as posted on LI.

"The excitement is in the air as is the concern of the 2 - 10 year note spread which has been down to 19 basis points recently and as Deutsche Bank noted late last week, The USA 2 - 10 spread fell below the Japanese 2 - 10 spread for the first time since November 2007... and the Great financial crisis went into high gear shortly there after. The FED is going to invert the yield curve when the September rate hike of .25 % occurs.... the reason that the US 10 and 30 year Sovereign debt has rallied this past several weeks is the wise Family offices, the pension funds like Calpers scaled back US stock exposure in Q4 of 2017... Mark Cuban is sitting with more cash than in 10 years... as is Warren Buffett

The really big operators have to scale out of stocks before the final high due to their tremendous size.... Dr. Fleming and Mr. Walker can attest to this truism ."

JP

-------------------------------------------------------------

http://www.investing.com/rates-bonds/de-10y-vs-it-10y

on 04/25/2018 the spread was 113 basis points.... the spread shot all the way up to 290.5 basis points

by 05/29/2018... clearly there is concern that the Italian Government has some issues about the

ability and / or the willingness to pay off the Italian Govt debt in Euro's..... why not leave the Eurozone

currency and go back to the Italian Lira.... after all if the UK can leave the EU what, pray tell, is keeping

a right wing .. Italy first populists, who are looking askance at all of the Muslim Refugees that are over

whelming several countries in Europe;especially Germany, France,Sweden; there is significant blow-back

How long is the the EURO currency going to continue to exist??? especially since European banks have

a fair bit of exposure to Turkish Lira loans that will be defaulted on. and the defaults are coming on

South African Rand loans, Argentinian peso loans, ......

Here is the 7 year spread.....

Summary

Emerging market countries might be facing an economic crisis.

16 emerging market countries borrowed $3.4 trillion from foreign lenders, but their foreign exchange reserves amounted to $1.3 trillion.

The currencies of Argentina, Ukraine, Egypt, Turkey, and Brazil have depreciated against dollar by 80.3%, 69.0%, 60.9%, 60.5%, and 42.5%, respectively, over 5-year period.

The percentage of exports per GDP of Vietnam, Malaysia, Belarus, Brazil, Ukraine, Mexico, and Morocco were 98.6%, 75.2%, 65.0%, 57.8%, 47.9%, 37.4%, and 35.7%, respectively, in 2017.

Emerging market countries would be facing high currency, liquidity, inflation, interest rate, default, and emerging market risks due to the shortage of foreign exchange reserves, strong dollar trend, and trade war.

Foreign Exchange ReservesEmerging market (EM) countries are facing an economic crisis. The EM countries on the above chart do not have sufficient amount of foreign exchange reserves to pay off external debts. The 16 EM countries borrowed total of $3.4 trillion from the foreign lenders. The 16 EM countries' foreign exchange reserves amounted to $1.3 trillion, which is short by $2.1 trillion to pay off the external debts.

