Viva Gold Announces PEA Study Results for its Tonopah Gold Project, Nevada

thenewswire.com

VANCOUVER, BC – TheNewswire – July 7, 2025 – Viva Gold Corp (TSXV: VAU; OTCQB: VAUCF) (the “Company” or “Viva”) is pleased to announce the results of its updated Mineral Resource Estimate (“MRE”) and Preliminary Economic Assessment (“PEA”) for its 100%-owned Tonopah Gold Project (“Tonopah or Project”). Tonopah is located about 20 minutes’ drive from the town of Tonopah, Nevada. The study was prepared by WSP Canada Inc. (“WSP”) of Calgary, Alberta and Kappes, Cassiday Associates (“KCA”) of Reno, Nevada. All amounts shown in this news release are in United States Dollars and metric units of measurement unless otherwise stated.

Tonopah Project PEA & MRE Highlights

- The updated MRE reports measured and indicated (“M”) Mineral Resource containing 504,000 ounces gold (“Au”) at 0.59 grams per tonne (“g/t” Au, 1.8 million ounces silver (“Ag”) 2.05 g/t Ag, and an inferred Mineral Resource of 83,000 ounces Au at 0.37 g/t Au, 402,000 ounces Ag, at 1.81 g/t Ag, all constrained within a pit shell above a 0.15 g/t Au cut-off (see Table 1).

- Life of mine “LOM”) PEA production of 23.5 million tonnes of Mineral Resource; consisting of 4.5 million tonnes at an average grade of 1.75 g/t Au and 3.35 g/t Ag as mill circuit feed; and 19.0 million tonnes at 0.37 g/t Au and 1.69 g/t Ag to the heap leach; at a strip ratio of 3.9 tonnes of waste per tonne of mineralized material.

- Average mill circuit gold recoveries of 93% Au, 37% Ag, and heap leach Au recoveries of 75% Au, 14% Ag, to produce a total of 404,000 ounces of payable Au and 354,000 ounces of Ag over a seven-year mine life with an additional year of residual Au/Ag recovery from the heap leach.

- After-tax net present value (“NPV”) at a 5% discount rate (“NPV5%”) of $111.6 million at a gold price of USD$2,400 per ounce($27.70 Ag increasing to $363.6 million at a gold price of $3,200 per ounce ($36.93 Ag).

- After-tax Internal rate of return (“IRR”) of 17.6% at a gold price of $2,400 per ounce increasing to an IRR of 43.4% at a gold price of $3,200.

- After-tax payback period of 3.6 years from commencement of production at $2,400 per ounce Au, decreasing to 1.8 years at an Au price of $3,200 ($36.93 Ag).

- Average production cash costs of $1,164 per ounce of Au and All-In Sustaining Cost (“AISC”) of $1,269 per ounce Au.

- Pre-production capital expenditure of $219.9 million, $22.2 million in working capital, and additional LOM sustaining capital of $70.4 million including purchase of mine fleet under capitalized lease/purchase terms. New equipment pricing is assumed at this phase of work.

“This detailed PEA of the Tonopah Gold Project demonstrates significant leverage to the price of gold and displays accretive potential value when compared to Viva’s current market capitalization”, states James Hesketh, President & CEO. “The Tonopah gold project represents a unique opportunity to develop a gold project in one of the best mining jurisdictions in the world with excellent existing infrastructure and proximity to surrounding producers and metallurgical facilities. This location reduces infrastructure capital and can help to accelerate the permitting process. Opportunity may exist to defer or reduce initial capital expense through toll processing/milling, purchased of used equipment, or through contract mining with competitive bidding versus owner mining operations. We also believe that a unique permitting environment exists in the US and Nevada and Viva intends to accelerate feasibility study on Tonopah which will allow Viva to initiate the permitting process to take advantage of that window. In addition, while Viva’s focus is on advancing its core gold resource through feasibility and permitting, we remain convinced that substantial exploration potential remains in and around our project area, which we can demonstrate from existing drill results”.

Project Description

Viva’s 100% owned Tonopah gold project sits in the middle of gold mining country about a half hour drive south of the Round Mountain mine owned by Kinross Gold and controls a major land position on the prolific Walker Lane Trend in Western Nevada. Viva has developed a high confidence level gold Mineral Resource and can demonstrate the potential for an economically viable open pit, heap leach/mill gold project through rigorous PEA study. The Project enjoys paved highway access, and proximity to Nevada grid power, commercial water supply, and a vast local vendor network for sourcing required mining project consumables and equipment.

