correct, not only did << Russians just back the ruble to gold? A timeline of how we got here and where we go next >>

But, per Message 33772844 ,

<<BTC <=> fiat <=> physical oil <=> gold>>

If so, Gold and BTC be money-good money, and fiat relegated to promise-of-money.

If doubly so, then we can look to the mother of all deflations of promise-of-money in terms of money-good money.

'THEY' are desperate by the number of anti-gold spins 'they' put out at this juncture

ft.com

Gold fetishism has had its dayMoney isn’t an asset. It’s a privilege

March 3 2022

© AFP via Getty ImagesHarold James is professor of European Studies at Princeton. Brendan Greeley is a PhD student there and a former FT Alphaville writer. Here they look to history to explain Russia’s gold fetishism, and to the nature of money to explain why that fetish will fail to deliver on its promise.

Putin’s war on Ukraine rested on two premises: that a massive show of force would demoralise Kyiv; and that Russia’s $630bn in financial reserves would deter anyone who might question the value of the rouble. But both premises evaporated, because they depended on decisions that were beyond Putin’s control: whether Ukrainians would flee before a column of tanks, and whether the world would continue to grant Russia the privilege of money. Never has money appeared more political.

Like Macbeth, Putin thought that his castle’s strength would laugh a siege to scorn. But money is not like a castle in one important way: it only works when everyone else agrees that you can use it. There was nothing intrinsic about the value of Russia’s reserves, even the $142bn in gold held in Russia itself. They only had value when they were still tied into the global financial system.

Gold has long been fetishised in Russia and elsewhere. But the fetish of gold — Keynes’ “barbarous relic” — is the last gasp of a view that money has an intrinsic value in itself, constituted just by the fact of its existence.

At the end of the 19th century, successive tsarist finance ministers imposed immense hardship on the Russian people to accumulate reserves, eventually taking Russia on to the gold standard. Gold was supposed to lend credibility, and international stature. After 1917, the Bolsheviks called their new currency the chervonets, using the old word for the gold coins that had circulated in Imperial Russia as part of an effort to build linguistic confidence in the new regime. Stalin regarded Russia’s gold as his greatest asset, and one of the principal reasons he refused to take the Soviet Union into IMF membership was that it would have required disclosure of statistical information on Russia’s gold reserves and gold production (then largely achieved by the use of gulag labour).

In the 1990s, Russian nationalists, including many — such as Alexander Dugin — who would exercise an influence on Vladimir Putin, took up the gold theme in a big way. Gold offered a way of resisting the world of the US dollar and international finance; it stood for real value; it carried the historic connotations from the golden religious icons of the Orthodox faith. But if gold cannot be moved in order to be traded, it too is useless. If it is stuck in the vaults of the Bank of Russia, it might as well not exist.

The very names of Ukraine and Russia’s currencies tell another, older history: one not of impregnable strength, but of constant trade. The word for Ukraine’s currency — the hryvnia — is derived from the name of a standardised six-sided ingot of silver. Medieval trade routes moved the ingots from mines in central Europe through the Baltic for wax and furs, then down to the Black Sea for luxuries, and ultimately to what is now China. A rouble, then, was simply a smaller piece of silver along these trade routes. Think of hryvnia and roubles as ingots and shards, inseparable from their role in global trade.

There was nothing mystical about the silver. It was used for decoration, but that doesn’t mean it had what we’d today call an intrinsic value. It was useful because of mining law in Bohemia, because of hundreds of years of informal custom among Baltic traders, because of decisions about money made in Ming China. Silver only had value only because of a series of agreements that moved it from one place to another.

The rouble now, instead of preserving a secure regime, offers a path to opposition. In past conflicts the ability to sell government debt was always regarded as a critical vote of financial confidence, and central banks manipulated interest rates in order to get citizens, whether patriotic or not, to buy national securities. It is clear that Putin has failed that critical vote of confidence. Meanwhile, Ukraine has been able to raise $277mn through a sale of bonds that pay 11 per cent and, more important, are denominated in hryvnia. In the midst of an active, horrific, confusing war, investors are making a political, moral decision with monetary consequences. The greater the international solidarity for Ukraine, the more attractive the bonds will be to investors across the world.

