I thought this was a pretty decent piece on XOM. Some of the numbers, particularly the amount they have spent to 'tread water' in terms of reserves, and what they will have to borrow to fund capex and the dividend are worrisome. If oil moves up they will be okay, if not this guy makes a pretty good argument for a dividend cut at some point which will hurt the stock.

Edit: - I think the balance sheet issues are the reason CVX is holding up somewhat better than XOM.

Exxon Mobil Cannot Cover Its Dividend, And That's Great News

Feb. 16, 2020 9:45 AM ET

|

888 comments

|

About: Exxon Mobil Corporation (XOM), Includes: BOIL, DGAZ, GAZ, GAZB, IMO, KOLD, OXY, UGAZ, UNG, UNL

Rida Morwa

Research analyst, REITs, energy, Dividend income for retirees

MARKETPLACE

High Dividend Opportunities

(53,039 followers)

Summary

Exxon Mobil hovers near multi-year lows as an entire generation shuns the broken stock.

The dividend coverage does not remotely look good.

We break down what this means for the stock.

We also take the time to recommend a better choice.

Looking for a portfolio of ideas like this one? Members of High Dividend Opportunities get exclusive access to our model portfolio. Get started today »

Co-produced with Trapping Value

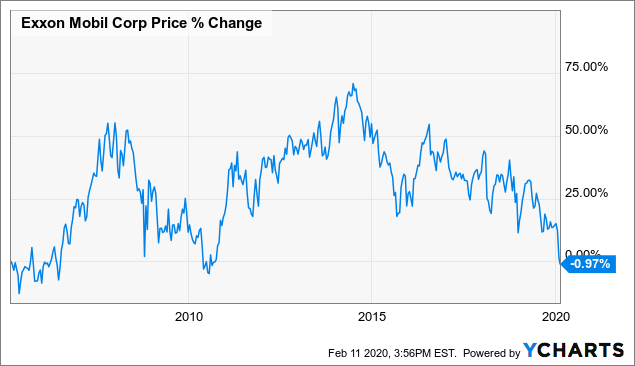

Exxon Mobil ( XOM) has certainly divided the investment community. Bulls argue that this price is the best thing since sliced bread. Bears argue that if XOM keeps contributing to climate change, we won't have any bread. The debate rages on. Certainly history has been on the side of the bears. XOM stock price has barely budged since Feb. 24, 2005.

Data by YCharts Data by YCharts

The rearview mirror look is fantastic, but we have to analyze not what XOM's price did, but what it will do in the next 15 odd years. To do that we have to understand why XOM is struggling and why that struggle is putting pressure on it to fund its dividend.

The companyXOM is the largest integrated oil company with a big global reach. From oil production, to refining and marketing, XOM has its hands in everything related to energy. At one point it also was the largest company by market capitalization.

Of course, the only thing constant is change and XOM's market cap has shrunk while technology stocks have now taken over the world. We could go on and on about XOM's introduction, but pretty much everyone does know what the company engages in. Instead of doing that, we will jump straight to the key issue with XOM. The inability to grow and pay its dividend.

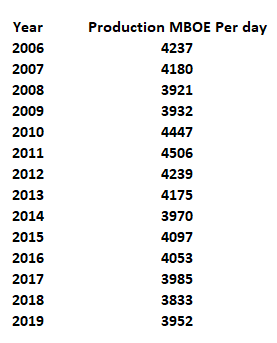

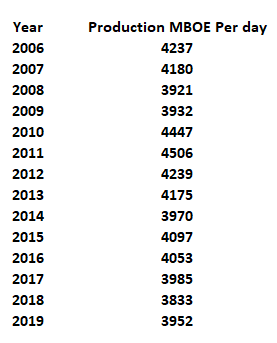

A brief history of big problemsXOM cannot grow. Since 2006, about the time from where its share price has been flat, its production as expressed in thousands of oil equivalent barrels per day (MBOE) has actually declined.