Tonopah is a near surface, well oxidized, epithermal gold/silver deposit with gold mineralization occurring in higher-grade veins and brecchias, all within a blanket of low-grade disseminated gold mineralization. Drill results demonstrate the potential for additional exploration potential, while the core Mineral Resource has been drilled to a high confidence level with approximately 87% of total contained gold ounces in the M&I resource category. The Project is located on 508 unpatented federal lode claims.

The PEA study was developed using conventional open pit hard rock mining methods at a nominal rate of approximately 45,000 tonnes per day (“TPD”) of material mined over a seven-year period. Pit slope angles are based on geotechnical study completed for Viva in 2020. Mined gold mineralization is transported by truck to either a high-grade (> 1.0 g/t) or low-grade stockpile. Barren waste rock would go to a waste rock storage facility.

Process design was developed based on preliminary indicative metallurgical testwork. The process considers crushing 10,000 TPD of mineralized run-of-mine material including 8,000 TPD of low-grade and 2,000 TPD of high-grade material. Mineralized material will be crushed to 100% passing 12.5 mm using a three-stage closed crushing circuit. High-grade and low-grade material will be campaigned through the crushing circuit and stockpiled separately using a radial stacking conveyor. Low-grade material will be agglomerated with cement, before being conveyor-stacked in 10m lifts onto a permanent geomembrane-lined heap leach pad and leached with a dilute cyanide solution. Pregnant leach solutions will be pumped to a carbon adsorption circuit. Gold will be collected onto activated carbon and then periodically transported off-site to be toll-processed where the loaded carbon will be stripped and regenerated before being returned to the Project for re-use.

High-grade mill feed ground to 80% passing 150 Mesh (106 micron) in a single stage ball mill circuit. Ball mill discharge will be diverted to a Carbon-in-Leach (“CIL”) circuit where the thickened slurry will be mixed with activated carbon with a portion of the flow being diverted to a gravity concentrator for the recovery of coarse metal. Loaded carbon from the CIL will be toll-processed along with carbon from the heap leach circuit. Leached slurry will be discharged and filtered using a filter press, and dry-stacked using trucks onto a dedicated portion of the heap leach pad.

The Tonopah open pit will extend below the existing water table. As a result, a pit de-watering system is required to de-water ahead of mining advance. A conceptual dewatering system design for the Project was developed by Piteau Associates of Reno, Nevada, Viva’s long term hydrologic consultant, dated June 20, 2025.

Existing project infrastructure includes paved State highway access, nearby 15 KV grid powerline upgradable to 25 KV, newly constructed cell and data communications tower, and nearby public utility water supply. The project has a total of 26 existing groundwater monitoring wells. Additional infrastructure will include fencing and gates, weigh scale, office buildings, repair shops, assay laboratory, fencing and gates, water supply system, power substation and overhead distribution lines.

Mineral Resource

The 2025 MRE incorporates data from 59 new drill holes completed since 2022, as well as a new structural model based on drilling and Controlled Source Audio-frequency Magnetotellurics (CSAMT) data. The updated resource model has resulted in an increase in the indicated resource, demonstrating enhanced confidence in the geologic interpretation.

Table 1: Summary of Estimated Mineral Resources – Effective Date: June 13, 2025

Classification

| Au (g/t)

| Ag (g/t)

| Tonnes (Kt)

| Contained Gold (oz/t)

| Contained Silver (oz/t)

| Measured

| 1.41

| 3.11

| 1,690

| 77,000

| 169,000

| Indicated

| 0.53

| 1.98

| 25,000

| 427,000

| 1,593,000

| Measured + Indicated

| 0.59

| 2.05

| 26,690

| 504,000

| 1,762,000

| Inferred

| 0.37

| 1.81

| 6,905

| 83,000

| 402,000

| Total

| 0.54

| 2.00

| 33,560

| 587,000

| 2,164,000

|

Notes:

- The MRE for the potentially surface mineable resource were constrained by conceptual pit shells for the purpose of establishing reasonable prospects of eventual economic extraction based on potential mining, metallurgical and processing grade parameters identified by studies performed to date on the Project.

