Re <<>> the f*cking f*cks>>

... are f*cking up my day, for am pacing, fretting, and now must get on line to click on green icon before it is too late, and it shall soon (20 min) be lunch hour for the market. I have never understood why the market needs to have lunch.

zerohedge.com

The UBS Precious Metals Team Visited China's Gold Markets: Here Is What They Found

BY TYLER DURDEN

SUNDAY, MAY 19, 2024 - 07:35 PM

In late April, UBS’s precious metals team visited China, which has played a key role in the gold market this year (as discussed extensively here, here, here and elsewhere) – taking in Beijing and Shanghai, easily commutable via a 400 km/hour bullet train in just over four hours. The two centers offered valuable insights into the country’s gold market against a challenging macroeconomic backdrop marked by property devaluations and a weak currency. The team’s visit was a follow-up to a trip taken nine months before.

The report matters because over the last three years, UBS’s footprint has grown considerably into one of the leading suppliers of physical gold to China (it has done this by re-enabling the infrastructure to settle gold via the Shanghai Gold Exchange International ).

China is the largest consuming and producing nation of gold on earth. Of around 3,500 tonnes that is dug out of the ground in primary supply, China consumes around a third of it and produces around 350 tonnes. The balance, 600-700 tonnes, is the universe UBS competes with as an international supplier of gold.

The Shanghai Gold Exchange (SGE) is the main conduit of retail imports where 15 domestic banks have import licenses, and the standard gold bar that is accepted onto the SGE is a kilobar with a fineness of 99.99% gold, about the same size as an iPhone. UBS commissions the top Swiss gold refineries to manufacture such bars which are co-branded with the refinery stamp and the three keys, per the image below:

[url=] [/url] [/url]

There are four domestic subsidiaries of foreign banks with import licenses – where they are obliged to serve the needs of Chinese corporates, and where they see fit can trade the well-trodden SGE/London gold arb. UBS’s business model operates on a wholesale level by utilising its decadeslong relationship with Swiss refineries and unique business model to source material and store it with maximum balance sheet efficiency.

Market activity is governed by seasonality and import quotas – demand typically peaks ahead of the Lunar New Year and then into Golden Week in Q3. Capital controls by the PBoC will lean heavily on the quantum and timing of awarding import quotas to domestic banks. More recently, the authorities have become more selective in awarding approvals in remitting offshore USD payments which has in turn driven more volume through SGEi where gold transactions are settled by the domestic bank in CNY and received by the supplier in CNH.

TINA: There Is No Alternative to Gold

The gold market remained rangebound in 2023, supported by strong official sector demand. PBoC was a well-documented buyer (per IMF central bank gold reserve data). Investor sentiment in western markets has struggled to gather pace with the punitive cost of carry, both as an opportunity cost for potential ETF investors and a funding cost for leveraged participants.

China built up considerable pent-up demand over the last year when the attraction to gold was clear in the form of a store of wealth. And while the authorities all but banned retail imports during much of the year as a capital control measure, there was plenty of activity, however, in supplying commercial banks with LBMA good delivery large bars.

There are two points to make on the flow of large bars into the country – firstly, there are 14 accredited LBMA refineries onshore and the government is keen to promote a made-in-China mantra. Secondly – and more importantly – during periods where import restrictions limited kilobar imports, large bars continued to flow into China, a form of gold that is preferred by the official sector.

China Sentiment – Dip Buying Mentality

UBS’s client base flagged the strength in SGE premium above the London market through the recent surge in gold prices, noting the authorities have a double-edged role in maintaining capital controls via strict gold import quotas and maintaining an orderly domestic market. The SGE premium hovered close to $150 per ounce in late 2023 and remains buoyant, above $30 per ounce.

The Lunar New Year quotas have now been fully utilized, and with gold’s ‘TINA’ status still relevant for small-bar investors, pent-up demand will remain. The authorities will likely take note of the stubbornly weak CNY and expected drag in jewellery demand and most likely tighten the quotas in Q2. As such, the market is likely to be more elastic to price in the near-term with appetite to buy dips towards $2,250 per ounce.

Market views were broadly domestically-driven – that said, clients favored the view that Fed will not cut rates and remain in the higher-for-longer camp, further supporting a dip in the gold price that should be bought into, as the longer-term case of holding it remains valid.

