Saks Fifth Avenue

Yesterday, January 14th, 2026, Saks filed Chapter 11 Bankruptcy in Texas Court assigned to Judge Alfredo R Perez. SAKS has Willkie Farr & Gallagher LLP (“WF&G”) and PJT Partners L.P. (“PJT”) on board to support them.

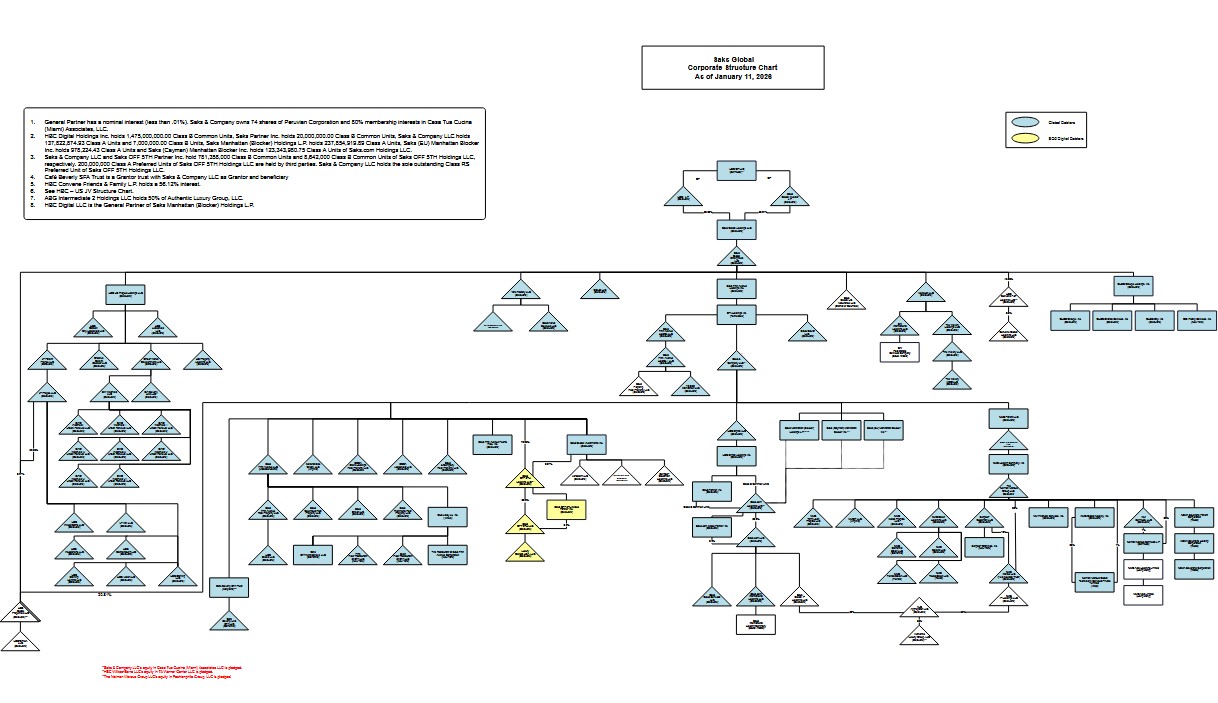

SAKS at the time of filing has 14,610 full-time employees (FTE) and 2,220 part-time employees. Below is a look at the complex corporate structure for SAKS:

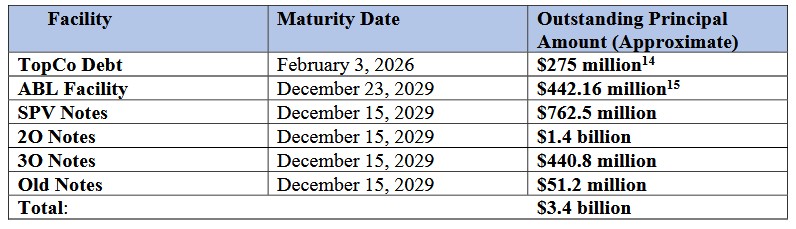

At the time of this filing the company has ~$3.4B in debt with

- $275M senior secured term loan

- $442.16M in loans

- $762.5M in SPV notes

- $1.4B in 2O notes

- $440.8M in 3O notes

- $51.2M "old notes"

Below is a breakdown of all the players in this case:

| Name | Type | Added | | Ad Hoc Group of Secured Noteholders | Other Prof. | 01/14/2026 | | Amazon.com Services LLC | Interested Party | 01/14/2026 | | Axonic Coinvest II, LP | Interested Party | 01/14/2026 | | B.H. Multi Color Corp. | Creditor | 01/14/2026 | | B.H. Multi Com Corp. | Creditor | 01/14/2026 | | Bank of America, N.A. | Interested Party | 01/14/2026 | | Bexar County | Creditor | 01/14/2026 | | Brookfield BPY US Retail Holdings, LLC | Interested Party | 01/14/2026 | | Brookfield Properties Retail Inc. | Creditor | 01/14/2026 | | Callodine Commercial Finance, LLC | Creditor | 01/14/2026 | | Capital One, National Association | Creditor | 01/14/2026 | | Comenity Capital Bank | Creditor | 01/14/2026 | | David Yurman Enterprises LLC | Creditor | 01/14/2026 | | Elsa Schiaparelli SAS | Interested Party | 01/14/2026 | | Ermenegildo Zegna Group | Creditor | 01/14/2026 | | Fort Bend County | Creditor | 01/14/2026 | | Gorski Group Ltd. | Interested Party | 01/14/2026 | | Goyard NM Chicago LLC | Creditor | 01/14/2026 | | Horizon Group Properties, Inc. | Creditor | 01/14/2026 | | Kering Americas, Inc | Creditor | 01/14/2026 | | Khaite LLC | Creditor | 01/14/2026 | | LVMH Mot Hennessy Louis Vuitton Inc. | Creditor | 01/14/2026 | | Local 1102 RWDSU UFCW | Creditor | 01/14/2026 | | Louis Vuitton USA Inc | Creditor | 01/14/2026 | | Luxury Outlets USA, LLC | Debtor | 01/14/2026 | | Margot McKinney | Creditor | 01/14/2026 | | National Realty & Development Corp. | Creditor | 01/14/2026 | | Pension Benefit Guaranty Corporation | Creditor | 01/14/2026 | | Richemont North America, Inc. | Creditor | 01/14/2026 | | Richline Group, Inc. | Creditor | 01/14/2026 | | SF Wilshire BH, LLC | Creditor | 01/14/2026 | | SMCP USA Inc. | Creditor | 01/14/2026 | | Saks Global Enterprises LLC | Debtor | 01/14/2026 | | Saks OFF 5TH Holdings LLC | Debtor | 01/14/2026 | | Saks OFF 5TH LLC | Debtor | 01/14/2026 | | Saks OFF 5TH Midco Partner Inc. | Debtor | 01/14/2026 | | Simon Property Group, L.P. | Creditor | 01/14/2026 | | Street Retail, LLC | Creditor | 01/14/2026 | | Stretto | Other Prof. | 01/14/2026 | | US Trustee | U.S. Trustee | 01/14/2026 | | Unique Designs, Inc. | Creditor | 01/14/2026 | | Urban Edge Properties | Creditor | 01/14/2026 | | V Opco, LLC | Creditor | 01/14/2026 | | Westfield, LLC | Creditor | 01/14/2026 | | Workers United New York New Jersey Regional Joint Board | Creditor | 01/14/2026 |

In total there are 112 cases jointly filed with SAKS and jointly administered under case: 26-90103 . Old rule of thumb was a bankruptcy filing can eat up to 10-20% of a firms enterprise value (EV) and with 112 cases going on it's easy to see how - those lawyers are eating well!

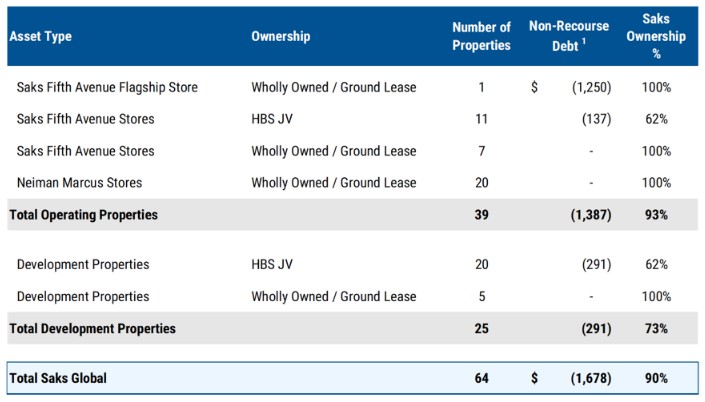

In the filing it is stated that collectively SAKS owns or ground leases 8.4 million of square feet in the U.S. real estate. The company has a joint-venture where they own 62.4% of the equity interests with Simon Property Group called the HBS JV. The HBS JV has around 31 properties inside of it and each property is held in a separate special purpose entity (SPE). HBS JV has leased property back to SAKS. More detail in this but below is a summary of their property holding:

SAKS also has another joint-venture with Authentic Brands, the owner of 50 global brands like Reebok, Champion, and Nautica, where each owns 50% of the JV titled "Authentic Luxury Group LLC".

My favorite statement from the filing "Despite the growth potential of Saks Global and synergies expected (and partially realized) from its recent acquisitions, the Company has been negatively impacted by sustained liquidity issues. Nonetheless, it is not a declining brick-and-mortar business."

SAKS has been reported to have liquidity issues for a long while now. It was reported in Forbes on August 7th, 2024 that "on the other hand, Ryan Babenzien, Founder of sneaker brand Greats (now owned by Steve Madden), says that Saks has stopped paying them “even though we had 100% sell-through.” According to Pymnts.com, CTE Watch Company is reporting they are owed hundreds of thousands of dollars by Saks as well. Saks says those two vendors sell to Saks OFF Fifth and not to Saks Fifth Avenue.

It raises a question: How can Saks’ parent spend $2.65 billion on an acquisition and still have vendors to one of their brands who say they don’t get paid?". Either the brand was in decline or they were grossly mismanaging money but I suspect the courts will uncover some fun!