For protesters, it’s dangerous to take to the streets in Russia. The oligarchs don’t even dare voice any open dissent, as the remarkable scene of acquiescence in the Kremlin’s grand Hall of St Catherine demonstrated. But, like the Russians who abandoned the front during the first world war, citizens can still vote with their feet, and move out of the rouble. The lines in Moscow to get dollars — or roubles, before they collapse further — are their own form of protest.

There is now also an intriguing new possibility of how money as a voting mechanism works. Electronic private currencies offer a way of expressing dissent, of rendering a financial vote of confidence. The dramatic surge in the bitcoin price since the imposition of Western financial sanctions — up 15 per cent against the dollar so far this week — is an indication of the movement out of Russian funds and assets, the dramatic flight of capital from a regime that has lost credibility.

People often mistakenly see money as an asset — that’s the old fetishism. But money represents a value, one that needs to be earned. What ultimately makes a currency secure is credibility: the confidence of others. That will depend on whether a government observes laws and conventions. Money isn’t a shared illusion. It is rather a series of agreements and customs among and within countries. Violating some of those agreements can shatter the rest, destroying the privilege of money. A massive violation of norms can produce a massive loss of value. And a fortress of reserves offers no protection.

bloomberg.com

Investors Piling Into Gold ETFs Face a Surprising Tax Bill

Exchange-traded funds backed by physical gold are taxed at a higher rate than stocks of gold mining companies.

Claire Ballentine

23 March 2022, 20:47 GMT+8

Photographer: Lisi Niesner/Bloomberg

Gold exchange-traded funds are one of this year’s hottest investments, with war, inflation and stock-market volatility sending people scrambling for safe havens. But those buying physical gold ETFs may face an unexpected tax burden.

Funds that invest in precious metals like gold and silver are treated like collectibles for U.S. tax purposes, meaning long-term capital gains from those funds will be taxed at a top rate of 28%, compared with a maximum rate of 20% for stocks. This could be costly for investors who decide to cash out after the recent rally in gold prices, which hit a peak of over $2,000 an ounce earlier this month, up more than 20% from a year ago.

Wealth for You

Because you're interested in and

It might come as a surprise for people who recently started making their own trades for the first time, eager to take advantage of rallies in almost every asset class. With apps like Robinhood and Webull, it’s never been easier to start trading. But understanding the tax implications is more difficult, with the reporting for stocks and crypto tokens already creating confusion for some retail investors. Even for those who have spent years buying and selling ETFs, the intricacies of taxes on gold products might be unwelcome news.

Plus, trading apps typically don’t provide a ton of information on the potential tax ramifications of different holdings.

“It’s complicated, and there are lots of nuances to the tax code, so I think a lot of investors — even seasoned investors — aren’t aware of some of the complexities of how investments are taxed,” said Christine Benz, director of personal finance at fund researcher Morningstar.

