Hi 60,

Quick read but will give me $0.04 on this write-up from TJ.

<< If you buy QVCGA, there is $250M in cash sitting at holdco, unencumbered by the Credit Agreement. There is also a 60% stake in CBI that is unencumbered by the Credit Agreement.>>

This is true, but that cash is not self-funding and they will eventually run out. Possible he sees this as the company would be liquidated and return said cash to shareholders? Otherwise $250M in today's world and CBI itself isn't some prized pig.

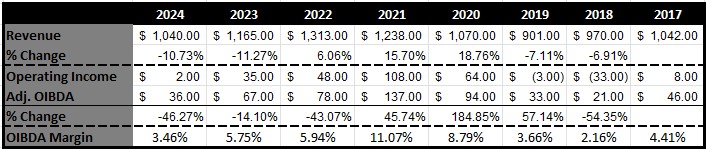

Adj. OIBDA of $36M last year with an OIBDA margin of 3.46%. And I know a few keep holding out for a "housing boom" but look at pre-2020 and the Adj. OIBDA is pretty much in-line today with historical levels. The probability of getting what we saw in 2020-2021 is very low at this stage of the cycle.

If we average out the last three years and assume Cornerstone gets to an Adj. OIBDA of $60.33M then at best this thing is valued at 2-3x for a low margin retailer and that gets them a valuation of maybe $120.67M - $181M and that's before transactions fees and taxes. This low valuation isn't even enough to stake as collateral and raise anything meaningful to fund an acquisition if they loose QVC, Inc.

Despite what Delaware law may state if this goes a legal route then one could argue Dr. Malone and Maffei bled the company capital to fund themselves for years. There's a lot of legal murky area here that isn't as clean for QVCGA as TJ makes it seem. If a lawsuit springs then that's more capital out the door. It isn't just John and Greg that hold them as they're in a few ETF's and held by others as well. Not sure how valid but Yahoo! shows only 8.33% are held by insiders.

<< All liability management exercises are going to be based off of the facts and circumstances of the individual company’s situation. What does management want? What do the credit documents allow?>>

This is an oversimplification.

Greg Maffei has indeed been a shareholder manager and made many returns to shareholders over time. I just shared with someone else on Michael Burry's Substack where I stated "in 2019 they spent $392M on share buybacks, $70M in 2020, and $365M in 2021. By end of 2021 shares outstanding for series A were 371.1M down from 2020 level of 386.7M. Total debt was sitting at $6.94B in 2020. They also issued the preferred shares to pay out additional dividends to shareholders.

By Q3 2025 debt has declined from $6,936M to $5,893M but interest expense in 2020 was $408M and in 2024 it was $468M. They can no longer buyback stock, preferred is in tanks and dividend halted, EBITDA went from $1.96B in 2019 to trending towards $850M in 2025, and shareholders (outside of declines) have been diluted 1.5% each year since 2021 as adjusted share count is now 393.3M."

This situation is not a time to think they're worried about shareholder returns when their fiduciary duty is to literally stay afloat. They wasted capital by buying shares back instead of just spending the $827M on debt reductions and ended up in 2025 with a higher share count because management incentives diluted current equity holders. 100% wasted capital. Then they paid the preferred dividend for YEARS while the company bled when they could have halted to conserve cash and pivot to debt reductions.

When you are hiring restructuring experts on your main board and forming a new board at your OpCo and restating bylaws this isn't to save the equity. This over-reliance on Greg Maffei is going to make these guys go broke.

I also wrote to that Substack user on Dr. Malone:

"Then you had Dr. Malone sell his B voting shares to Maffei which triggered the change of control and they were sued by the company. Result ended with Malone being banned from running again for the board. November 2024 Maffei “stepped” down from Liberty Media and as such is only the Chairman of QVC Group and QVCG lost all the core shared assets they had with Liberty.

Dr. Malone has ~608,460 shares of QVCGA stock for an economic interest of maybe $6,388,519.62 ($10.50/s as of 1/22/2026). For an 85 year old wrapping up his empire this is nothing and likely already mentally written off - especially since he isn’t even on the board anymore. 100% not something one invests more capital or sweat equity into saving at 85".

Again putting their faith in these guys for stuff they did 20 years ago is going to cost them their capital. TJ wrote:

<<all liability management exercises are going to be based off of the facts and circumstances of the individual company’s situation.>>

And yet uses prior Malone/Maffei moves as if the individual situation is even close to the same. It isn't.