But wait!

The lawyers in the first day filings noted that this is not a declining brick-and-mortar business but then just a few paragraphs later state "during the Debtors’ fiscal year ending February 1, 2025—which included the

Debtors’ acquisition of Neiman Marcus and Bergdorf Goodman—consolidated total revenue

declined by 13.6% year over year, largely driven by lower retail sales across all channels.". Sure looks like decline to me and more so when you couple in they stopped paying vendors.

The case then goes on to talk about the liability management exercise (LME) SAKS did in the summer of 2025 (as I noted in my original post in December). The company secured $600M of new money (before fees and taxes of course) and it allowed them to perform creditor-on-creditor violence and take out $115M of prior notes at a discount to face. The intent of the LME was to give the company more time but also with the money to pay some aged payables and restore inventory to normal levels but the lawyers then state "the proceeds alone were insufficient to normalize aged payables or restore inventory flow to planned levels ahead of the

2025 holiday season.". Interesting, did any of the prior creditors look at how bad the situation was when this LME took place? It would seem not as if an LME done in August 2025 lead to a chapter 11 filing by January 2026 then someone didn't do their work OR possible (100% speculation on my end) management misled creditors on health.

I have written a lot about QVC on the Qurate thread, but these moves mentioned in the first day filing echo a lot of recent moves we have also seen with QVC:

"To further the Global Debtors’ evaluation of strategic alternatives, the Global Debtors appointed (i) me as their Chief Restructuring Officer and (ii) independent managers Paul Aronzon and William Tracy (the “Independent Managers”) to the board of managers of HBC GP LLC (the parent company of all Debtors) as well as to the governing body at each subsidiary Global Debtor that is not member-managed, and formed a special committee of the board comprised of the Independent Managers at the applicable entities (the “Special Committee”). In addition, the Board of Managers of HBC GP LLC approved the appointment of Scott Vogel to serve as an independent director of HBC GP LLC, each subsidiary Global Debtor that is not member-managed, and to the Special Committee, subject to the entry of the interim order approving the DIP Facilities (defined below)".

The filing also stated in late 2025 SAKS attempted a series of other things with key equity holders to prevent a petition filing in court. These things include sale of assets, financing alternatives with new/existing lenders, and holistic restructuring transactions, but as it goes they were not able to get enough support and into Chapter 11 we go.

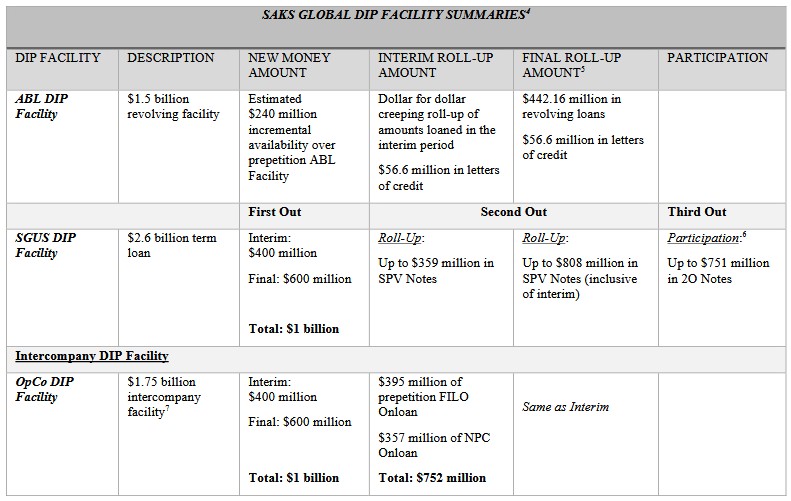

In December 2025 the company then engaged key creditors and some third-party investors on terms for a debtor-in-possession (DIP) loan. This ad-hoc group of creditors and investors owns 72% of the existing SPV notes and 50% of the existing 2O notes. Paul, Weiss, Rifkind, Wharton & Garrison LLP, FTI Consulting, Inc. and Lazard Frères & Co, LLC were all engaged to support the DIP. In total the DIP will provide around $1.75B in new money to SAKS during the course of the case and DIP lenders offered to backstop a $2.6B delayed draw term loan under the "SGUS DIP FACILITY" which consists of $1B of new money available in three draws and up to $808M in second out loans as a cashless roll-up of prepetition SPV notes and up to $751M of third out DIP loans under the "SGUS THIRD OUT DIP LOANS". The SGUS DIP FACILITY is paired with $500M in exit financing to help the company exit bankruptcy.

The case was asked to be jointly administrated to reduce costs and facilitate the entire process by avoiding duplicate hearings, notices, and orders. It was stated this joint filing is for procedural processes only.

Given the layers here this may be in court for a while. A typical prepackaged bankruptcy could be 45-60 days but here we have a good 'ol freefall. I suspect given the size of the DIP that a lot of the older 2O or 3O are not going to see much, maybe new equity? Depends on how much of the 2O are in the third out SGUS DIP FACILITY.

It will be interesting to see where this lands and will continue to report on what I read as filings come out.

-Sean |