re <<wow wee>> ... from behind the curtain

Where I’m going with that: the year is not yet 25% complete, and the degree of difficulty is very high, so preservation of capital is as important as anything else right now. zerohedge.com

"Degree Of Difficulty Is Very High" Right Now - Goldman Hedge Fund Honcho Warns 'Preservation Of Capital Is Most Important'

BY TYLER DURDEN

MONDAY, MAR 24, 2025 - 03:45 AM

A lower volume, lower velocity week relative to the fireworks of past month, and US equities scratched out a modest winner.

With a touch of distance from the screens, Goldman Sachs head of hedge fund coverage, Tony Pasquariello, lays out a set of high level observations:

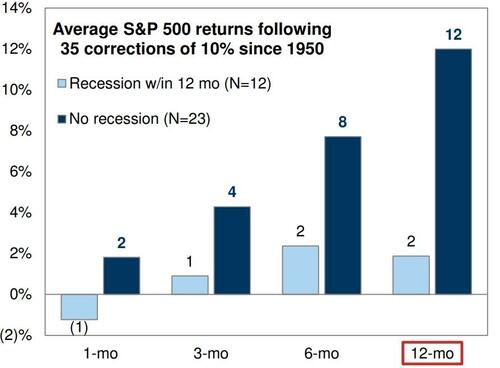

i. a bullish thought: the US economy has clearly slowed, but as this week’s data set demonstrated, growth is not collapsing (as ever, the biggest judgement to make is whether to plan for a recession, or not -- see chart at bottom). in addition, the trading community has already shed a huge amount of length in US equities.

ii. a bearish thought: if the market is going to seriously contemplate recession risk for a while longer, the PE multiple will be under significant pressure (and is far from bottomed out -- witness 14x in late 2018). in addition, it’s not like everyone has culled their overweight in US equities (here I’m referring to structural holders of the asset class, particularly foreigners).

iii. irrespective of market bias, when you take a half step back, it’s stunning how much is going on right now... and, even if implied volatility has settled down, the market continues to metabolize a huge range of significant variables. the result is a trading environment that is profoundly different from the past few years, to say nothing of entire blocks of time (e.g. the secular stagnation era).

iv. what follows from that point: the post-GFC period was dominated by seemingly unbounded Fed policy, extraordinary US fiscal spending and unrivaled US tech preeminence. while I’m still a believer in the structural advantages of the US, that fact set has changed. my point here: the views and biases that one accrued in the past few cycles may not serve them well in the current cycle (again, I have the scars to prove it).

v. in addition, when you step back and monitor the daily flow of market commentary, you realize that a huge part of navigating the current environment comes down to game theory on what is between the ears of just a handful of people.

vi. in the end, whatever your market view, I’d remain very flexible on where this all leads. Here I’ll invoke the wisdom of Jesse Livermore: “when you are doing nothing, those speculators who feel they must trade day in and day out are laying the foundation for your next venture.”

Where I’m going with that: the year is not yet 25% complete, and the degree of difficulty is very high, so preservation of capital is as important as anything else right now.

What follows from here is a set of questions that bounced around my head this week -- with answers provisioned by resident experts.

1. US politics. How significant (and lasting) is the drag on growth from the current abundance of policy uncertainty? will tariffs continue to act as a chokehold on animal spirits? or, are market participants too negative on the agenda -- whereby tariffs will only go so far, tax rates are to be here or lower, and a significant de-regulatory impulse is on the come? enter Alec Phillips:

the market probably has the balance of growth risks right for the near-term. our new survey shows investors expect tariffs and fiscal policy similar to our views: a roughly 9pp overall increase in the effective tariff rate (we expect 10pp), and fiscal policy that leaves the budget deficit broadly unchanged (modest net tax cuts offset by modest spending cuts).

but the sequencing has not been market-friendly, with growth-negative and more uncertain items up front: tariff hikes face few constraints and are clearly negative for growth (we recently downgraded our 2025 growth view on the back of higher tariff assumptions). fiscal policy is a mixed bag, as tax cuts could be growth-positive and follow a predictable process, but DOGE-related cuts have created uncertainty. deregulation would be positive but faces the greatest institutional constraints, making it predictable but slow.