- Key constraint inputs included reasonable assumptions for operating costs, geotechnical slope parameters, forecast Au prices, and a minimum Cut-off Grade of 0.15 g/t Au.

- The Cut-off Grade assumes a gold price of US$2,200 and a revenue factor of 1.2 (equivalent to US$2,640 gold price), and includes all material that can be economically processed

- Heap leach recovery of 75% was assumed.

- Tonnage and contained metal estimates are rounded to the nearest 1,000.

- kt = kilotonnes; g/t = grams per tonne; oz/t = troy ounces per tonne.

- Mineral Resource categorization of Measured, Indicated and Inferred Mineral Resources presented in the summary table is in accordance with the CIM definition standards (CIMDS, 2014).

- No mining recovery, dilution or other similar mining parameters have been applied.

- Although the Mineral Resources presented in this press release are believed to have a reasonable expectation of being extracted economically, they are not Mineral Reserves. Estimation of Mineral Reserves requires the application of modifying factors and a minimum of a PFS.

- The reported Inferred Mineral Resources are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as Mineral Reserves.

- There is no certainty that all or any part of this Mineral Resource will be converted into Mineral Reserve.

- Mineral Resource estimates are not precise calculations, being dependent on the interpretation of limited information on the location, shape and continuity of the occurrence and on the available sampling results. All figures are rounded to reflect the relative accuracy of the estimates.

The Mineral Resource categorization applied by the Qualified Person (“QP”) has included the consideration of data reliability, spatial distribution and abundance of data and continuity of geology and grade parameters. The QP performed a statistical and geostatistical analysis for evaluating the confidence of continuity of the geological units and grade parameters. The results of this analysis were applied to developing the Mineral Resource categorization criteria.

The updated MRE reports 504,000 ounces of measured and indicated gold resources at 0.59 g/t Au, constrained within a pit shell above a 0.15 g/t Au cut-off (see Table 1). Compared to the 2022 PEA, this is an increase of 109,000 ounces of measured and indicated Mineral Resources, and a reduction of 123,000 ounces of inferred Mineral Resources. Additional drilling reduced drill hole spacing and revealed new high-grade zones as well as non-mineralized areas. The introduction of a structural interpretation served to constrain the estimate to additional hard-boundary domains. For the first time, 2,164,000 ounces of silver at 2.0 g/t are reported.

Au and Ag were estimated into a 3D block model using ordinary kriging interpolation. The block size in the area of the reported resources is 6 m x 6 m x 6 m. Estimation was constrained by hard boundary domains based on rock type and fault boundaries.

Primary differences between the 2022 resource block model and the 2025 resource block model include a reduction in block size from 20 m to 6 m, a change in the Au top-cut grade parameters (increased from 10 g/t to 100 g/t and using a high-grade search restriction), and a change to the resource classification methodology.

At present, only Mineral Resources have been estimated and there are no Mineral Reserves for the Project.

The Mineral Resource estimates for the potentially surface mineable resources at Tonopah were constrained by conceptual resource pit shells for the purpose of establishing reasonable prospects of eventual economic extraction based on potential mining, metallurgical recovery and processing parameters identified by mining, metallurgical, and processing studies performed to date on the Project.

Key constraint inputs included reasonable assumptions for operating costs, geotechnical slope parameters, Au forecast prices, as summarized in Table 2, resulting in a minimum Cut-off Grade (“COG”) of 0.15 g/t Au. The COG assumes a gold price of US$2,200 and a revenue factor (“RF”) of 1.2 (equivalent to US$2,640 gold price) and includes all material that can be economically processed.

Table 2: Break-Even Cut-off Grade for Mineral Resources

Parameter

| Unit

| Value

| Processing Costs (incl. Sustaining Capex) + G&A

| $/t

| 7.12

| Processing Recovery

| %

| 75.0%

| Refining Recovery/Payable

| %

| 99.9%

| Royalty

| % NSR

| 1.0%

| Refining Cost/Selling Cost

| $/oz Au

| 2

| Resource Gold Price at RF

| $/oz Au

| 2,640

| Cut-off grade

| g/t Au

| 0.15

|

GEOVIA Whittle™ (“Whittle”) Pit Optimizer software was used to develop the resource pit shell. Whittle was used with the input parameters presented in Table 3 to provide guidance for establishing reasonable prospects of eventual economic extraction.

