[ The "Hard Asset" Hedge You have a robust defense against currency devaluation and inflation.- Holdings: SLV (5.6%), GLD (3.6%), and IBIT (1.5%).

- Observation: Having nearly 11% of the portfolio in Silver, Gold, and Bitcoin is a bold stance. It suggests a strong "store of value" mindset for the next generation. ]

=> Agreed.

Read your comment and thought -- which can be dangerous ;-)

What's my view the future?

Have mentioned some of the following elsewhere, but this is a longer, somewhat more complete overview.

A summary of Harry Browne's Fail-Safe Investing suggests the following:

Fail-Safe Investing emphasizes wealth preservation over aggressive growth as the path to lifelong financial security, rooted in the recognition that financial markets are inherently uncertain and unpredictable. The book asserts that no one can reliably forecast future economic conditions or eliminate uncertainty, making the acceptance of this reality the starting point for sound financial decisions. Browne distinguishes sharply between investing, which means accepting the general returns available in the markets without attempting to outperform them, and speculation, which involves trying to beat average returns through timing, forecasting, or selective asset choices.[1] According to the author this type of portfolio has the goal of assuring "that you are financially safe, no matter what the future brings" including economic prosperity, inflation, recession or deflation. According to the book this is because some portion of the portfolio will perform favorably during each of those economic cycles. The book calls this type of investment portfolio, a "permanent portfolio" and advocates it be re-balanced once per year so that the 25% allocation is precisely maintained for each asset class. The breakdown is as follows- 25% in U.S. stocks, to provide a strong return during times of prosperity. For this portion of the portfolio, Browne recommends a basic S&P 500 index fund such as VFINX (closed to new investors since publication, replaced by VFIAX, which is also Vanguard 500 Index fund) or FSMKX (Fidelity Spartan 500 Index).

- 25% in long-term U.S. Treasury bonds, which do well during prosperity and during deflation (but which do poorly during other economic cycles).

- 25% in cash in order to hedge against periods of “tight money” or recession. In this case, “cash” means U.S. Treasury bills.

- 25% in precious metals (gold) in order to provide protection during periods of inflation. Browne recommends gold bullion coins.

According to Browne such a permanent portfolio should be safe, simple and stable. Authors Craig Rowland and J. M. Lawson call it a passive style of investing.[2] Last October, The Macro Butler stated: Every investor confined to domestic assets faces the same four flavors of the so-called Permanent Portfolio: Cash, Bonds, Stocks, and Gold — all in their local currency. Now, if you’ve actually done your homework, you already know that stocks and gold don’t care about your currency; they have intrinsic value, which is finance-speak for “real worth that doesn’t vanish when your central bank gets creative.”

Intrinsic value, in theory, is just the present value of all the future cash an asset will generate, discounted for risk — or in plain English, what it’s really worth once you strip away market noise and central bank fairy dust. For dividend-paying stocks, the Dividend Discount Model (DDM) works just fine. For everyone else, the grown-up version is the Discounted Cash Flow (DCF) model, which tallies up future free cash flows plus a terminal value — basically, the “and they lived happily ever after” of finance.

. . .

Gold is the oddball in the asset family—no coupons, no dividends, no earnings calls, and certainly no “guidance.” You can’t run a DCF on it because there are no future cash flows to discount. Yet, it stubbornly holds value while entire currencies come and go. Why? Because gold’s worth isn’t financial—it’s elemental.

Economists like to dress this up in fancy terms: scarcity and indestructibility (you can’t print or destroy it), universal acceptability (everyone from ancient Egyptians to modern central bankers wants it), and monetary independence (it’s nobody’s IOU, so it can’t default). Add in some industrial and jewelry demand—roughly half the market—and you get a hard floor under its price.

In short, gold’s “intrinsic value” comes from what it is, not what it earns. It’s the asset you hold when you stop trusting everyone else’s promises—and history shows that moment comes around more often than most investors care to admit.[3] While Browne's permanent portfolio has four equally weighted quadrants to cover four types of risk, in today's world don't believe all four risks are equally probable. And unlike Browne, due to Uncle's ever growing debt believe the odds of financial repression[4] are much larger from zero, as a result, believe holding long-term U.S. Treasury bonds is foolish -- and dangerous to my wealth.[5]

As a consequence have oriented my portfolios towards equities and PM and have deliberately avoided long-dated government bonds. However, keep some cash 'cause:

- enough of it can, in my experience, transform emergencies into mere inconveniences.