<< It allows for over $2 billion of loans to be made to unrestricted subs/non-guarantor subs, which would prime existing lenders. The banks already signed off on this. Consent isn’t required, because it’s already been given. >>

Allows does not mean it's happening. The credit agreement is specifically designed this way so the company can go to the banks and get more capital when needed without needing a new agreement. They are not getting new capital from these lenders. This is why they formed a 75% co-op to ensure anything is blocked out.

The company can make whatever pro-forma adjustments to claim the capital they can get on the available revolver draw, but the rest isn't coming as easy as he makes it seem.

<< I’ve seen many people suggest that the banks need to “sign off” on whatever happens next. They don’t need to sign off on anything. QVC can just do it. They were given the green light back in 2021.>>

And here TJ assumes because an agreement allows it that is can be done. QVC is listed as a going concern right now and the banks have boarded the vessel and are making their way to the captain deck. They already formed a 75% co-op and have hired Simpson Thatcher and Lazard if they wanted to extend more capital or even do a simple A&E this wouldn't be done. This is what you do when you're preparing to take the company through a prepackaged bankruptcy. They already traded term sheets which is beyond typical.

Again Ben Oren started revolver A&E talks back in November 2024 and expected an update by Q1 or Q2 2025. By Q1 2025 Maffei had "stepped down" from Liberty and the shared resources were gone and Bill Wafford who stepped into CFO/CAO role was being asked if a A&E was even on the table. By Q2 2025 there was no live Q&A and they borrowed $1,050M more from their credit facility ($75M in Q2 and then the after period $975M draw).

The banks can A&E, sure, and they will likely want a higher interest rate, tighter cash covenants, and various other things. If QVC management doesn't want to play or starts doing stupid things all the banks need to do is wait for October 2026 and call the loan and then the bond holders can call in too and you get a freefall Chapter 11 anyway.

And what are you going to do? Make a move against the banks? This isn't the bond community where you can perform creditor-on-creditor violence more easily because of fragmentation. They will need the banks in the future and Maffei will still need them for other organizations too.

And speaking of those relationships, remember how I also shared what happened at $SIRI, another Maffei company, when they A&E their credit facility in 2025? The financials stated:

"On August 20, 2025, Sirius XM entered into an amendment to, among other things, increase the Credit Facility to $2,000 and extend its maturity to August 31, 2030. Sirius XM's obligations under the Credit Facility are guaranteed by certain of its material domestic subsidiaries, including Pandora and its subsidiaries, and by Sirius XM Inc. and are secured by a lien on substantially all of Sirius XM's assets and the assets of its material domestic subsidiaries. Borrowings bear interest at the Secured Overnight Financing Rate (“SOFR”) plus an applicable rate determined by Sirius XM’s debt to operating cash flow ratio, and we pay a variable commitment fee on unused commitments of 0.25% per annum as of September 30, 2025. The amendment also adds a springing maturity feature which will automatically accelerate the maturity date of the Credit Facility to a date 91 days prior to the stated maturity of certain of Sirius XM’s long-term debt instruments, including Sirius XM’s 2026, 2027, 2028, 2029 and 2030 Senior Notes and the Delayed Draw Incremental Term Loan, if at such date Sirius XM does not have sufficient liquidity to repay the maturing obligations. Liquidity for this test is defined as the sum of (i) unrestricted cash and cash equivalents and (ii) available borrowing capacity under the Credit Facility. "

<< Kirkland & Ellis, who QVC has hired, are the market leaders in liability management transactions, and their expertise is to take advantage of these loose credit documents and find out-of-court solutions to force creditors’ hands.>>