Table 3: Resource Pit Shell Input Parameters

Mining Parameter

| Unit

| Value

| Waste Mining Cost1

| $/t

| 1.90

| Mineral Mining Cost1

| $/t

| 1.90

| Overburden Mining Cost1

| $/t

| 1.60

| Mining Sustaining Capital Cost2

| $/t

| 0.24

| Mining Recovery3

| %

| 100

| Mining Dilution3

| %

| 0 | Processing Parameter

| Unit

| Value

| Mill Recovery

| %

| 92.5

| Heap Leach Recovery

| %

| 75

| Mill COG

| g/t

| 1.0

| Heap Leach COG

| -

| breakeven

| Mill Processing Cost + G&A

| $/t

| 17.50

| Mill Processing Sustaining Capital Cost4

| $/t

| 0.11

| Heap Leach Processing Cost + G&A

| $/t

| 8.70

| Heap Leach Processing Sustaining Capital Cost5

| $/t

| 0.62

| Selling Parameter

| Unit

| Value

| Gold Price

| $/oz

| 2,640

| Gold Royalty

| %

| 1.0

| Selling Cost

| $/oz

| 2.00

| Gold Payable

| %

| 99.9

|

Notes:

- The mineral and waste mining cost were based on escalated mining cost from similar projects in Nevada and nearby states escalated to Q2 2025 US$ value. The overburden mining cost is the cost of free digging the overburden, without drilling and blasting.

- Mining sustaining capital cost of 0.24 $/t was calculated based on the escalated April 2020 PEA cost estimate to Q2 2025 US$ value and was included in the pit optimization to the mining cost.

- The block model described included dilution or mining recovery. Viva recommended to use 100% mining recovery and 0% dilution, and it is the QP’s opinion that this logic is reasonable for a PEA-level study.

- Mill processing sustaining capital cost of 0.11 $/t was obtained from the April 2020 PEA cost estimate and escalated to Q2 2025 US$ value.

- Heap leach processing sustaining capital cost of 0.62 $/t was obtained from industry benchmarking, and both were included in the pit optimization to the processing cost for all scenarios.

PEA Mine Plan and Production Details

Tonopah will have a seven-year mine life with eight years of gold recovery. Closure and reclamation activities are expected to commence at the cessation of mining and last for a period of three years utilizing exiting mine equipment and personnel. Please note that a Preliminary Economic Assessment is preliminary in nature and includes inferred mineral resources that are considered too speculative geologically to have the economic consideration applied to them that would enable them to be categorized as mineral reserves, and that there is no certainty that the preliminary economic assessment will be realized.

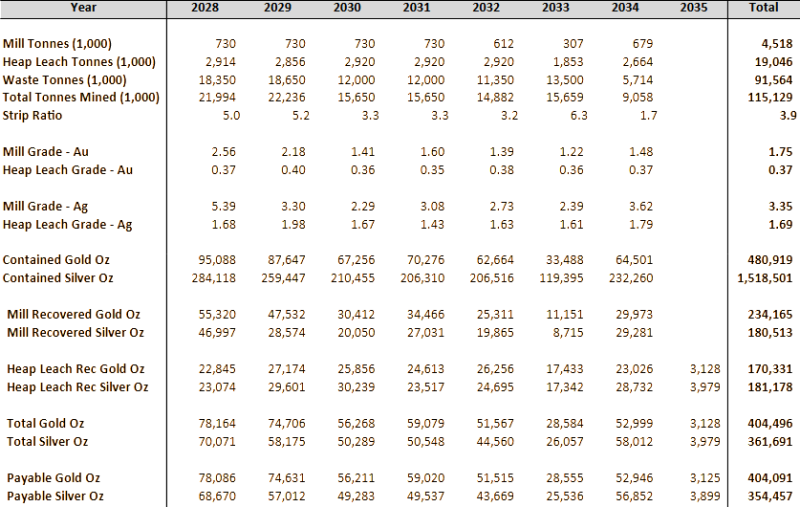

Table 4: Annual Detail of Tonopah PEA Production Schedule

Click Image To View Full Size

PEA Study Economic Analysis

The PEA economic analysis is based on the estimated production schedule, capital costs, and operating costs, and cash flow model prepared by WSP. All information used in this economic evaluation was derived from work completed by WSP and KCA, with support from Viva Gold.