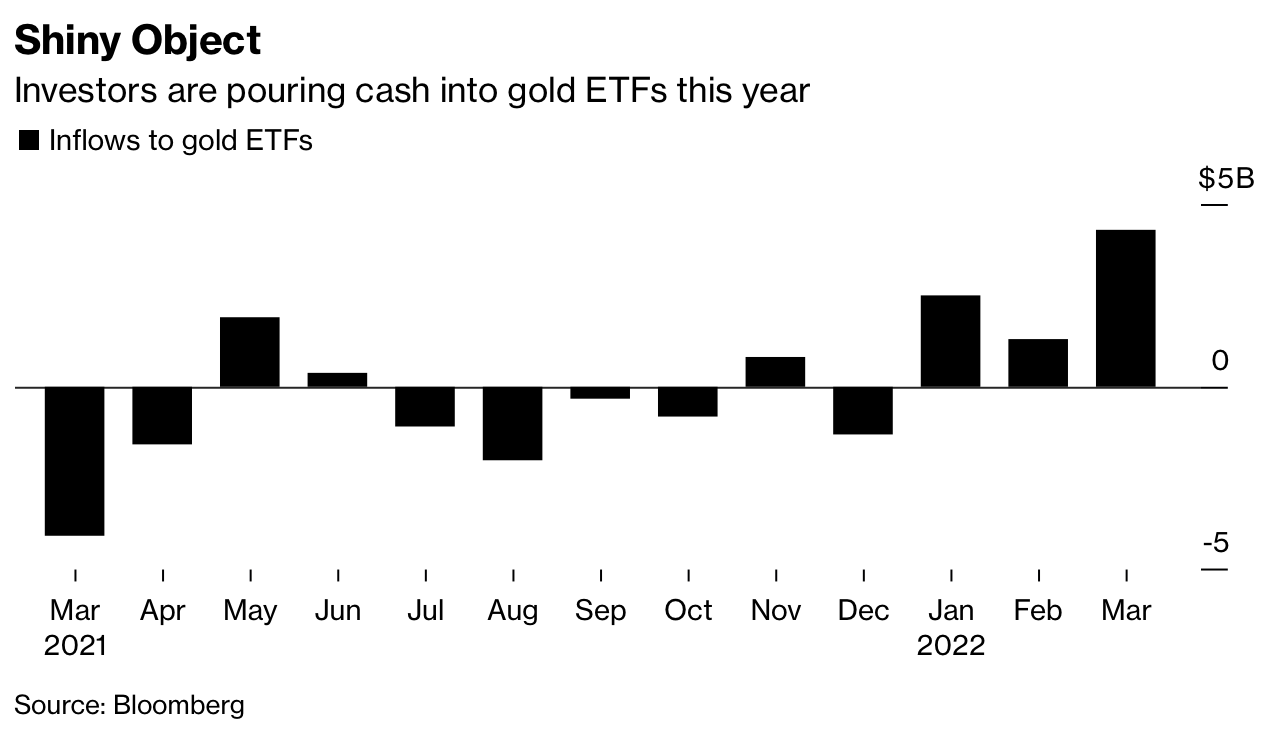

Shiny Object

Investors are pouring cash into gold ETFs this year

Source: Bloomberg

The entire category of gold ETFs has attracted more than $8 billion in new cash this year as investors sought a safe haven for their money amid stock-market volatility, according to data compiled by Bloomberg. That’s a sharp turnaround from 2021, when these funds lost nearly $13 billion as investors sold gold holdings and instead bought riskier assets like cryptocurrencies and meme stocks.

“Gold’s correlation to the stock market tends to turn more and more negative the more significant the risk is, the more significant the pullback is,” said Juan Carlos Artigas, global head of research at the World Gold Council. “The past few weeks have served as an example of this type of behavior,” as stocks fell and gold rallied.

The two largest gold ETFs by far — State Street's Gold Shares ETF (GLD) and the iShares Gold Trust (IAU), with assets under management of nearly $100 billion between them — both invest in physical gold bullion and have attracted the majority of the inflows this year. Even though these funds trade on exchanges like stocks, they’re taxed at the same rate as physical gold coins or bars.

It’s a quirk of U.S. tax policy. When the top capital-gains tax rate was lowered to 20% in the 1990s, collectibles were excluded and left at the old maximum rate of 28%. Because these ETFs are backed by physical metal, their shares are treated the same way as stamps, antiques or gems.

There’s more to consider besides taxes when deciding whether to invest in physical gold or the stocks of gold mining companies, said Nate Geraci, president of the ETF Store, an investment adviser.

“Taxes should never be the tail that wags the dog,” Geraci said. “ETF taxation is something that every investor should be aware of, but I don't believe the higher tax rate for physical gold ETFs should be the sole reason investors look toward gold mining ETFs.”