Source: Author, from company filings

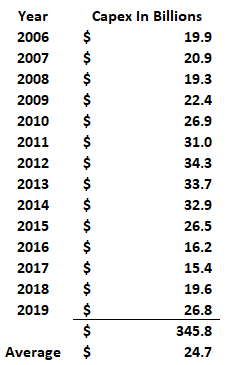

That's an incredibly long time frame and puts to ease any doubts about any temporary issues. World production of course has grown in that time frame, both for oil and natural gas. XOM has of course sold and bought assets during that time frame, but it also has invested very huge amounts of capex in its projects.

Source: Author, from company filings

When investing $25 billion a year cannot keep your production flat, you will obviously have problems.

It gets worseWhile oil companies love to lump all production into one single easy to understand metric, like "oil equivalent production," pretty much everyone knows that metric just serves to obfuscate. To explain what we mean by that, let us quickly revisit XOM's production numbers.

Source: Author, from company filings

At first glance it looks bad because production declined by about 285,000 barrels per day over 14 years. But what makes this problem worse is that all of that was a decline in liquids production. In 2006, XOM produced 2.681 million barrels per day of high margin liquids. This number has since declined to 2.386 million barrels per day. That's a decline of 295,000 barrels per day. Now, pricing for natural gas varies throughout the world, but everywhere you look, natural gas trades cheaper than oil and natural gas liquids. So increasing a lower margin product and decreasing a higher margin product has been bad for cash flow.

How Bad You Ask?While investors may think we are making mountains out of molehills here for a small decline, we think they should hear us out. The margin shift along with production declines has been beyond terrible for the company. In 2006, XOM produced close to $50 billion of operating cash flow.

Source: 2007 Annual report

Fast forward to 2019 and we have operating cash flow of almost 40% less.

Source: XOM Q4, 2019 results

There are two main reasons for this. The first is cost inflation as everything today is more expensive than it was 14 years ago. XOM hence makes less operating cash flow per barrel. The second is the big collapse in natural gas prices which have moved down by 75% in North America.

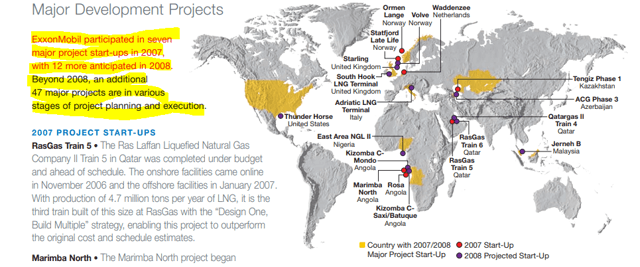

What lies aheadWe keep reading about all the excitement about XOM's projects in Guyana and its decision to jump on the Permian treadmill. In that regard, we think that those projects are a way of offsetting base decline rates. Anyone projecting any big increases in cash flow from them is very sadly mistaken. To understand this, please have a look at the number of projects XOM has brought online every single year. We show below 2007 just as one example.

Source: 2007 Annual report

XOM started 7 major projects in 2007 and had a huge number (47) on its plate. Some were delayed, but most were eventually completed. Yet, XOM's production has declined since then. Remember, XOM has spent $25 billion a year over the last 14 years and it could not keep production flat. Even after increasing production of near worthless natural gas in North America, it could not hold total production barrels steady. Depletion and base declines never sleep and Guyana and Permian will just offset these production declines. So if you are buying because these events will be game changer, please don't.

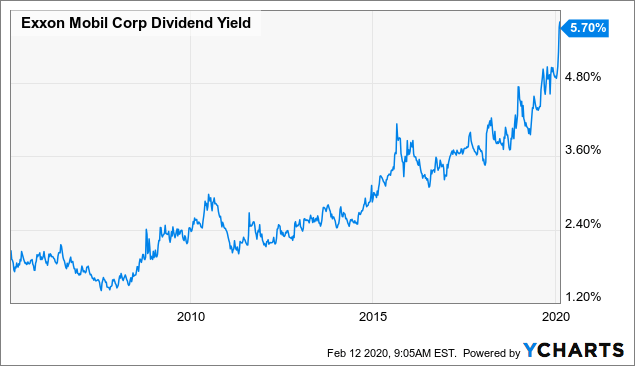

Debt For DividendsSo we can see that XOM cannot maintain its production and has replaced lower margin natural gas for higher margin liquids. But it still pays a rocker of a dividend. That dividend has increased from $1.28 to $3.48. Alongside a flat stock price, the dividend increase has pushed the yield up to 5.7%.