Project economics were evaluated using a discounted cash flow method that measures the before-tax and after-tax NPV of future cash flow streams. The PEA economic model was based on the following key assumptions:

- A gold price of $2,400 per ounce.

- Mine production schedule developed by WSP with a nominal average mining rate of 45,000 TPD with higher levels in the first two years and a mill and heap leach process rate totaling 10,000 TPD of mineralized material.

- A period of analysis of eleven years that includes one year of investment, years of production, and three years to complete reclamation and closure commencing after cessation of mining activities.

- Capital costs as summarized in Table 9 and operating costs as summarized in Table 7 and described in the following sections.

Project economics are based on criteria from the cash flow model that are summarized in Table 5.

Table 5: Economic Analysis Summary

Financial parameters

| Results

| Internal Rate of Return (IRR), Pre-Tax

| 20.6%

| Internal Rate of Return (IRR), After-Tax

| 17.6%

| Average Annual Cash Flow in Production (Pre-Tax)

| $56.8 million

| NPV 5% (Pre-Tax)

| $138.6 million

| Average Annual Cash Flow in Production (After-Tax)

| $52.8 million

| NPV 5% (After-Tax)

| $111.6 Million

| Gold Price Assumption

| $2,400/Ounce Au

| All-In sustaining Cost

| $1,164

| Cash Cost of Production

| $1,269

|

Economic Sensitivity Analysis

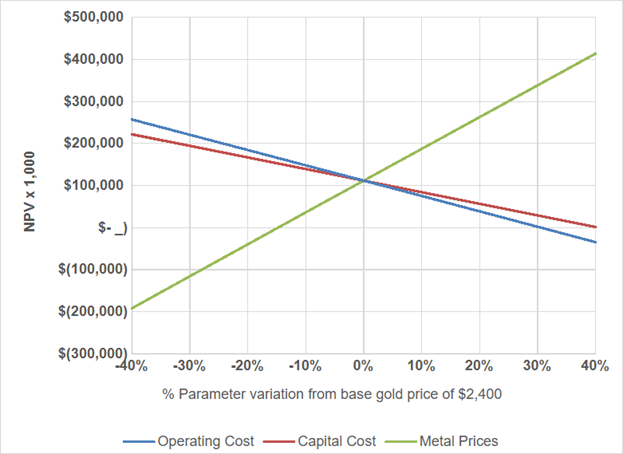

At a current market price level of approximately $3,200 per ounce Au, a 33.3% increase over the base price of $2,400, Tonopah returns a post-tax NPV 5% of $363.6 million and an IRR of 43.4%, demonstrating strong leverage to gold price.

Project sensitivity to Au/Ag price, operating and capital costs are shown in the following Figure 1:

Figure 1: Project Sensitivity to Changes in Price, Capital and Operating Cost

Table 6: Project Sensitivity to Gold Price

Sensitivity to Gold Price

| Gold Price

| NPV 5% (xUSD 1,000)

| 80%

| 1,920

| (38,425)

| 90%

| 2,160

| 36,738

| 100%

| 2,400

| 111,617

| 110%

| 2,640

| 186,451

| 120%

| 2,880

| 261,286

| 130%

| 3,120

| 336,120

| 140%

| 3,360

| 410,955

|

Operating Costs

Table 7: Unit Operating Cost Breakdown

AREA

| UNITS

| COST

| Mine

| $/tonne Material

| 1.95

| CIL Mill

| $/tonne Milled

| 16.43

| Heap Leach

| $/tonne Leach

| 6.62

| Water Systems

| Annual Variable

| $670K to $1.2K

| Gen & Admin

| Annual

| $4.4 million

|

Mine operating costs are based on self-mining, non-contractor rates. Mine operating costs and equipment productivity rates were estimated from first principals by WSP using equipment productivity handbooks, reference guides and databased information. The mine is anticipated to operate 365 days per year utilizing two twelve-hour shift per day, with a total of four operating crews working on a four-day rotational schedule.

Process costing is based on the processing design criteria shown in Table 8.