to get to the more positive/predictable parts of the agenda we first have to get through tariffs and the April 2 announcement. President Trump’s approach has been to start big then partly walk back, so the risks on April 2 lean toward a negative surprise. but these tariffs should also represent the upper bound, which is currently unknown, and walking back most of the Canada/Mexico tariffs two days after they took effect suggests market (and public) sentiment is still relevant to this White House, even if the linkage is weaker than 2017-2019. overall, April holds the potential for negative tariff surprises -- even for a market already expecting more tariffs -- but probably also represents peak trade policy uncertainty.

in the couple of weeks that follow the April 2 tariff news, the focus should shift to fiscal front: congressional leaders should finalize targets for the fiscal package, which might net to around $100bn/yr (0.3% of GDP) of additional tax cut and similarly sized but more backloaded spending cuts, meaning only a very modest net fiscal boost. once the House and Senate finalize those targets (likely by mid-April), the ball gets rolling on passing the bill (likely by late July). for now, the growth boost from tax policy looks likely to offset only a fraction of the drag from the tariffs we expect. but if growth looks at risk by the summer, near-term tax cuts might grow a bit.

deregulatory efforts could be positive but will take a while -- it takes more than a year to replace an longstanding regulation with a new one. in the past, we haven’t found much direct linkage between deregulation and hiring or investment, but there was clearly a boost to business sentiment following the election, and some of that seems likely to return tariff uncertainty recedes.

2. US growth. The attendant question: how aggressively can the new administration push tariffs higher -- and spending lower -- before the US economy is at genuine risk of recession. enter Jan Hatzius:

we’ve downgraded our 2025 GDP forecast to a slightly below consensus 1.7% on a Q4/Q4 basis, but have only nudged up our 12-month recession probability from 15% to 20% so far. this is partly because the hard data have shown only limited weakness so far, private-sector fundamentals remain healthy, and we don’t expect a big macro impact from either DOGE job cuts or deportations. but it is also because tariffs are a self-inflicted wound and we would still expect the Trump administration to soften its tariff approach if the economy weakened sharply. we would revise up our recession probability in response to further significant disappointments on that reaction function.

3. The US consumer. n one hand, sentiment surveys look like dirt, and pressures on the low end consumer are accumulating. on the other hand, the hard data looks solid (witness retail sales), and the high end consumer seems stable. where does this all net out? enter Joseph Briggs:

as noted in our March consumer dashboard and highlighted by the stronger retail sales report this week, concerns around the consumer earlier this year were mostly overblown. any softness in hard spending data seen so far appears to have been driven by choppy seasonals and colder weather, which is not too surprising given that consumer fundamentals remain solid (even after accounting for the recent pullback in equity prices). that said, I’m moderately concerned about the consumer outlook. if Trump cumulatively raises the effective tariff rate by 10pp on April 2 (in line with our forecast), job growth should slow and higher inflation will erode consumer income and spending power. as a result, we now forecast only 2.0% real income growth in 2025 on a Q4/Q4 basis (vs. 2.5% previously). this hit to real spending power, combined with increasing evidence that uncertainty is taking a toll on consumer sentiment, sets the stage for a more challenging consumer outlook (if Trump indeed delivers large tariff increases). we therefore forecast real consumer spending growth slows to 1.9% in 2025 on a Q4/Q4 basis (vs. 3.1% in 2024).

4. The Fed. relative to all of the recent fireworks in the foreground, the Fed has occupied a less consequential spot in the background. going into the FOMC meeting, I had two basic questions: (1) would Powell [or the SEP] give a clear sense for where the Fed put is struck; (2) what is the glidepath for QT? enter David Mericle:

I thought Powell was a bit dovish, quite comfortable with the two-cut baseline and unconcerned about the rise in Michigan inflation expectations. I still think that high inflation and inflation expectations mean the bar for cuts will be higher than it was in 2019, but the risks are much larger too, and if the economic data weaken enough for the FOMC to worry the unemployment rate might start trending higher, I think they would cut. on QT, we expect it to continue through Q3, though I don’t think it matters at a macroeconomic level.