Data by YCharts Data by YCharts

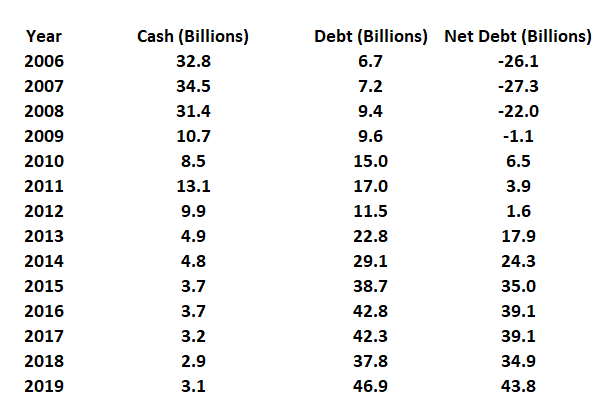

5.7% is an astounding yield from a company with a AA balance sheet. But that yield shows half the picture. XOM is showing an increasing inability to fund its dividend and capex. So much so that XOM's debt continues to steadily inch up.

Source: Author, from company filings

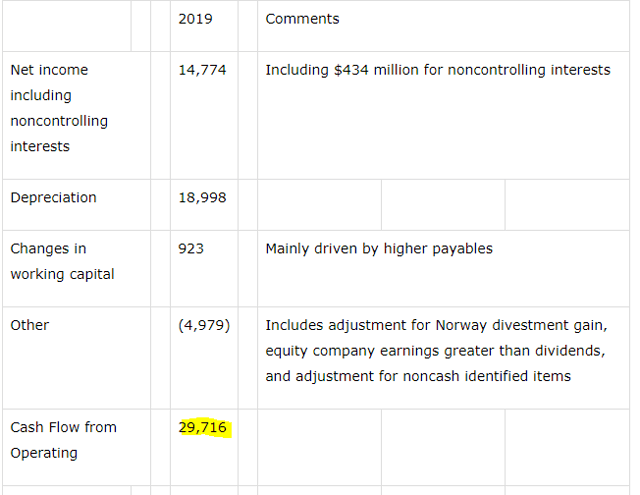

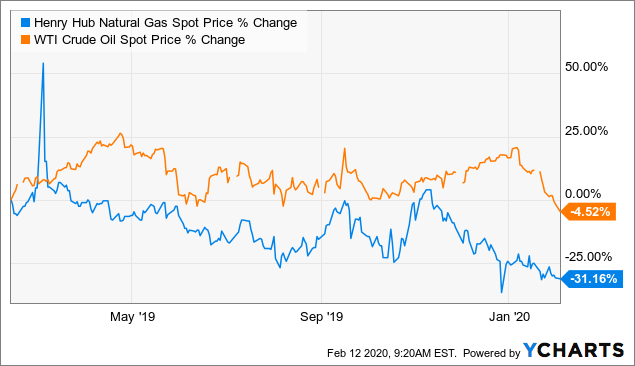

The jump in 2019 was rather notable. Operating cash flow edged near $30 billion but capex consumed almost all of that. Dividends of $14.7 billion were financed mainly by asset sales and expanding debt. What's worse is that the current strip looks far worse than the 2019 prices XOM got.

Data by YCharts Data by YCharts

Abandon the dividend?Based on XOM's capital expenditure plans of $30 billion, operating cash flow will be dwarfed by just the capex in 2020. There should be zero left for the dividends.

So you can assume another $15 billion odd increase in debt over the course of 2020. XOM would need strip prices exceeding $75 WTI and natural gas over $3.00 to start to fund the dividend and capex sustainably, and we possibly are being conservative. The reason is that higher oil prices tend to usually detract from downstream earnings and XOM benefits rather slowly as prices move up.

Why this is great (not necessarily for XOM)At the bottom of the cycle, pretty much no one can make money. We are sure all of you have heard this ridiculous comment by XOM.

CEO Darren Woods said the Irving-based company will see very good returns in the Permian all the way down to $35 a barrel.