Table 8: Processing Design Criteria Summary

Item

| Design Criteria

| Annual Tonnage Processed

| 3,650,000 tonnes

| Production Rate

| | Crushing Rate

| 10,000 tonnes/day, 365 days/year

| CIL Milling Rate

| 2,000 tonnes/day, 365 days/year

| Leach Pad Stacking Rate

| 8,000 tonnes/day, 365 days/year

| Recovery

| | High-grade Mill Au Recovery, Average

| 93%

| Low-grade Heap Leach Au Recovery, Average

| 75%

| Operation

| 12 hours/shift, 2 shifts/day, 7days/week, 365 days/year

| Leach Cycle

| 120 days

| Reagents

| | High-grade Mill NaCN Consumption, kg/t

| 0.58

| Low-grade Heap Leach NaCN Consumption, kg/t

| 0.26

| High-grade Mill CaO Addition, kg/t

| 0.60

| Low-grade Heap Leach Cement Addition, kg/t

| 4.0

|

Plant and general and administrative (“G&A”) operating costs were estimated by KCA using first principals based on the second quarter 2025 US dollars and are presented with no added contingency based upon the design and operating criteria present in this release and are considered to have an accuracy of +/-35%. Sales tax was not included in the operating cost estimate. G&A costs include annual premiums for reclamation surety bonds. Water system costs were estimated by Piteau Associates of Reno Nevada and are estimated to have an accuracy of +50%/-25%.

Capital Costs

Table 9: Capital Cost Estimate

Description

| Costs ($,000)

| Pre-production Capital

| | Process and Infrastructure Capital including Spare Parts

| $120,640

| Mining Capital including Shops, and Equipment lease down payment

| $21,435

| Dewatering Systems

| $9,898

| NSR Royalty Option Exercise

| $1,000

| Indirect, First Fills, & Owners Costs

| $16,271

| Engineering, Procurement & Construction Management (“EPCM”)

| $17,228

| Contingency

| $33,436

| Total Pre-Production Capital

| $219,909

| | | | Initial Working Capital Requirement

| $22,160

| | | | Sustaining Capital

| | Leach Pad Expansion

| $9,597

| Mine Equipment Lease Payments

| $55,257

| Dewatering systems

| $5,580

| Total Sustaining Capital

| $70,434

| | | | Reclamation & Closure Allowance

| $12,000

| Initial Reclamation Bond Restricted Cash Collateral

| $4,740

|

Process and infrastructure capital can be divided into two components: preproduction capital for crushing, leaching systems, and infrastructure with a total preproduction capital cost of approximately $119.5 million including all contingencies and EPCM; and mill circuit costs of $52.5 million all inclusive

All process and infrastructure equipment and material requirements are based on the design information as determined by KCA. Capital cost estimates were developed based on budgetary project specific quotes or recent quotes from similar projects in KCA’s files for all major and most minor equipment. Where recent quotes were not available, reasonable cost estimates or allowances were made based on cost guide data. All capital cost estimates were based on the purchase of equipment quoted new from the manufacturer or to be fabricated new. Capital cost estimates were based on the second quarter of 2025 US dollars and are considered to have an accuracy of +/-35%.

Mine equipment cost is based primarily on a Financing Proposal received from Caterpillar Financial Services Corporation data June 18, 2025. The fleet consists of eleven-100 tonne CAT 777 haul trucks with three CAT 992 loaders, three CAT MD6250 drills and associated auxiliary equipment. Terms include a 20% down payment and the equipment is leased over a three-year period in equal payments of principal and interest. Equipment is purchased with a $1.00 purchase option at the end of the lease. Mine infrastructure, indirect and contingency costs were based on similar projects in WSP’s files and reasonable cost estimates or allowances were made based on cost guide data.

Dewatering capital was estimated to account for the drilling of interceptor wells in surface gravel’s and basement rock, and the construction of HDPE pipeline to convey water directly to valley floor re-infiltration basins where clean water is discharged directly back into valley floor gravels. Royalty cost reflects the cost required to exercise the option to acquire 1% of the Tonopah 2% net smelter return royalty.

Project Closure and Environmental Closure Bonding

Federal and State agencies require a reclamation bond to ensure completion of reclamation and closure of Tonopah, estimated at $23.7 MM, if performed by the State. Actual closure costs if performed using existing mining equipment and personnel are estimated at $12.0 million. Viva anticipates using a Surety policy to cover bond costs which would include providing 20% cash collateral into an interest-bearing restricted cash account and paying an annual surety premium estimated to be $380,000, which is included in G&A costs.