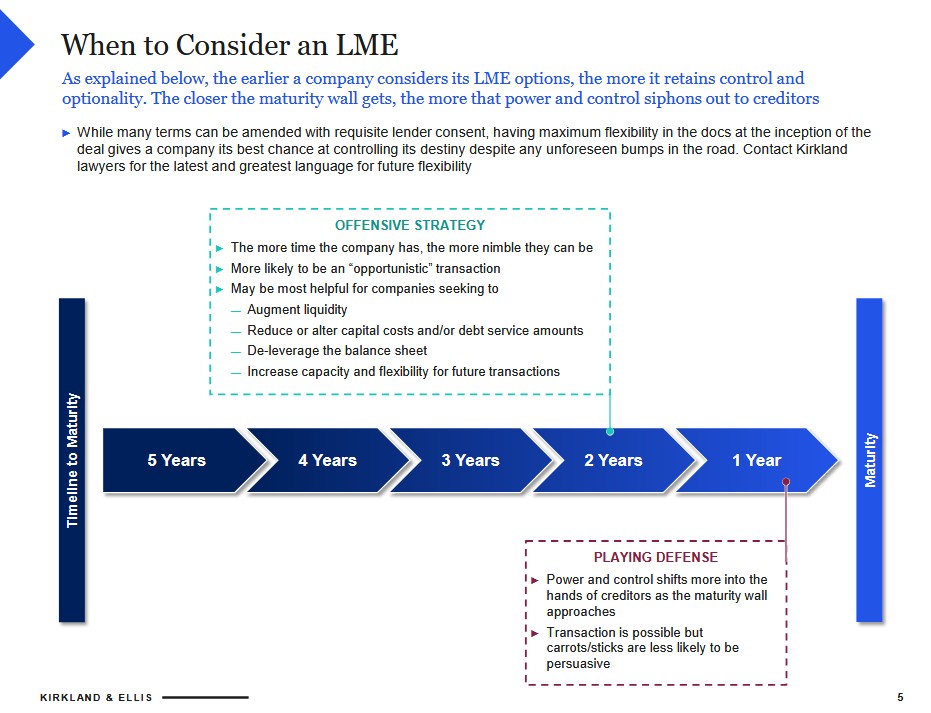

And from Kirkland and Ellis own presentation once you are within one year of a maturity you are playing defense and as of January, almost February, 2026 QVC credit facility which ows $2.9B is listed as current and the company has going concern language in their financials. By Kirklands own view, QVC is now playing defense and not here to play offense:

<< The Wall Street Journal already reported that QVC’s banks formed a co-op in preparation for a liability management transaction.¹>>

What the WSJ article fully stated was "lenders holding more than 75% of QVC’s revolving loan have signed onto the agreement to prepare for possible liability management transactions or other restructuring moves, said the people." so I find it interesting we're just glossing over the "other restructuring moves" statement because it doesn't fit the LME thesis. The company likely tried an LME as is usually the case (usually also comes with a bankruptcy threat too) and yet here we are, more value bled, banks have more exposure diluting their recoveries, and QVC is paying their management in a KEIP style cash bleed plus paying two board heavyweights.

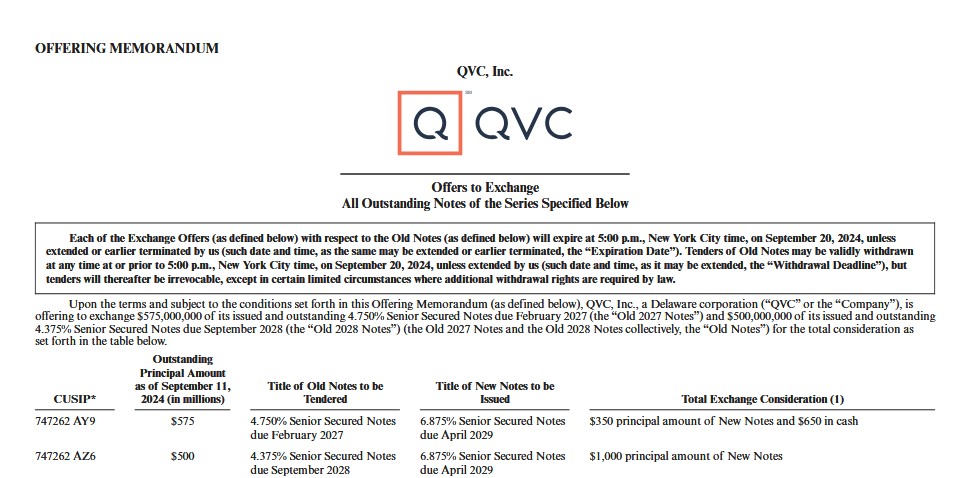

Also again they did an LME of sorts in September 2024 when Morgan Stanley led Project Nomi for the 2029 debt exchange:

While there was not any vicious creditor-on-creditor moves here with drop-downs or uptiers, this was a liability move and value has not improved a year later. Those same bonds are trading at a discount to PAR.