Source: Darren Woods Laying It On Thick

Well Darren Woods must think that pretty much no one has a calculator. If XOM did somehow through its relentless drilling boost production and force oil prices down to $35 to test that theory, it would likely find itself with a debt rating in the BBB range. It would be adding debt to its balance sheet at the rate of $30 billion a year to fund its dividend and capex (assuming natural gas prices stay where they are). If you think we are alone in this pessimism, then take a moment to hear what some other analysts have to say.

Just to cover project spending and dividend payouts without borrowing, Exxon would have needed international crude prices around $100 a barrel, according to Citigroup Inc. analyst Alastair Syme. That’s well above the $62 fourth-quarter average.

Source: Yahoo

The more probable situation though is that XOM will either have to slash its spending or its dividend, even if prices move up from here. Giving up on Permian growth and focusing on smaller higher return projects is likely to help move demand and supply in better balance and stop subsidizing the world's energy costs at the expense of shareholders.

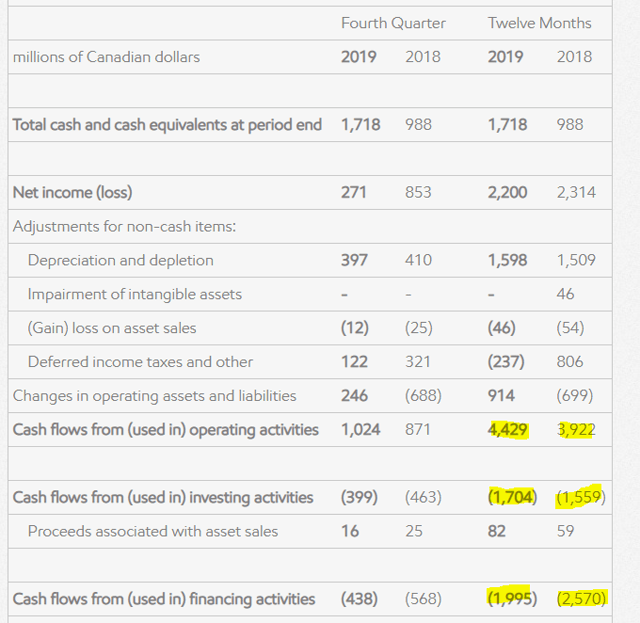

Do You Buy?We are positive on energy prices but XOM's capex and dividends just don't do it for us. Instead we like the company controlled by XOM, Imperial Oil ( IMO). Imperial generated free cash flow over $2.5 billion in 2019 after capex and returned most of that to shareholders via dividends and buybacks.

Source: Imperial Oil

In fact it continues to fund XOM on a daily (we mean this literally) basis by buying back IMO shares held by XOM.

Source: Canadian Insider

IMO has the smaller yield but it's far more sustainable and fully funded internally.

Another company we like is Occidental Petroleum ( OXY) which is deleveraging in full swing and trades at very attractive valuations. Not long ago, the shrewd investor who goes by the name Warren Buffett bought both convertible preferred shares and common shares of Occidental through Berkshire Hathaway (NYSE: BRK.A) ( BRK.B) in late 2019.

BRK.B purchased 7.4 million common shares, worth about $300 million, and $10 billion worth of convertible preferred shares. He would have done this if he did not see the oil cycle turning after years of battering for the E&P names. As income investors, we would buy OXY for the dividend and enjoy the delicious 7.5% yield.

ConclusionXOM's problems are a symptom of unsustainable commodity prices. The company can either embrace that reality or continue to dig itself into a hole and promise returns "down to $35/barrel". The correct approach is to dial back capex to where there are sustainable returns on capital employed. At the current strip we expect all capital to be wasted down the proverbial sewer. We do expect XOM to get it and it might come with a CEO change. Ultimately prices should rise to reflect what's needed for energy companies to make money over the full cycle. We would be foolish to make a bet against XOM when sentiment is so one sided, hence we are taking a neutral view. But for our money, IMO and OXY are the place to be.

Disclosure: I am/we are long IMO, OXY, VET. I wrote this article myself, and it expresses my own opinions. I am not receiving comp |