- cash lets me pay my annual RMD without removing dividend paying assets from my tIRA[6].

Also, William J. Bernstein's short, but influential 2013 book, "Deep Risk: How History Informs Portfolio Design"[7] provides a similar perspective -- the four deep risks Bernstein identified that can destroy portfolios are:

- inflation

- deflation

- confiscation

- devastation

When I look ahead at the relatively near future (10-20 years) believe those four risks are also not equally likely.

Why?

Based on my reading of history, see my risks due to inflation and confiscation as significantly higher than my risk of deflation.

Devastation is, and has always been, a persistent background risk that is {in the worst case} far beyond my ability to handle[8] or insure against.

For many, but definitely not all, types of trivial devastations, the farm acts as a type of insurance 'cause what it produces can, and has supplemented our diet. However, for the vast host of moderate and major types of devastations it is, and always will be, utterly inadequate.

When I look at geopolitics and geo-economics, regardless of the reasons why, believe a question worth asking is: based on their recent behavior, do foreign central banks trust any fiat currency?

Evidence suggests the answer is "no".

Why?

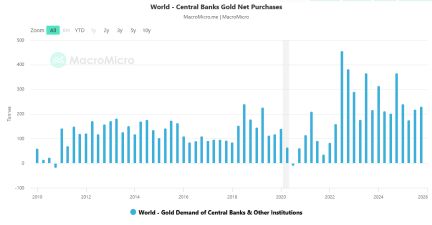

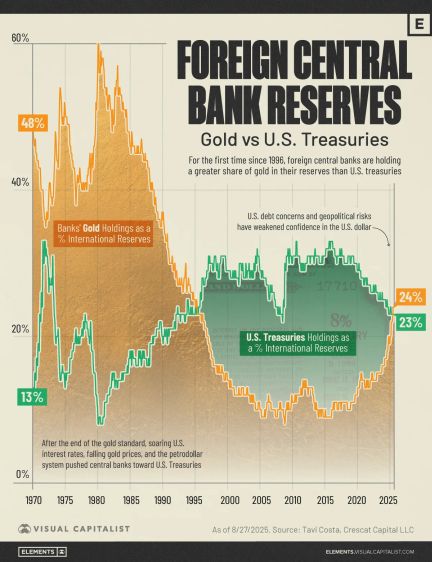

As shown below[9], foreign central banks, in the recent past, have been --on a net basis-- buying rather than selling gold.

As a consequence foreign central banks now hold more gold than US Treasuries.[10]

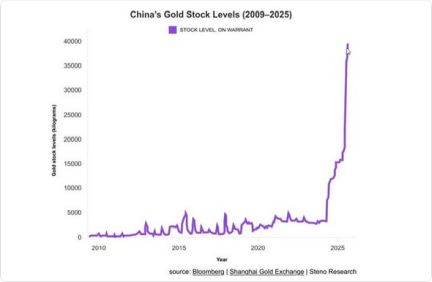

China has been buying gold for years. Based on what I've read, a significant fraction of those purchases are indirect, deliberately hidden, or otherwise not reported. Even so, China now holds far more gold than it did previously.[11]

As China continues to accumulate gold, it simultaneously reduces its US risk. Uncle can freeze (or seize) many types of foreign assets, but it cannot freeze (or seize) gold held within China.