And remember the collateral for all the senior lenders is the equity of QVC, Inc. So you can try drop-downs or uptiers but the collateral is what? Customer lists, $400M of book value P&E, but you can't move an entire company and whatever collateral they can move isn't getting them enough to de-lever without bleeding more cash. The interest from a private credit lender alone would likely offset any savings from a senior secured LME AND most of their senior debt is termed 2034-2068 so all they would do is push maturities up and likely have to file anyway.

We can look at J Crew as an example and we can also look at SAKS who literally did a creditor-on-creditor LME August of 2025 and is now in freefall Chapter 11 as of January 2026. An LME is to buy time, and not to deleverage out of court. I would challenge QVC bought time since 2024 when they used their credit facility & cash to take out the 2024 notes, 2025 notes, and majority of 2027/2028 and extend to 2029. Their earnings potential has not improved.

<< The credit agencies also said they expect a liability management transaction.>>

And S&P specifically stated on an LME "the negative outlook reflects that we could lower our ratings if we believe a default scenario is inevitable within the subsequent six months or the company announces a debt exchange that we view as distressed.

<< A moat is a unique characteristic of a business that is hard for a competitor to replicate. I don’t think people understand how hard it is logistically to do what QVC does.>>

From a traditional QVC view I would agree. To get on TV and have a channel or two dedicated to selling a product requires TV agreements, paying for TV personal, expensive equipment, studios, and whatever else. In 2026? I don't see the world as rosy as he does.

It was reported by Wired in Q3 2025 that TikTok shop in the US did about $4 - $4.5B in gross sales and I have QVC in that same time doing maybe $25-30M which at the $30M end is about 0.75% of TikTok US sales at $4B mark. It would "seem" that there are a few that can do what QVC does.

For Q4 I have QVC on TikTok around maybe $50-54M in gross revenue and meanwhile between Black Friday and Cyber Monday TikTok shop in the US did $500M. Again it would seem others can indeed do what QVC can do.

Remember when I shared that report from Business Insider that "the app drove over $500 million in US sales during the four-day stretch between Black Friday and Cyber Monday.

Household-name brands like Disney, Samsung, and Ralph Lauren, once hesitant to sell in an unproven marketplace, all signed up for TikTok Shop in the US in recent months. Razor brand Harry's is paying as much as $150,000 a year to hire an in-house "TikTok Shop manager" who will monitor the app full-time".

Harry's Razor is paying $150K a year for someone to just manage TikTok shop. Wonder what Disney or others are spending? As more come into the playing field it dilutes QVC and they have to outspend to get the views. As it stands just over the past 22 days they have averaged 4.6K transactions per day which is a steep decline from the 12-16K they were hitting when they likely paid for aggressive algorithm placement in Q4 2025 as almost every retailer would be doing. Now spending normalized. As TikTok gets bigger it attracts more vendors and BAM that's more QVC needs to spend to gain eyeballs.

QVC would need to average 30K transactions a day for 365 days a year and average a $45 average transaction value to get to $492.75M in gross revenue (5.5% of their 2024 annual revenue of $8,997M). Then you figure 14.5% for returns which puts them to $421.30M (4.7% of 2024 revenue) and with an 11% EBITDA margin even that's only an impact of $46.34M and with a 50% core cash flow to EBITDA conversion it's $23.17M of core cash flows. And that's assuming 11% EBITDA margin holds and it's not worse on TikTok - we have no margin analysis so who can say but we do know it's pay-to-play.

<< Who’s going to compete with that at this scale? Who has the ability to take 25% of their fulfillment capacity to focus on one product? Who has the buying teams? Who can generate the amount of video content that they do? Who has the vendor network? QVC already has over 100,000 affiliates working with them. Who else can support that? QVC can, because if a product goes viral, they’re already prepared to sell millions in a single day of a single product. And then they have a completely different product for the next day. And the day after that.>>

Well given in Q3 alone TikTok shop did $4B - $4.5B and QVC was around $25-30M I would say there appears to be a few folks who can. They may not be QVC but there is clearly numerous others. Even the Black Friday - Cyber Monday should be an alarming view into the size.

I just cannot get on board with these views - not that it matters that I do either. The management tried the turnaround with Project Athens and are again bleeding "OIBDA" and this year have posted some bad cash flow numbers. They've paid management their stock rewards in cash, paid two restructuring experts $50K each a month, brought on two more at the OpCo and restated the by-laws, and everything else I've shared. There is far too much risk to be as bullish as many are.

Happy investing,

Sean |