---------------------------------------------

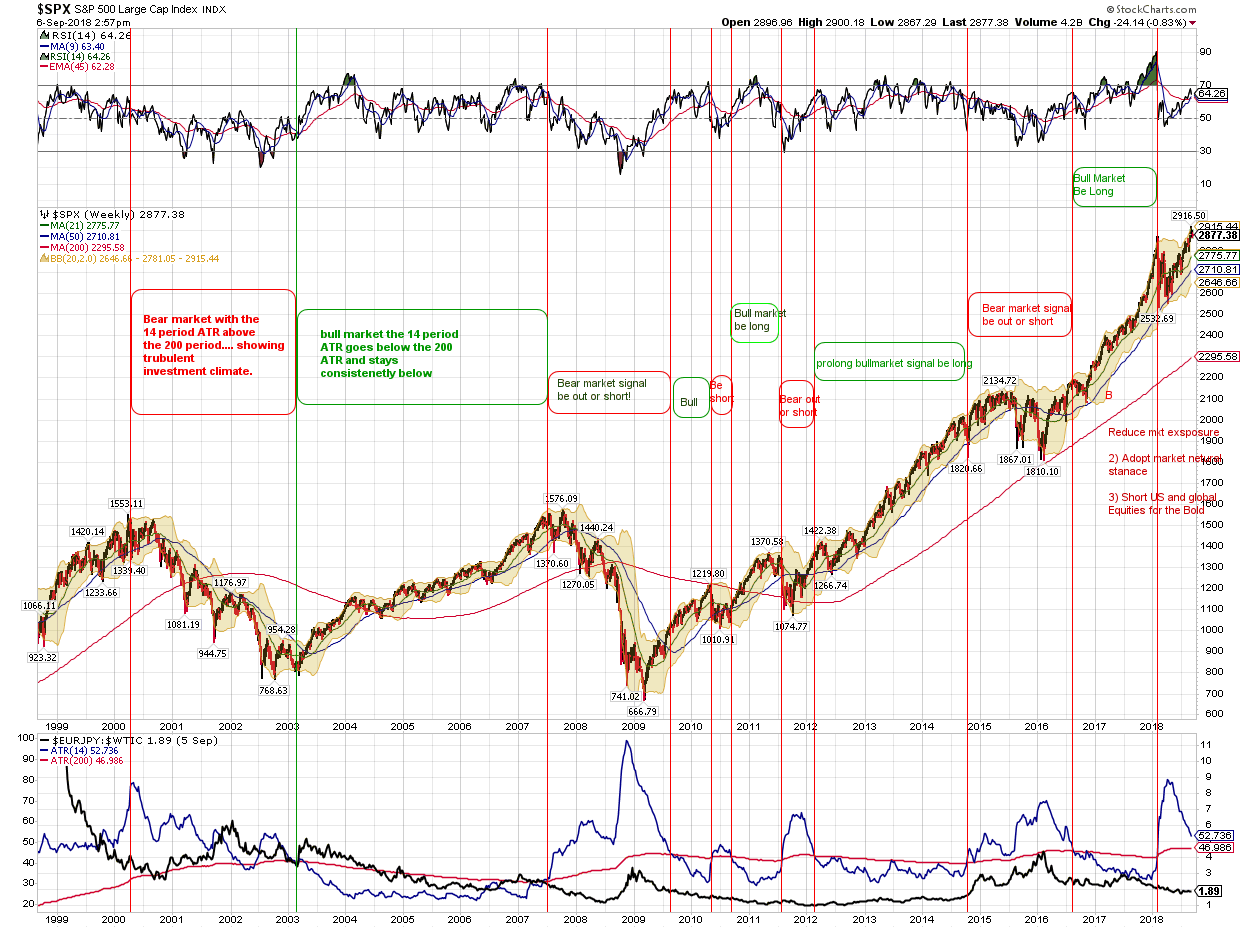

The GFA proprietary Weekly 14 week and 200 week ATR on the EUR/JPY:$WTIC ratio is still in caution

mode (the red flag is still out indicating there are rip currents in the waters.)

The Model which is longer term in Nature has been indicating abnormally high volatility in the 4 deepest

markets in the world, the EUR, JPY, WTIC and USD index.

----------------------------------------------------------------------------------------------------

Memories are very long on Wall Street... Lehman Brothers and Bear Sterns, not being team players in

the 1998 LTCM bailout resulted in them being severely punished for their intransigence when the next

big financial crisis occurred a decade later....

Lehman Brothers was liquidated..... and Bear Sterns was paid a few cents on the dollar a token amount by JPM

September 15, 2008

The filing for Chapter 11 bankruptcy protection by financial services firm Lehman Brothers on September 15, 2008, remains the largest bankruptcy filing in U.S. history, with Lehman holding over US$600,000,000,000 in assets.

Bankruptcy of Lehman Brothers - Wikipedia

en.wikipedia.org

Search for: When did Lehman Brothers go under?

Who was responsible for Lehman Brothers collapse?

Dick Fuld, the chief executive who led Lehman Brothers to the largest corporate collapse in modern times, has defended the failed investment bank's culture, insisting that it was a victim of wider market excesses and regulatory failings in his first public speech since the banking crash of 2008.May 28, 2015

Lehman Brothers' former CEO blames bad regulations for bank's ...

theguardian.com.