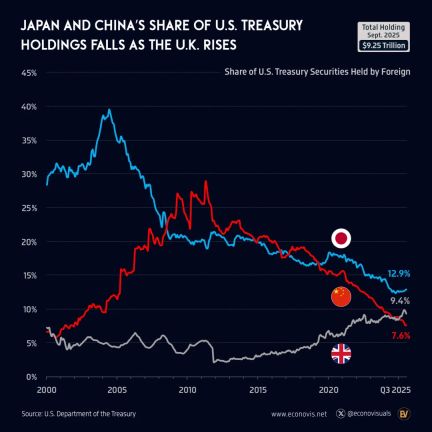

For me, another major geopolitical and geo-economic influence is Japanese debt[12] -- and Japan's share of US debt[13].[14]

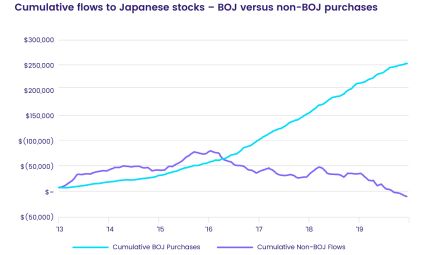

As Japan's interest rates continue to climb, suspect various entities there will sell US Treasuries[15]. Also believe the BOJ (Bank of Japan) will continue to sell US Treasuries in an attempt to manage {what I see as} the country's growing, unmanageable debt.

In order to maintain economic stability, believe BOJ actions have substantially increased instability ...

The ETF-purchasing program, launched in 2010 as a limited measure, grew over time into one of the most visible symbols of Japan’s unconventional monetary policy experimentation. The BOJ has a reported book value of 37 trillion yen (around $243 billion) in ETF holdings on its balance sheet, with an estimated market value of 70 trillion yen to 80 trillion yen. This amounts to roughly 7% of Japan’s stock market capitalization, suggesting the market implications of the BOJ’s equity holdings and selling schedule are profound. The BOJ’s plans to sell these risk assets under a framework that emphasizes avoidance of financial losses and limiting destabilizing effects on markets. At the steady pace that the BOJ foresees selling its equity holdings, the central bank will remain one of the Japanese economy’s largest holders of shares for decades ahead.[16] The net result of the BOJ's market intervention has been {from my perspective} rather disconcerting.

Unfortunately, the Fed's solution has, thus far, been {from my skewed perspective} a distinction without a significant difference ...

Between December 2005 and December 2025, the Federal Reserve's balance sheet grew from about $800 billion to roughly $6.5 trillion—an increase from around 6 percent to 21 percent of GDP.[17] And ...The U.S. Federal Reserve may soon need to grow its balance sheet through bond purchases and could consider shortening the average duration of its debt holdings, Federal Reserve Bank of New York President John Williams said on Friday.[18] For what it's worth, believe we discarded all the good economic solutions many decades ago 'cause they were seen as either politically unpopular or infeasible. What's left is {at best} uncomfortable and, if history is a reasonable guide quite painful.

As a consequence, my goals include the following:

- continue to grow my anticipated annual dividend income to supplement, in the near term, my pension as the associated COLA[19] fails to keep up with actual price increases

- grow the PM fraction[20] of my total portfolio to help preserve long-term wealth and purchasing power

- continue to upgrade farm infrastructure so we can better ride out a larger realm of trivial devastations

Good Luck to all and best wishes,

Kiisu

1. grokipedia.com

2. en.wikipedia.org

3. themacrobutler.substack.com

4. investopedia.com

5. Monetization happens when central banks permanently expand the monetary base to help fund government spending by exchanging interest-bearing debt for newly created cash. While this can provide financial support, it influences inflation and, if overused, may lead to hyperinflation. By separating monetary from fiscal policy, central banks try to maintain economic stability. Their challenge lies in supporting government financing when necessary while maintaining long-term price stability. investopedia.com

6. DGP-1a is my sole remaining tIRA. Continue to shove all its dividends into a MM fund so they can later be extracted to pay the RMD.

Sprott's Physical Gold and Silver Trust (CEF), which does not pay a dividend, is currently 13.8% of portfolio. Periodically intend to convert {by moving to DGP-1b(ROTH)} shares of CEF to manage the portfolio value and therefore adjust my annual RMD.