5. Is the 2018 analog the right one? I’m dropping this specific comparison in because it’s the one that keeps coming up in client dialogue. enter Dominic Wilson:

what’s interesting about that episode relative to this one -- for all the obvious differences -- is the origin of the problem: the market came to believe that the Fed policy put was struck much further out than they thought it should be (particularly after the “far from neutral” remarks from Powell). then, when growth fears surfaced in late 2018 (even though they proved mostly overdone), the market unwound sharply. the process didn’t really stop until Powell pivoted in early January and market views of the policy stance shifted.

it’s the Administration more than the Fed that’s creating the parallel now, but we are seeing what happens when policymakers signal that the put is far away and that they aren’t willing to support growth at a moment when the market is worrying that they should. as long as the market believes that’s an error, then the market is going to stay very sensitive to any sign of growth weakness, until there’s some sign that the policy stance is shifting. you could get lucky if the growth data holds up better than expected. but this set-up means we’re likely to stay very vulnerable to anything growth-negative from the data or fresh policy. and if it’s the Fed that flinches -- as they did in 2018 -- not the Administration, that’s more likely to be going to be at lower prices or with clearer signs of economic damage, though this week's FOMC provided some reassurance that the Fed does not feel overly constrained in responding if the economy stumbles.

6. The US credit market. Should one be concerned about the recent creak wider in spreads? what’s the fundamental view on where we’re headed? enter Lotfi Karoui:

since the first tariff headlines broke in early February, our message has been simple: add hedges and brace for some rebuild in premia, given an unexpectedly thicker left tail of the risk distribution. despite the spread widening of the last few weeks, current spread levels are still too tight, in our view. we expect more widening towards historical medians, akin to a realignment to higher macro volatility. that said, we do not envision spreads overshooting to recession levels, nor do we expect defaults and rating downgrades to pick up materially from here. this is essentially a repricing of risk premia, at least for now.

7. Europe. Are we so sure that newfound fiscal enthusiasm can absolve Europe of its growth challenges? who has space to fiscally expand beyond Germany? if the Trump administration really ups the ante on tariffs, how big a headwind is that? enter Jari Stehn:

Germany's fiscal package implies a material shift in policy and we notably raised our German GDP forecast, with a cumulative upgrade of 1.5% over the next 3 years. fiscal space in the rest of Europe, however, is more limited and we upgraded our forecast for the Euro area by half as much, up a cumulative 3/4% through 2027. despite this material improvement in the growth outlook, the near-term risks to growth remain to the downside given rising trade tensions with the US. in particular, we estimate that an across-the-board tariffs on the EU would lower Euro area GDP by around 1% this year (only half of which is included in our baseline forecast). as a result, we look for two more ECB cuts to 2% in June.

8. China. After something of a tease last fall, has the long-awaited fiscal support for consumption finally arrived? enter Hui Shan:

the “special action plan” for boosting consumption says all the right things: raise employment and income, stabilize stock and house prices, strengthen social safety net, and even encouraging workers to take vacations. but there aren’t many details or much funding behind the high-level guidelines in the announcement. besides the RMB 300bn for the consumer goods trade-in program (i.e., China’s cash-for-clunkers) this year, not much has been offered so far. my take is that the government understands that consumption is weak and they need to boost consumption, but they either do not know how to sustainably increase consumption or are unwilling to allocate significant amounts of fiscal spending to boost consumption. bottom line: we do think fiscal support for consumption is the direction of travel, but we do not expect the pace will be rapid.

9. Japan. This market has suffered from a loss of momentum -- and thus popularity -- in 2025. with that said, TPX never really broke its trading range, and that specific index has quietly been trading better of late (up seven straight days). enter Dani Wojdyla:

Japan has fallen out of the spotlight. foreign positioning is at the lows yet the fundamental backdrop remains intact (earnings revisions are among the highest across DMs; TPX is trading on ~13x forward PE despite double digit forecasted EPS growth). the lack of interest can be chalked up to a combination of a variety of factors -- cyclical market coupled with forex instability, lack of catalysts, tariff risk, political uncertainty, policy rates still normalizing, et al -- and think the Aug 5th sell off did material damage that has set the bar even higher to re-engage. China was also the unexpected wildcard this year: many investors in the region were not positioned for HSI to outperform NKY by 19%+ YTD.

looking forward, we are entering a seasonally strong time of year. Bruce Kirk in GIR notes that TPX has produced a mean Mar-Jun cumulative return of +5.3% since 2020, providing some additional seasonal support for our current constructive view. there will also be sizeable inflows into TPX with the upcoming Mar '25 dividend reinvestment - our trading desk assumes some of the positioning will start this week. after div reinvestment, another catalyst is Q4 earnings starting end-Apr and reloading of positions from domestic community in the new fiscal year from Apr 1st. themes that are working are not new but still see room to run (banks, defense), and expect more focus on corporate reform going into the June AGM season.