Future trends point towards the SGEi, where UBS is fully operational with a selection of clients. The reluctance by authorities to approve offshore USD remittances will drive further volume down this channel.

The SHFE Fable

The perception in the west lately has been that the Shanghai Futures Exchange (SHFE) gold contract was a key driver of gold’s rally above $2,400 per ounce with commentators including the FT flagging a large spike in volumes and optically large long open interest in the gold contract.

But having polled most clients during the trip, the commentary pointing towards the ‘SHFE effect’ seems purely circumstantial. Onshore banks are prominent market makers on SHFE gold futures – the SGE/SHFE arb akin to the gold EFP traded in western markets is a popular carry trade with bank prop desks and they are in a credible position to comment on this perception.

- SHFE is a speculatively driven gold market, participants rarely stand for delivery, positions are generally rolled or closed cash settled.

- As such, SHFE has minimal impact given the lack of fungibility to the loco London and comex gold futures markets.

- The FT article cited above states that large long open interest positions have built up in recent months amounting to 300 tonnes. What it doesn’t refer to is the net long open interest position which currently amounts to 100 tonnes of gold. Compare to COMEX gold, the most liquid global contract that currently has a net speculative length of 700 tonnes.

- The spike in volumes of this broadly closed futures market was due to two reasons: onshore hedge fund speculation; and rolling of the previously active May contract to the June expiry.

- The true physical driver in China is the SGE; the main contract trades spot for physical delivery and is a true beacon to the international gold price. Retail were banned from trading SGE gold last year.

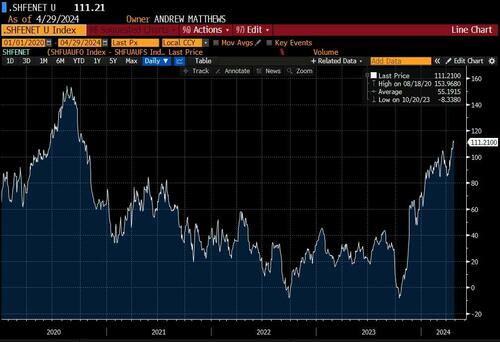

Historical daily net long SHFE open interest, metric tonnes

SHFE post daily gross longs and gross short positions – combining both provides the net position, currently at 111 metric tonnes

[url=] [/url] [/url]

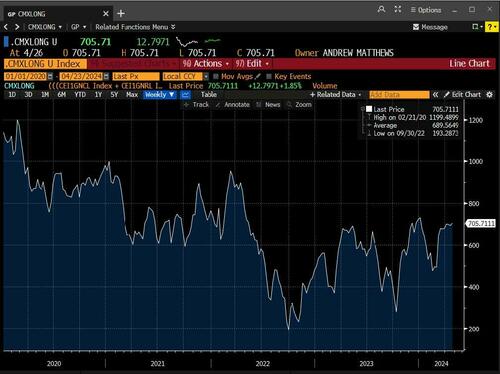

Net non-commercial and non-reportable length of COMEX gold, published weekly. Shown in metric tonnes.

Much larger footprint versus SHFE

[url=] [/url] [/url]

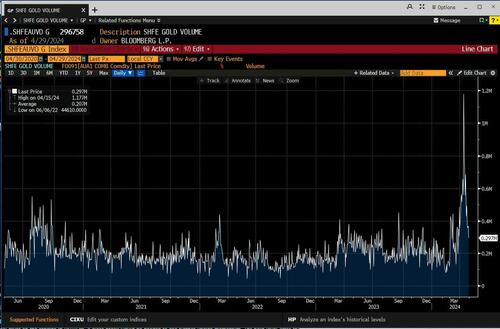

Large spike in volume SHFE gold

Speculative and contract roll driven – little influence on the international gold price

[url=] [/url] [/url]

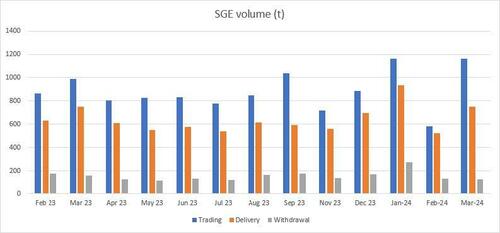

SGE – the true physical market

SGE – monthly physical delivery/withdrawal volumes

[url=] [/url] [/url] |