Why the Fed had to bail out Bear Stearns. ... Now Bear is being bailed out by the Fed via JPMorgan Chase, which is buying the troubled firm for $2 a share. And as one might expect, the finger-pointing and recriminations have already begun.Mar 18, 2008

Why the Fed had to bail out Bear Stearns.

www.slate.com/articles/business/moneybox/2008/03/bear_run.html

1998 bailout[ edit]

On September 23, 1998, the chiefs of some of the largest investment firms of Wall Street— Bankers Trust, Bear Stearns, Chase Manhattan, Goldman Sachs, J.P. Morgan, Lehman Brothers, Merrill Lynch, Morgan Stanley Dean Witter, and Salomon Smith Barney—met on the 10th floor conference room of the Federal Reserve Bank of New York (pictured) to rescue LTCM.

Long-Term Capital Management did business with nearly everyone important on Wall Street. Indeed, much of LTCM's capital was composed of funds from the same financial professionals with whom it traded. As LTCM teetered, Wall Street feared that Long-Term's failure could cause a chain reaction in numerous markets, causing catastrophic losses throughout the financial system.

After LTCM failed to raise more money on its own, it became clear it was running out of options. On September 23, 1998, Goldman Sachs, AIG, and Berkshire Hathaway offered then to buy out the fund's partners for $250 million, to inject $3.75 billion and to operate LTCM within Goldman's own trading division.

The offer was stunningly low to LTCM's partners because at the start of the year their firm had been worth $4.7 billion. Warren Buffett gave Meriwether less than one hour to accept the deal; the time lapsed before a deal could be worked out. [25]

Seeing no options left, the Federal Reserve Bank of New York organized a bailout of $3.625 billion by the major creditors to avoid a wider collapse in the financial markets. [26] The principal negotiator for LTCM was general counsel James G. Rickards. [27] The contributions from the various institutions were as follows: [28] [29]

$300 million:

Bankers Trust,

Barclays,

Chase,

Credit Suisse First Boston,

Deutsche Bank,

Goldman Sachs,

Merrill Lynch,

J.P.Morgan,

Morgan Stanley,

Salomon Smith Barney,

UBS

$125 million: Société Générale

$100 million: Paribas, Crédit Agricole [30]

**** Bear Stearns and Lehman Brothers [30] declined to participate. ****

In return, the participating banks got a 90% share in the fund and a promise that a supervisory board would be established. LTCM's partners received a 10% stake, still worth about $400 million, but this money was completely consumed by their debts. The partners once had $1.9 billion of their own money invested in LTCM, all of which was wiped out. [31]

The fear was that there would be a chain reaction as the company liquidated its securities to cover its debt, leading to a drop in prices, which would force other companies to liquidate their own debt in a vicious cycle.

The total losses were found to be $4.6 billion. The losses in the major investment categories were (ordered by magnitude): [21]

1) $1.6 bn in swaps

2) $1.3 bn in equity volatility

3) $430 mn in Russia and other emerging markets

4)$371 mn in directional trades in developed countries

5) $286 mn in Dual-listed company pairs (such as VW, Shell)

6) $215 mn in yield curve arbitrage

7) $203 mn in S&P 500 stocks

8) $100 mn in junk bond arbitrage

no substantial losses in merger arbitrage

Long-Term Capital was audited by Price Waterhouse LLP.

After the bailout by the other investors, the panic abated, and the positions formerly held by LTCM were eventually liquidated at a small profit to the rescuers. Although termed a bailout, the transaction effectively amounted to an orderly liquidation of the positions held by LTCM with creditor involvement and supervision by the Federal Reserve Bank.

No public money was injected or directly at risk, and the companies involved in providing support to LTCM were also those that stood to lose from its failure. The creditors themselves did not lose money from being involved in the transaction.

Some industry officials said that Federal Reserve Bank of New York involvement in the rescue, however benign, would encourage large financial institutions to assume more risk, in the belief that the Federal Reserve would intervene on their behalf in the event of trouble. Federal Reserve Bank of New York actions raised concerns among some market observers that it could create moral hazard since even though the Fed had not directly injected capital, its use of moral suasion to encourage creditor involvement emphasized its interest in supporting the financial system . [32]

LTCM's strategies were compared (a contrast with the market efficiency aphorism that there are no $100 bills lying on the street, as someone else has already picked them up) to "picking up nickels in front of a bulldozer" [33]—a likely small gain balanced against a small chance of a large loss,

like the payouts from selling an out-of-the-money naked call option.