10. Gold. The yellow metal has been as good an asset as any on the board . why? lower real rates -- check. weaker dollar -- check. hedge against disorderly outcomes -- check. ongoing destination for central bank reserves -- check. enter Tony Kim (who was more sober than I expected):

the pace of the rally YTD has certainly given us pause. investors are worried of a flush on a Ukraine/Russia peace headline, but most agree they’d want to buy that dip. recent client roadshows in both Asia and the US indicate that participation is close to the lows of the last 12 months, which is incongruent to the universally bullish view on the structural thesis of de-dollarization. there is scope for the rally to continue -- buy dips and deploy options for upside expressions as implied vol and call skew are still reasonably priced (binaries, call spreads and light exotics look interesting).

11. flow-of-funds / positioning. I’m going to break this into the six most important parts:

i. what is the positioning of the systematic trading community in US equity index futures? Paul Leyzerovich:

currently the community -- CTA trend followers + risk parity style + VA vol control -- is long $123bn, down from a YTD high of $217bn in February. the historical max for reference is $265bn, and historical low is $18bn, so this current $123bn is near a 1-yr low and a 43% rank on that historical min-max scale. it’s a combination of CTA being net short after the signals turned negative in February, and RP + VA VC -- led by the latter -- cutting some size as vols rose. CTA are much closer to their historic lows than the vol-based investors. from here, the baseline selling has rounded out and completed and the forward is pretty neutral, i.e. the industry has rebalanced into its new target weights for the time being.

ii. how are discretionary hedge funds positioned -- net exposure is very contained, yet gross exposure remains elevated? Vincent Lin:

six straight weeks of net selling of US equities. our view is that this has been much more of a “net down” than “gross down” episode: (1) while HFs aggressively unwound risk on Mar 7 & Mar 10, managers added back risk when performance started to stabilize, as gross trading flow increased in each of the 6 subsequent sessions, led by short sales; (2) overall gross market value (numerator of the gross leverage equation) fell to the level seen just before last year’s US elections, driven mainly by price declines (mark-to-market), while net market value is at the lowest level since Sep ’24; (3) global fundamental long/short gross leverage is still high in the 83rd percentile vs the past year, while net leverage is at one-year lows (vs 100th percentile a month ago).

iii. what are active long only funds up to? Arianna Contessa:

LOs sold $4bn on the week and $22bn over the past month, which is the most supply we’ve seen in the past three years.

iv. what are US retail traders up to? Ryan Sharkey:

retail engagement in the market has been consistent to start the year, albeit at different paces (large buying in January and only 7 net selling sessions YTD). over the last week, we are seeing green shoots of an enhanced buy footprint. however, with tax season approaching, April tends to be the second worst month of the year for the retail darlings (GSXURFAV).

v. with the Q1 reporting period around the corner, what is the glidepath for stock buybacks? Vani Ranganath:

the beginning of this week was still active, but we are seeing a slight decrease in activity. with the blackout underway, we’re expecting our flows to decrease ~30% over the period. we expect this blackout to end around April 25th.

vi. what is the expectation for quarter end asset rebalancing? Braden Burke:

US Pensions are modeled to BUY $30bn of US equities for quarter-end. $30bn to buy ranks in the 92nd percentile amongst all buy and sell estimates in absolute dollar value over the past three years and in the 92nd percentile going back to Jan 2000.

TP conclusion: again, the fiercest risk transfer from the levered community is behind us.

As we emerge from quarterly expiry -- which should always be watched for its mysterious ways -- we’ll lose a tailwind in stock buybacks, yet pick up a tailwind from pensions (and, perhaps, the CTA community).

That all nets out to something of a draw.

Therefore, the spotlight remains on the structural holders of US equities (both households and institutions). .

Finally, one chart for the road...[url=] [/url] [/url]

To say it again, the big judgement that stock operators need to make is whether you think a recession is coming or not. |