7. Appreciate your repeated references to the book.

amazon.com

8. Why?

Due to my background {in government, astrophysics, etc}, my view of devastation is far more dire than Bernstein's vanilla view:

... the risk of local military devastation in the developed world, outside of perhaps South Korea or Israel, seems remote at present. An unintended worldwide catastrophic nuclear exchange is slightly more likely, but the remediation options in this instance are, shall we say, limited. (During the Cuban Missile Crisis of 1962, when apocalypse seemed more than possible, an apocryphal story has a young derivatives trader asking an older one whether to go long or short equity options. The immediate reply, "Long, of course. If things turn out all right, we'll make a ton of money." Quavered the younger trader, "And if they don't?" To which the older trader rather cheerfully replied, "Well, then, there won't be anyone on the other side of the trade to collect from us!") ...

There is one devastation scenario that can present a localized threat to a single nation, and that is civil war, again, a very distant prospect in this day and age in a developed nation. A terrorist nuclear attack on a major metropolitan area anywhere in the world would fall under the "severe and localized" heading as well. Whether civil war or a nuclear terrorist attack is more or less likely than a global nuclear exchange is an imponderable, but at least the first two disasters offer the possibility of escape. Forecasting future cataclysms, in any case, requires humility since the most obvious threats are only rarely the ones that pan out. (pg 20) Why?

'Cause Bernstein fails to account for numerous natural and man-made events which would devastate today's modern world and its fragile infrastructure, which includes such things as:

- Carrington and Miyake events

- Gamma Ray Bursts

- engineered pandemics

- impact events and super-volcanoes

- Nuclear EMP

grokipedia.com

en.wikipedia.org

grokipedia.com

en.wikipedia.org

grokipedia.com

en.wikipedia.org

https://

grokipedia.com

en.wikipedia.org

grokipedia.com

en.wikipedia.org

grokipedia.com

en.wikipedia.org

9. en.macromicro.me

10. visualcapitalist.com

11. threads.com@stocksharks/post/DQGSF6EDKxT/china-has-massively-increased-its-gold-reserves-since?hl=en

12. At the top of the list, Japan holds a staggering 230% debt-to-GDP ratio, reflecting decades of fiscal stimulus and aging demographics. visualcapitalist.com

13. With $1.2 trillion in U.S. Treasuries, Japan is the largest foreign holder of U.S. debt.

In 2019, Japan overtook China, marking a major shift from a decade earlier, when China held nearly $1.3 trillion. Since then, China’s Treasury holdings have been nearly cut in half, while Japan’s have risen more modestly, up $61 billion over the same period. visualcapitalist.com

14. voronoiapp.com

15. "Japanese investors in the past have been particularly aggressive in buying debt in other markets, in particular the U.S., where interest rates have been higher than in Japan," said Yardeni. cnbc.com

16. See:

- The Bank of Japan Must Define a Strategy for Its ETF Holdings – Not Just Its Sales (Oct 2025)

cepweb.org

- A rising tide lifts some (Japanese) boats: The Bank of Japan’s ETF purchases and their impact on market signals for individual stocks (Mar 2021)

At the time of their presentation, the Bank of Japan (BOJ) was seven years into its ETF Purchasing Program, launched in early 4Q10 and expanded in 2013 as part of the “three arrows” policy launched by then Prime Minister Shinzo Abe to snap Japan out of the deflationary slowdown that started in 1991 and came to be known as the “lost decades”. Its ETF holdings at the end of the year totaled some $175 billion with unrealized gains that added another $50 billion to the value of those holdings.

Four years later, the combined value of the BOJ’s domestic ETF holdings exceed $450 billion. It owns over 5% of the total market capitalization of the TOPIX index and, by some estimates, has acquired 70% of the total ETFs eligible under the terms of its current program. This makes it the largest shareholder, institutional or otherwise, in Japan, and the question of what this is doing to classic price, value and volatility metrics has taken on a new urgency. epfr.com

17. (Jan 2026) federalreserve.gov

18. (Nov 2025) reuters.com

19. The CSRS pension system uses the SS COLA data and formula. The continual CPI adjustments have the effect of increasing GDP and minimizing Uncle's expenses.

investopedia.com

20. Includes such things as:

- junk silver (old US 90% silver coins) and gold coins

- Sprott Physical Gold and Silver Trust (CEF)

- PM royalty and streaming companies

- PM miners

- critical mineral ETFs

As of 29 Jan, across all portfolios, the current fraction of all {except the coins} is 13.61% with CEF weighing in at over 9%. |