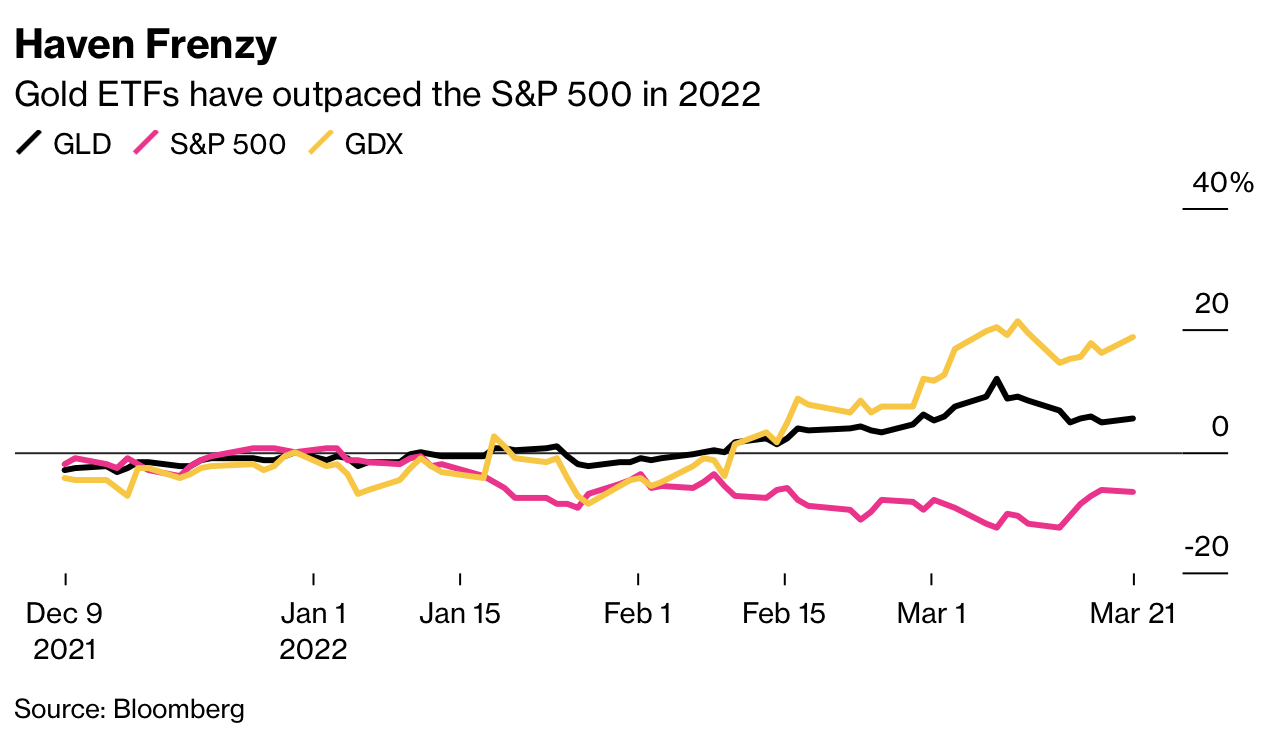

Haven Frenzy

Gold ETFs have outpaced the S&P 500 in 2022

Source: Bloomberg

Gold stocks tend to outperform bullion when gold prices are rising and underperform when prices are falling, said Brandon Rakszawski, vice president of ETF product management at VanEck. That’s because mining costs tend to rise more slowly than prices, allowing miners to boost their profits and potentially pay out more to shareholders via dividends. However, the same is true in reverse: Costs fall more slowly than gold prices in downturns, weighing on profitability.

“Gold stocks are very much tied to gold but come with their own set of risks and considerations, and taxes is just one of those,” Rakszawski said.

VanEck’s own funds illustrate the point: The VanEck Gold Miners ETF (GDX) is up 18% year-to-date, while the bullion-backed VanEck Merk Gold Trust (OUNZ), which is one of a few in the world that allows investors to take delivery of gold bullion in exchange for their shares, has gained 5%. By comparison, the S&P 500 Index is down 5%.

Last year, when the S&P surged 27%, GDX fell 11% and OUNZ lost 4%.

Ultimately, investors should take into account the total cost of owning an ETF, including fees and commissions, when deciding how to invest.

“The lowest-cost physical gold ETF you can find backed by a solid sponsor, that's your best bet if you've been bitten by the gold bug,” said Ben Johnson, director of global ETF research at Morningstar. He also suggests people buy products backed by physical gold through accounts like IRAs, some of which defer taxation until retirement. |