Mine Permitting

Permits required for the proposed surface mining operation will include, but not be limited to, Bureau of Land Management Mine Plan of Operation/National Environmental Policy Act analysis, Environmental Impact Statement, Amended Nevada Mining Reclamation Permit, Nevada Water Pollution Control Permits, Air Quality Operating Permit, Liquified Propane Gas license, Nevada water rights, and Nevada Industrial Artificial Pond permit.

Recommended Forward Studies

WSP makes the following recommendations:

- A diamond drill core program to capture additional data such as specific gravity measurements, core recovery, rock quality designation RQD), and the location and angles of major faults to further refine tonnage estimates for the project and existing structural interpretations.

- Developing an alteration model could improve understanding of its impact on gold mineralization and potentially identify new drill targets.

- A more detailed tradeoff study between leasing production equipment vs. purchasing should be undertaken (perhaps even a hybrid of the two options) to assess if up-front capital can be reduced and evaluate the effects on operating costs.

- More detailed phasing of the open pit at a PFS level should be undertaken given the nature of the grade and strip ratio of the deposit to help focus on bringing more high-grade material up front to help offset the initial capital cost payback.

KCA has made recommendations for additional metallurgical studies including:

- High-grade mill and gravity variability testing

- Variability column testing at various crush sizes (9.5mm, 12.5 mm, 25 mm and 38mm) for a 120 to 180-day period.

- Perform additional characterization work.

Samples for KCA’s metallurgical program may be captured in the diamond core program recommended by WSP. The cost of a 1,000 meters PQ drill program including assay, teleview/oriented core study is approximately $500,000 not including additional cost for specific gravity testing. Quotations for metallurgical testwork and updated geotechnical study are in process.

Environmental study recommended by Lewis Consulting LLC, Viva’s long term environmental consultant, includes:

- Ongoing baseline study work for environmental monitoring, cultural resources surveys, biological studies, and hydrogeologic studies.

- Construction of one upgradient and two downgradient groundwater monitoring wells.

- Thirty-day aquifer tests from the existing site bedrock and alluvial production/monitoring wells, should be conducted to support the numerical groundwater model required for Federal and State permitting.

- A program to test the capacity of alluvial soils to allow infiltration of excess mine dewatering water.

- A Class III cultural resources survey should be completed for those areas within the projected Project boundary that have not been surveyed in more than ten years.

- Two years of Golden Eagle and Raptor aerial surveys should be completed to develop plans and permits if necessary to ensure compliance with the Bald and Golden Eagle Protection Act.

It is anticipated that these recommended environmental study activities will cost approximately $900,000.

Qualified Person

Brian Thomas, P.Geo. of WSP, is the qualified person, as defined by NI 43-101, responsible for the preparation of the MRE. Jason Baker, P.Eng. of WSP, is the qualified person, as defined by NI 43-101, responsible for the mining method. Rick McBride, P.Eng. of WSP, is the qualified person, as defined by NI 43-101, responsible for integration of the costs into the cashflow model. Caleb Cook, PE is qualified person for metallurgy and processing. James Hesketh, MMSA-QP, has approved the scientific and technical disclosure contained in this press release. Mr. Hesketh is not independent of the Company; he is an Officer and Director.

About Viva Gold Corp:

Viva Gold is led by CEO James Hesketh, a 40-year veteran in the mining space who has led the development and construction of eight other mines around the world throughout his career. James has surrounded himself with equally experienced mining professionals both on the management team and the board.

Viva Gold trades on the TSX Venture exchange “VAU”, on the OTCQB "VAUCF" and on the Frankfurt exchange "7PB". Viva currently has ~145.2 million shares outstanding and boasts a best-in-class management team and board with decades of gold exploration and production experience. The Company is advancing its high-grade Tonopah Gold Project in mining friendly Nevada with the support of several institutional shareholders. More information can be found on sedar.com and please visit our website: www.vivagoldcorp.com.

Viva is committed to developing the Tonopah Gold Project in an environmentally and socially responsible fashion. These values are aligned with management’s core values and permeate throughout our decision-making process.