------------------------------------------------------------------------------------------------------------------------------------

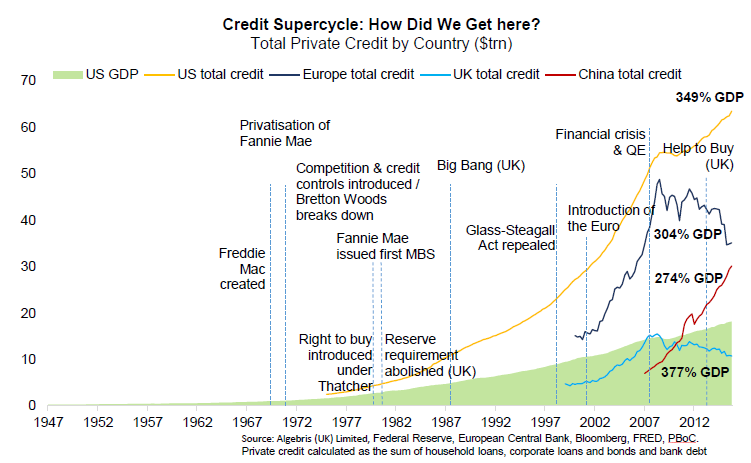

The Credit SuperCycle as presented on the World Economic Forum website

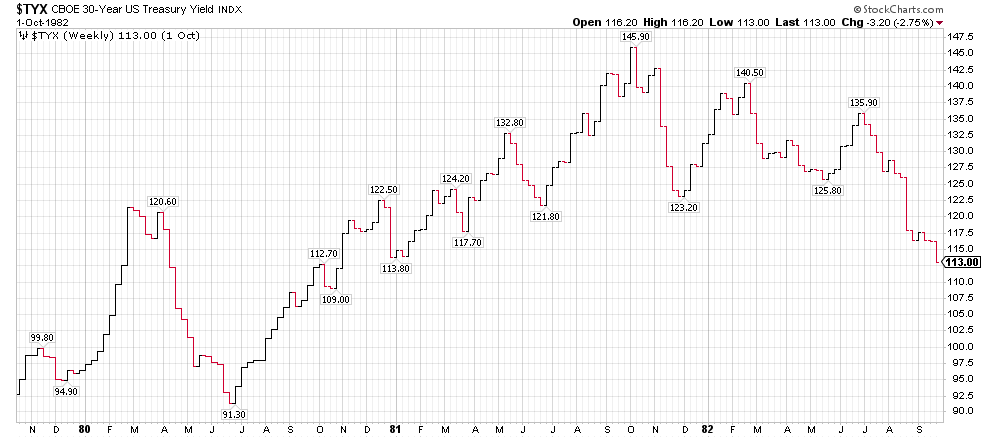

The 72 year master cycle in the US 30 year Treasury bond --- The US entered a secular bull market in yield (interest rates are going higher) and bear market in bond prices on July 8 2016. We are now in the

wave of advance that the general Wall street and global financial community comes to the mass realization

that interest rates are going up.

THE 30 YEAR US TREASURY BOND WEEKLY CHART FROM LATE 1979 TO SEPTEMBER 1982

THE High in Yield was 14.59% on Oct 12 1981.

we have a number of global central banks taking steps to normalize interest rates, which means to raise them and since we have had 8 years of global Zero interest rate policy, on short rates in the US, the ECB, the BOJ, the SNB - swiss national bank, the swedish Riskbank, the BOE was very accomodative...

and so it's a brave new world of the reduction of monetary stimulus and we have already had 3 or 3 Fed Fund increases here in the US.... are we up to 4 already? We have another coming in Dec.

and we have never seen the global central banks in this position, We have the FED, the Bank of England, the Reserve Bank of Australia, the central bank of Canada, and the European Central bank all in tightening

mode....... .. they have never been in this position and in central banking land.... mistakes in the movement of the short term borrowing rates can occur, especially when you have multiple countries doing the same thing... It sets up uncertainty in the Long dated FX market.... creates uncertainty for Banking, Insurance, Reinsurance companies as to how to hedge and value their long dated commitments.

Endowments, pension funds , soverign wealth funds are also all impacted by this grand experiment.

as Hyman Minsky famously said "stability is Destabilizing" that has always been the case and

will always be the case...we have been through a long period of stability which has let lots of all of the

above market participants, companies, hedge funds.... take advantage of very cheap credit by issuing a vast

ocean of it.... we shall find out who is over levered..... and then their are exogenous shocks and black swan

events.

-------------------------------------------- |