For further information please contact:

James Hesketh, President & CEO

(720) 291-1775

jhesketh@vivagoldcorp.com

Graham Farrell, Investor Relations

(416) 842-9003

graham.farrell@vivagoldcorp.com

Forward-Looking Information:

This news release contains certain information that may constitute forward-looking information or forward-looking statements under applicable Canadian securities legislation (collectively, “forward-looking information”), including but not limited to forward-looking information related to Mineral Resource estimates for the Project. The material factors that could cause actual results to differ materially from the conclusions, estimates, designs, forecasts or projections in the forward-looking information include any significant differences from one or more of the material factors or assumptions that were set forth in this press release including geological and grade interpretations and controls and assumptions and forecasts associated with establishing the prospects for economic extraction of gold mineral resource and preliminary economic analysis at the Tonopah Gold Project. This forward-looking information entails various risks and uncertainties that are based on current expectations, and actual results may differ materially from those contained in such information. These uncertainties and risks include, but are not limited to, the strength of the global economy, inflationary pressures, pandemics, and issues and delays related to permitting activities; the price of gold; operational, funding and liquidity risks; the potential for achieving targeted drill results, the degree to which mineral resource estimates are reflective of actual mineral resources; the degree to which factors which would make a mineral deposit commercially viable are present; the accuracy of capital and operating cost estimates; the variability of actual from estimated gold recovery; potential for geotechnical issues; the risks and hazards associated with drilling and mining operations; and the ability of Viva to fund its capital requirements. Risks and uncertainties about the Company’s business are more fully discussed in the Company’s disclosure materials filed with the securities regulatory authorities in Canada available at www.sedar.com. Readers are urged to read these materials. Viva assumes no obligation to update any forward-looking information or to update the reasons why actual results could differ from such information unless required by law.

Cautionary Note to Investors --- Investors are cautioned not to assume that any "measured mineral resources", "indicated mineral resources", or "inferred mineral resources" that the Company reports in this news release are or will be economically or legally mineable. United States investors are cautioned that while the SEC now recognizes "measured mineral resources", "indicated mineral resources" and "inferred mineral resources", investors should not assume that any part or all of the mineral deposits in these categories will ever be converted into a higher category of mineral resources or into mineral reserves. These terms have a great amount of uncertainty as to their economic and legal feasibility. Under Canadian regulations, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in limited circumstances. Further, "inferred mineral resources" have a great amount of uncertainty as to their existence and as to their economic and legal feasibility. It cannot be assumed that any part or all of an inferred mineral resource will ever be upgraded to a higher category. The mineral reserve and mineral resource data set out in this news release are estimates, and no assurance can be given that the anticipated tonnages and grades will be achieved or that the indicated level of recovery will be realized.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Definitions

“All-in sustaining costs” is a non-IFRS or US GAAP financial measure calculated based on guidance published by the World Gold Council (“WGC”). The WGC is a market development organization for the gold industry and is an association whose membership comprises leading gold mining companies. Although the WGC is not a mining industry regulatory organization, it worked closely with its member companies to develop these metrics. Adoption of the all-in sustaining cost metric is voluntary and not necessarily standard, and therefore, this measure presented by the Company may not be comparable to similar measures presented by other issuers. The Company believes that the all-in sustaining cost measure complements existing measures and ratios reported by the Company. All-in sustaining cost includes both operating and capital costs required to sustain gold production on an ongoing basis. Sustaining operating costs represent expenditures expected to be incurred at the Project that are considered necessary to maintain production. Sustaining capital represents expected capital expenditures comprising mine development costs, including capitalized waste, and ongoing replacement of mine equipment and other capital facilities, and does not include expected capital expenditures for major growth projects or enhancement capital for significant infrastructure improvements.

“Cash cost per gold ounce” is a common financial performance measure in the gold mining industry but has no standard meaning under IFRS or US GAAP. The Company believes that, in addition to conventional measures prepared in accordance with IFRS or US GAAP, certain investors use this information to evaluate the Company’s performance and ability to generate cash flow. Cash cost figures are calculated in accordance with a standard developed by The Gold Institute. The Gold Institute ceased operations in 2002, but the standard is considered the accepted standard of reporting cash cost of production in North America. Adoption of the standard is voluntary, and the cost measures presented may not be comparable to other similarly titled measures of other companies. |